Maybe this time it’s different?

Last week, we heard from Fed officials that it was too early to “pivot”, these comments fell on deaf ears as equities rallied, and this week’s inflation print of 8.5% continued to buoy markets. Investors are assessing whether a slowdown in inflation would prompt the Federal Reserve to reduce the pace of rate hikes and increase the likelihood of achieving a soft landing while bringing prices down.

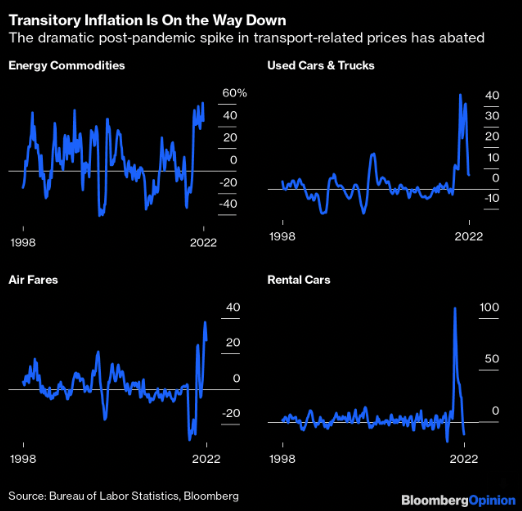

Headline inflation in the US abated slightly, down to 8.5% as compared to 9.1% in June, coming in below consensus and signalling that we may have reached peak inflation in June.

Looking under the hood, some of the components (energy, used cars, rental cars) that led to those eye watering figures are showing promising signs of abating. Most strikingly, rental car inflation, which once reached more than 100%, is now negative.

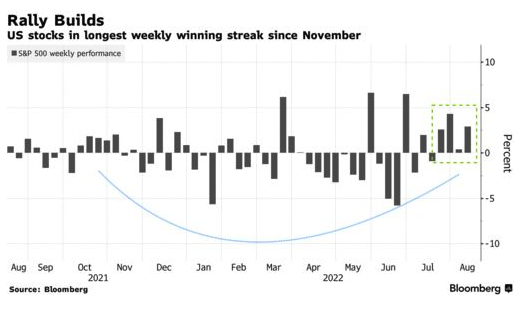

The S&P 500 ended up higher for the 4th week in a row. The “sell in May and go away” adage certainly did not hold up this time.

As we exit the summer months and head into the September FOMC meeting and US midterm elections in November, more market volatility could be expected as investors wait for clarity on where inflation and growth is headed.

It’s not too bad after all

Besides investors, consumers are feeling more optimistic too! US consumer sentiment rose to a three month high. A significant contributor to this could be the average price of gasoline has fallen over the last few weeks, and down to $4 a gallon for the first time since Russia invaded Ukraine.

Consumer sentiment is an important statistic to watch as roughly ⅔ of the US economy is driven by consumption.

Cars > Apartments

Official macroeconomic data from China is expected to show gradual improvement in key indicators in July as the country exited the most extensive lockdowns (since 2020) in Q2 2022. Chinese equities ended the week higher.

Automobile sales were boosted in July, as policies encouraged consumption through subsidies and tax cuts. In fact, GM and BYD sold more EVs than Tesla in China. Data from the National Passenger Car Information Exchange Association showed that passenger vehicle sales increased 41% year on year, as of July 2022.

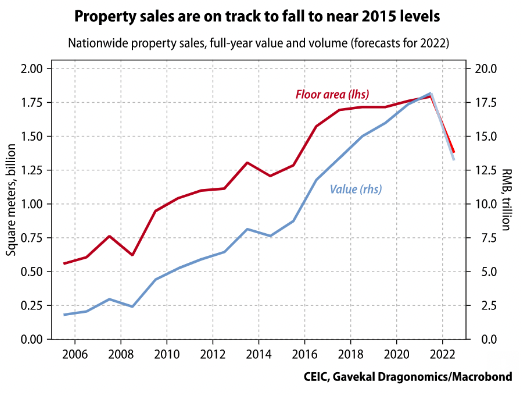

Property sales, on the other hand, continued to slump, falling to 2015 levels, according to Gavekal.

There are difficult issues to resolve on both the demand and supply side and there is no “silver bullet” solution. PBoC has eased policy, but so far it looks like it is not quite enough to slow the decline. Aggregate financing has slowed sharply, but the growth of M2, money supply, has continued – meaning that banks are flush with cash but are not making enough loans to consumers and businesses.

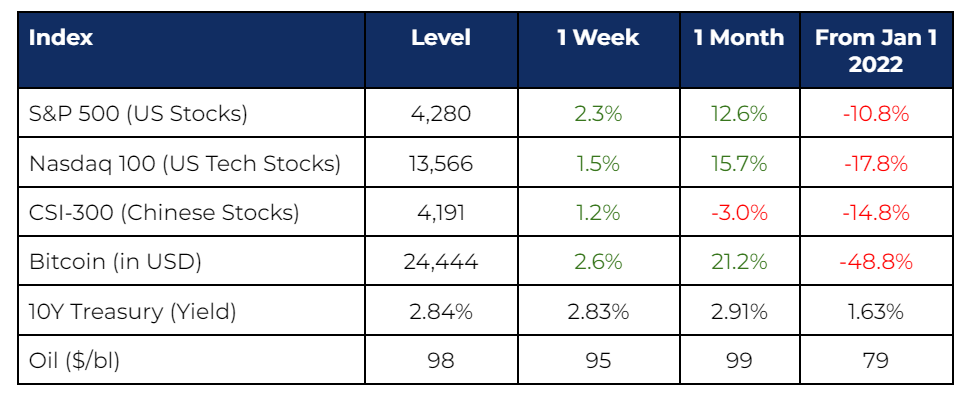

Market stats

Source: Google Finance, CNBC, as of August 12, 2022.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.