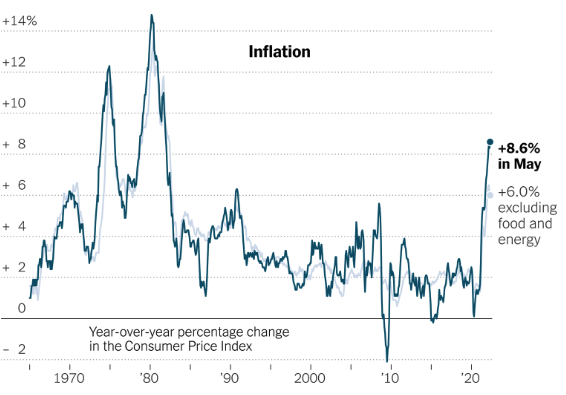

Still Running Hot

The closely watched inflation report released on Friday showed a re-acceleration of inflation, quashing hopes that inflation has already peaked and that the Fed could ease up on hiking rates. The Consumer Price Index (CPI), also known as headline inflation, came in at 8.6%. Russia’s invasion of Ukraine was continuing to push the prices of food and energy – the most volatile components of the CPI up. Costs for meat, eggs and wheat-based products like bread rose at the fastest pace since 1979, as measured by an index representing the price of food at home. Core inflation (the line in light blue below) moderated slightly, falling from 6.2% to 6.0%.

The differentiation between headline and core inflation is important as while the Fed wants to bring inflation down through demand moderation, it has pretty much no control over commodity prices and the demand for staples such as energy and food. A better measure for whether the Fed’s policies are working would be the core inflation (which excludes energy and food) figure, rather than headline inflation.

What does this mean for the Fed?

The S&P 500 lost ground on Friday, falling 2.9% after the release of CPI data to end the week 5.7% lower. Market participants got their hopes up that the Fed might ease up on large rate increases after delivering one in May. The CPI print is one of the last and perhaps most important data points the Fed will take into account before the rate setting meeting in the week of June 14-15th. The Fed has more incentive to stay on the current path and on course to deliver at least another 50bps increase at the next meeting. Powell has shown that he wants to guide expectations, rather than create additional uncertainty.

World Bank and OECD Lower Growth Forecasts

Following in the IMF’s footsteps, World Bank and Organization for Economic Cooperation and Development (OECD) cut forecasts for 2022 to 2.9% and 3%, lower than IMF’s estimate of 3.6% back in April. OECD represents 38 countries, most of them are the world’s most advanced economies. Unsurprisingly, inflation and war were main reasons cited for the cut. The World Bank expects emerging markets to experience the brunt of the setback, after dealing with the pandemic with less resources and now with food and energy insecurity.

Is it the 70s?

We have heard comparisons to the 70s, where the oil crisis led to rising interest rates and that resulted in a “lost decade” of stagnant growth. It goes without saying that the world is vastly different now but we wanted to outline just how different: firstly, global governmental institutions are now better equipped and positioned to manage this challenging situation. Secondly, most advanced economies are much less energy intensive, looking at the energy needed to generate growth. Despite the jump in energy prices, the magnitude and impact is still smaller than the experience in the 70s. Thirdly, the dollar is strong, as are corporate balance sheets, particularly those of large financial institutions. There will be continued challenges, as we saw this week where Oil, as represented by the West Texas Intermediate, surged past $123 a barrel, after seeming to stabilise a month ago.

Supportive Measures from China

Shares of Chinese internet companies, represented by KWEB, ended the week largely flat but gained more than 5% in the middle of the week. New gaming licences were suspended for many months but the National Press and Publication Administration (NPPA) announced the approval of 60 new game licences on June 7, making this the second batch of new gaming licences – possibly a signal that the crackdown on the tech sector is moderating.

China’s new loans rebounded to 1.9 trillion yuan in May after a drop in April, demonstrating that “Back to Normal” is gaining steam. The Chinese government has continued to shore up support for the slowing economy and to come as close to achieving its 5.5% growth target as possible. One of the many measures that are broadly supportive of the property market seeks to lower the barrier of entry for first-home purchases where the down payment amount was cut from 25% to 20%.

Earning Insights

We covered market moves here.

What’s Ahead?

Week of Jun 13, 2022:

All eyes on the FOMC meeting on June 14-15th. The Bank of England (BoE) and the Bank of Japan (BoJ) are due to update their monetary policy decisions too. China and US, running at different speeds, will share retail sales figures and industrial production data.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.