#LIBOR #FebJobReport #ChinaGrowth

Topic #1: LIBOR crosses 5% for the first time since 2007

The 3-month LIBOR (London Interbank Offered Rate) cracked 5% for the first time in 15 years on Monday, on account of the rise in expectations of Fed policy tightening. The LIBOR is a globally accepted benchmark rate at which major banks lend to one another in the international interbank market. An increase in LIBOR generally reduces the value of fixed income securities due to higher interest rates and borrowing costs.

Why did it happen?

The recent increase in LIBOR is largely driven by the recent congress testimony by Fed Chair Powell, which largely increased the probability of a 50-bps rate hike in the upcoming March meeting. The latest testimony has once again made it clear that the US Fed’s focus remains to bring down inflation levels by increasing interest rates, thereby cooling the economy and raising the cost of borrowing. Despite a current policy rate of 4.50 – 4.75% range, inflation has remained persistently high and is proving to be sticky.

Why should I care?

Equity markets have had a positive start to the year but the recent inflation numbers have brought some uncertainty which may negatively impact the market in the short-term. However, long-term investors should find these corrections as opportunities to enter the market and make fresh investments.

Topic #2: The US Job Report for February

The US released its job report for February this Friday. The actual job additions in the US came to about 311,000 which is quite stronger than 225,000 that was expected. The leisure and hospitality sectors added 105,000 jobs which was the most amongst all the sectors.

As shown in the chart below, the unemployment rate increased to 3.6% in February as compared to 3.4% in January. Additionally, the labor participation rate increased to 62.5% along with the average wage earnings increasing by 0.2% which was the slowest increase since the Fed started raising interest rates last year.

What can we expect going forward?

After Powell’s testimony on Capitol Hill, the market started pricing a 50-bps hike in the interest rates as the likely outcome in the upcoming Fed meeting later this month. However, Powell had mentioned that much of it depends on the February data that would come out.

This job report was a breather for the investors as even though the job additions showed strength, the increase in unemployment and the slower increase in wage gains implied slowing growth in the economy. This has made the market put back the possibility of a 25-bps increase in the interest rates on the table.

A lot will depend on the CPI and PPI data that comes out next week. If the inflation is higher than expected and does not show signs of cooling, the Fed is likely to go for a higher rate hike than expected.

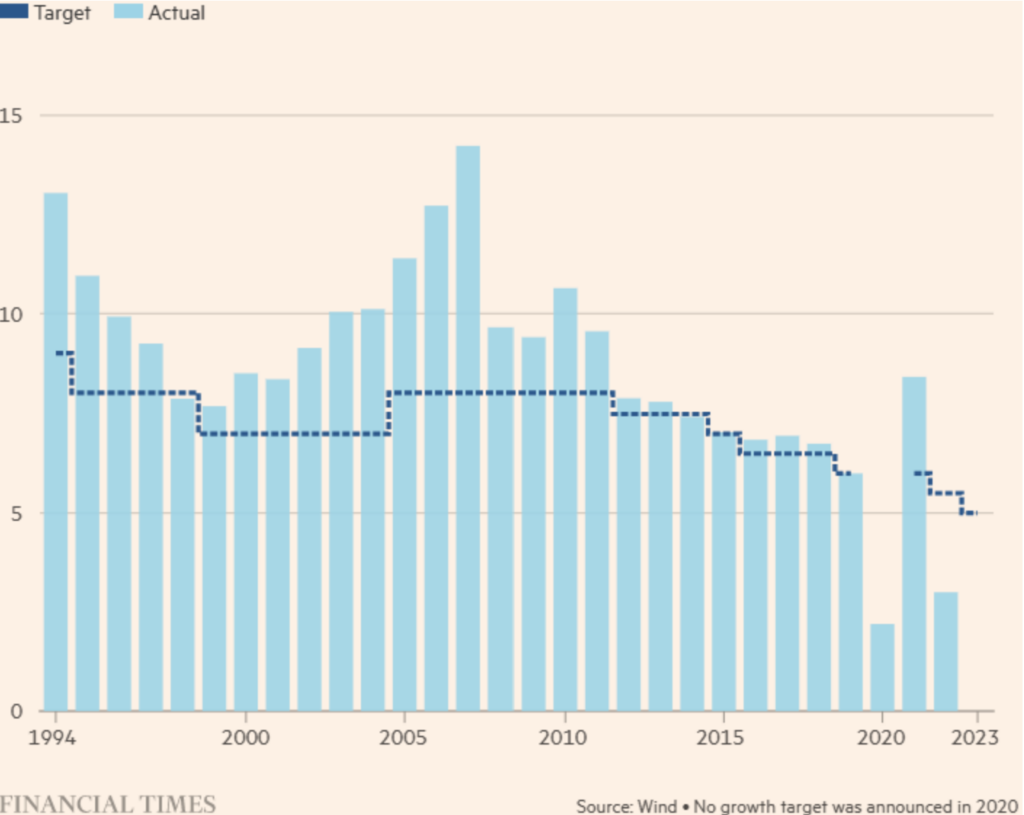

Topic #3: China’s Growth Forecast: Conservative or Realistic?

On 5th March, China released its growth forecast for 2023, setting a modest target of around 5%. The graph below shows the target and actual growth rates of China since 1994.

Historically, China has been known for always achieving its target growth as shown in the above chart. However, in 2022, Beijing missed the growth target that it had set at 5.5% by a large margin of 2.5%.

Despite having a positive start to the year, China’s markets did not perform as well in Feb and reversed all of its gains it previously made. Even after a U-turn from China’s zero Covid-19 policy, investors remain wary of Beijing’s previous stop-and-go approach, especially amidst a low vaccination rate in China, and have largely taken profits instead of remaining invested.

Regardless, unexpectedly strong manufacturing data in February, together with a rapid increase in consumer spending show strong rebound signs in the economy. The People’s Bank of China also has room to stimulate demand, thanks to its relatively low inflation, a key factor that other developed economies currently lack.

While transitional pain should be expected before economic activity moves towards normalcy, most analysts believe that China’s relatively unambitious growth target this year will likely be met. Whether there will be introduction of economic stimulus tools from policymakers remains to be seen still.

| Index | Level | 1 Week | 1 Month | From Jan 1 2023 |

| S&P 500 (US Stocks) | 3,861.59 | -4.77% | -6.66% | 0.98% |

| Nasdaq 100 (US Tech Stocks) | 11,830.28 | -4.17% | -5.38% | 8.91% |

| CSI-300 (Chinese Stocks) | 3,967.14 | -3.97% | -4.26% | 2.04% |

| Bitcoin (in USD) | 20,358.80 | -9.15% | -6.94% | 22.61% |

Source: Google Finance as of 11 March, 2023, Financial Times, Yahoo News

You must be logged in to post a comment.