Thought Of The Week

Powell’s Testimony, Jobs Report, OPEC Meeting

After months of defending that inflation is “transitory”, Fed chair Jerome Powell told Congress on Tuesday that it is time to retire that word as it is proving more powerful and persistent than expected. Continued strength in goods spending, shortage of microchips and shipping squeeze have increased costs and pushed the consumer price index (CPI) persistently above Fed’s 2% inflation target. After Powell’s remarks, money markets are estimating that the Fed will hike as early as May.

U.S employers added 210,000 jobs in November compared to expected 550,000. While the headline number disappointed, the report also showed that the unemployment rate had dropped, and the overall participation rate increased. Friday’s jobs report was not weak enough and it is unlikely to change the market’s view that the Fed could push up the timing of rate increases to tamp down inflation.

Meanwhile, OPEC agreed to continue increasing oil production in spite of falling oil prices and the new Omicron variant. The group decided to stick to its existing policy, giving in to the pressures by the consumer countries as it is part of core inflation and affects consumer inflation expectations disproportionately.

Delisting Jitters

The Securities and Exchange Commission (SEC) announced its final plan on Thursday for a new law that mandates foreign companies to comply with U.S disclosure requirements within 3 years in order to stay listed on U.S exchanges.

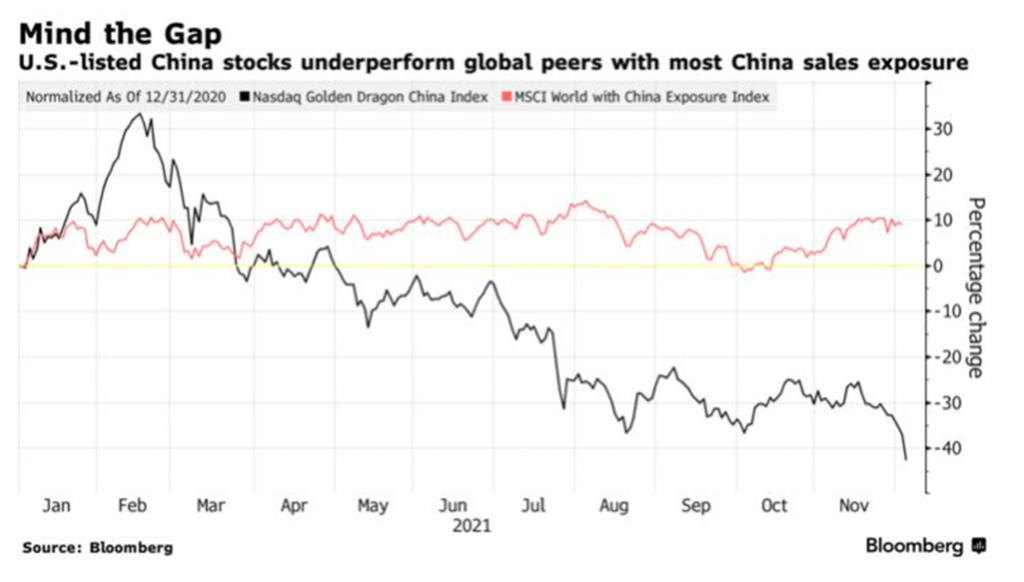

After the rule was announced, Nasdaq Golden Dragon China Index (which tracks China-exposed firms listed in the U.S) plunged 9.1% on Friday, adding further pressure to its YTD performance of -43%. The slump came amid a broader drop in equities on the day with China’s government ordering Didi Global Inc. to delist from the New York Stock Exchange as it is able to amass enormous amounts of data from hundreds of millions users both at home and abroad.

The move marked an expansion and escalation in a broader campaign to curb the growing power of internet titans which could someday threaten the Communist Party’s grip on power if given enough resources and influence. The regulatory crackdowns have chilled the global investment community and ratcheted up uncertainty. Investors will need to be more selective of the industries that can promote President Xi’s common prosperity that will fuel a more broad-based economic growth over the next few decades.

Chart Of The Week

Important Information and Disclosure

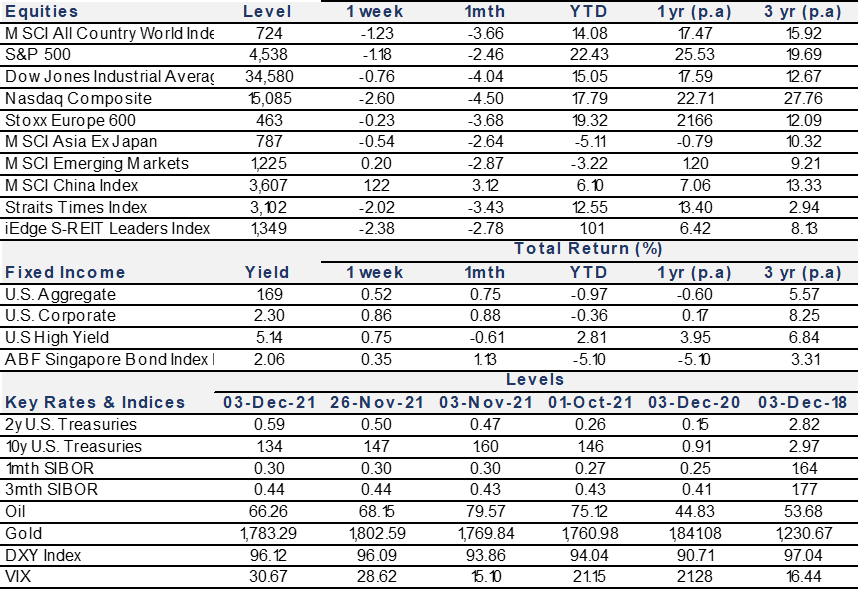

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total

return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.