Thought Of The Week

U.S Jobs Report, Consumer Confidence Index

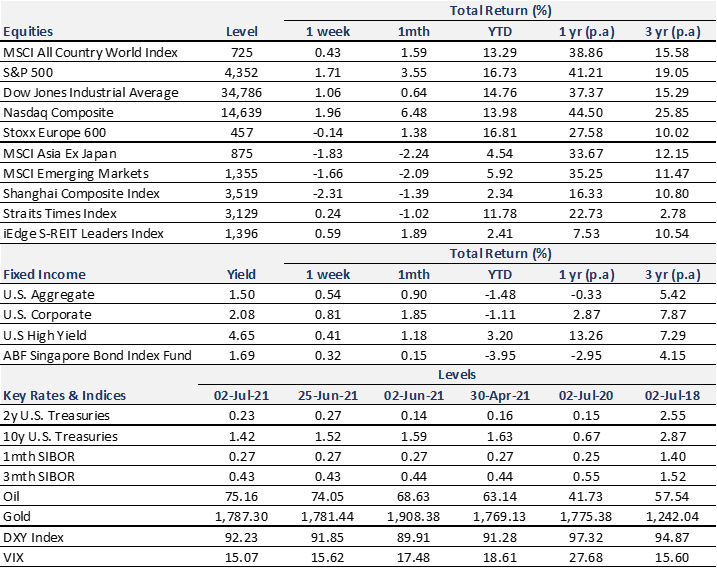

U.S stocks continue to extend its rally with jobs data suggesting that the economy is recovering better than expected. June nonfarm payrolls jumped by 850,000, bolstered by strong gains in leisure and hospitality compared to the median estimate of 720,000. Although the figure was well above expectations, markets have decidedly agreed that this will not raise pressure on the Federal Reserve to pare monetary policy support since it is still well below the pre-pandemic level. Meanwhile, consumer confidence index recorded its the highest level since February 2020 due to lower COVID infections, rebounding employment, and elevated savings. With the renewed optimism and historically low mortgage rates, demand for durable goods such as homes and cars remains strong even as spending shifts backs to services such as air travel and dining out. Major U.S indices inched higher while Chinese stocks fell for the week as open market operations undertaken by China’s central bank to drain funds from the financial system contributing to the declines.

Oil Meeting

The rapid rebound in the energy demand has been outpacing supply over the past year, driving oil prices to its highest levels while adding to the mounting inflationary pressures in the global economy. The highly anticipated meeting of the OPEC+ was forced to postpone on Thursday after the United Arab Emirates disagreed with the pace of production level and wanted to change the baseline from October 2018 to April 2020 to be allowed to pump more oil. However, this will not only affect other producers who saw their output decreased during that period, it also tarnishes the cartel’s carefully reconstructed reputation and creates confusion in the market. The cartel met again on Friday, but the deadlock was left unresolved. With the possibility of an impasse acting a “price accelerator”, WTI crude and Brent crude settled at $75.16 and $76.17 per barrel on Friday although headwinds remain from the delta variant capping demand and U.S nuclear deal with Iran lifting supply.

Chinese Communist Party 100th Anniversary

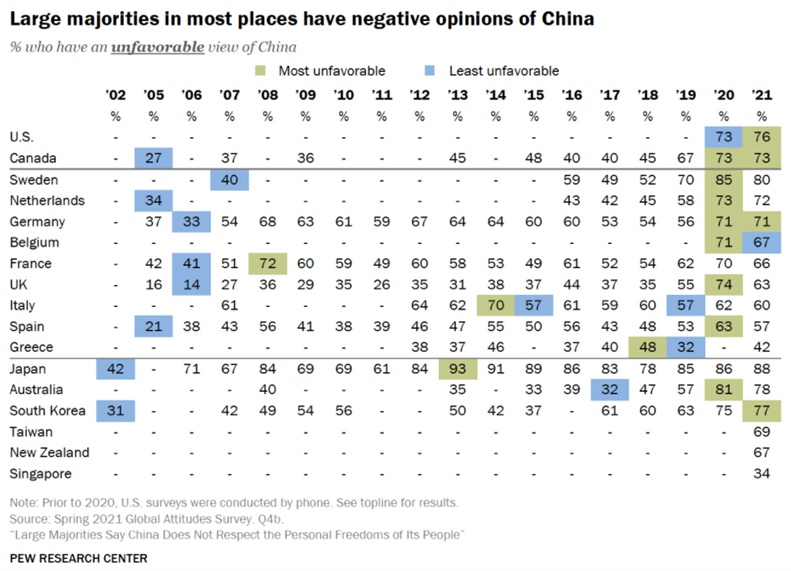

“Let China sleep, for when she wakes, she will shake the world.” About 200 years ago, Napoleon Bonaparte, a French military leader and emperor, cautioned that China would pose a global threat to other nations once she becomes conscious of her social, political, and economic development. The prophecy is getting increasingly fulfilled in recent years as Chinese Communist Party (CCP) marked its 100-year anniversary on Thursday. In a nationwide address aimed at building nationalist support, President Xi Jinping vowed to “never allow any foreign forces to bully, coerce and enslave us” or they will “surely break their heads on the steel Great Wall built with the blood and flesh of 1.4 billion of Chinese people.” The defiant tone in his speech sent a stern warning to the U.S and its allies where geopolitical tensions have been escalating and negative views of China are increasing across the developed world. Despite the countless achievements, CCP faces looming challenges ahead with declining birth rates and growing apathy from the younger generation especially the “flat liers” who are losing hope in the “Chinese Dream”. With the road going to be harder for the next 100 years, the CCP needs to continue to adapt and spur innovation while managing the growing dissent in Hong Kong and Taiwan.

Chart Of The Week

Important Information and Disclosure

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.