The China market has experienced sharp falls over the past few months even as global equity markets hit all-time highs. How should investors understand the recent events and think about investing in China going forward?

In a webinar this month, Samantha Horton, Head of Business Development at Syfe, shared her insights on the deeper implications of China’s regulatory shake-up as well as the outlook for Chinese equities going forward. Prior to Syfe, Samantha has 15 years of research and investing experience under her belt, having worked at Morgan Stanley and Broad Peak, a multi-billion dollar hedge fund, as Managing Director.

Please watch the webinar replay here and read the highlights of the session below.

Highlights from the webinar

What has happened in China? (1:30)

Numerous sectors and companies in China have been hit by a wave of regulatory crackdowns in the last 10 months. The reforms primarily target three categories: antitrust and monopolistic activity, data privacy and data security, and social equality and responsibility.

While these reforms are well-intentioned and guided by the Chinese government’s principles to maintain social harmony and financial stability, they have negatively impacted companies’ business activities and profitability.

For instance, news of the probe into DiDi’s (a ride-hailing company) cybersecurity policies was revealed days after their initial public offering (IPO) in the US. Consequently, DiDi was forced to be removed from the app store, leading to a big drop in stock prices and significant investor outrage.

More recently, reforms in the after-school and for-profit tuition sector have hit the likes of TAL Education Group and New Oriental Education & Techno, in a bid to regulate the industry and reduce the financial burden of education on lower and middle-class households.

Key implications for Chinese companies (7:00)

The reforms impact Chinese companies in four main areas outlined below.

Firstly, we can expect to see greater transparency both in terms of the way companies use and store user data and the way consumers are charged for goods and services.

We can also anticipate reduced inequality as the government attempts to level the playing field for different social classes of the population.

There is also likely to be reduced M&A activity and listings due to higher scrutiny around transactions that potentially create or enhance monopoly situations.

Finally, there will be increased competition given that less monopolistic actions are allowed. While this would lower the profitability of monopoly companies, it translates to better outcomes for consumers in terms of pricing and choice.

Impact on financial markets (11:35)

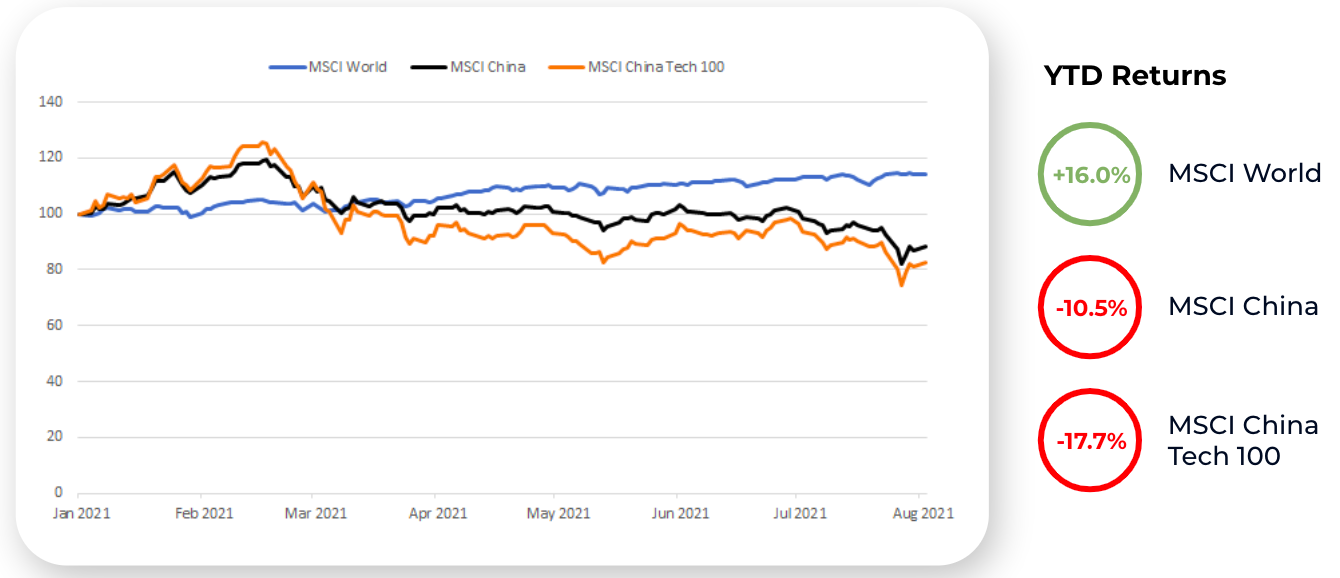

Following these regulatory actions, we have seen significant underperformance for Chinese stocks since late February, particularly those in the Internet and technology sector.

While the MSCI World Index is at an all-time high, up 16% year-to-date (YTD), the MSCI China Index and the MSCI China Tech 100 Index is down 10.5% and 17.7% YTD respectively, after outperforming at the beginning of the year.

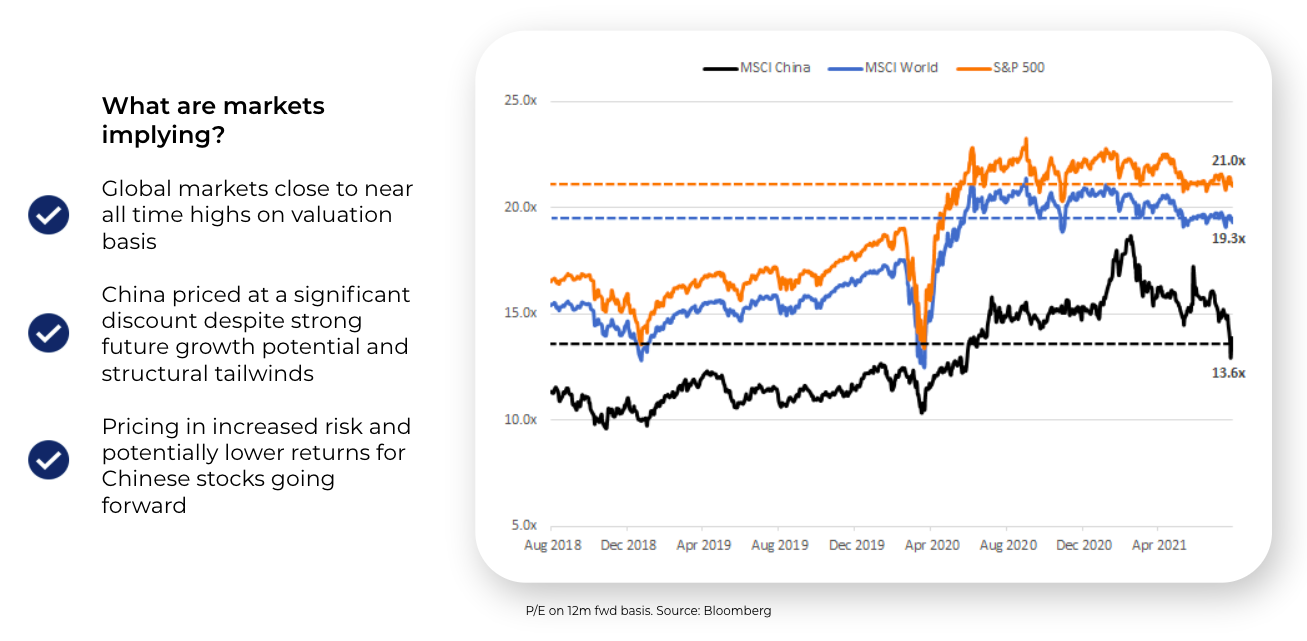

The chart below shows the 12-month forward price-to-earnings (P/E) multiples, which indicates how much a stock is trading at in terms of the earnings it generates.

Similar to the previous chart, while global markets, represented by the S&P 500 and MSCI World Index, are at an all-time high, China stocks are trading at a significant discount close to 2019 and pre-COVID-19 levels despite a positive long-term growth outlook. This indicates that the market is pricing in significant risk and potentially lower returns for Chinese stocks going forward.

While we agree that large-cap monopoly companies have taken some hits to profitability, we believe that a lot of this has been reflected in earnings estimate cuts. For example, Alibaba missed its revenue estimates recently for the first time in two years which would normally lead to a sharp correction in share price. However, the stock was only down 1.4% and bounced back the next day, showing that the markets have already priced in investors’ bearish sentiments.

In fact, both Alibaba and Tencent are trading at P/E multiples of 20x, which is an all-time low. This is decent compared to the astronomical P/E ratios we see in some of the US growth and Internet stocks at the moment.

China market outlook (16:20)

Ultimately, Chinese regulators do not want financial markets to come down, or worse, trigger a downturn in the real economy and put growth targets at risk. As such, we can expect some potential support levers such as fiscal stimulus measures in the next few months. This generally bodes well for equity markets.

In the long-term, the reforms will likely result in lower outsized returns for large monopoly companies. However, they will also create a more sustainable and transparent market place, which translates into higher quality of growth and more stable returns.

Taking these parts together, this means that we should expect to see higher short-term volatility but greater benefits and stability in the long-term.

You must be logged in to post a comment.