No surprises from FOMC Minutes

Minutes from the January FOMC Meeting show that participants agreed that the “current economic and financial conditions would likely warrant a faster pace of balance sheet runoff” This did not come as a surprise as inflation has spread into the broader economy, beyond sectors affected by the pandemic.

However, Mary Daly, president of the Federal Reserve Bank of San Francisco cautioned that the Fed should still be “measured” as history shows that “abrupt and aggressive action can actually have a destabilizing effect” on the growth and price stability the Fed is aiming to achieve.

US/Russia Tensions

Financial markets have been on a ride last week over developments in Ukraine. Possible sanctions against Russia and conflicting accounts over what is happening on the ground have increased uncertainty how this conflict could end. An escalation would roil financial markets. Russian equities fell 7.4% from Wednesday’s high to Friday closing after US officials discredited Russia’s claim of moving troops away from Ukraine. The S&P 500 fell 3% over the same period.

Russia is the third-largest producer of oil in the world after the United States and Saudi Arabia. Possible sanctions against Russia have fuelled fears that supplies of key commodities (Oil and energy products make up 63% of total exports) would suffer.

A diplomatic solution is still on the table as US Secretary of State Anthony Blinken is set to meet with his counterpart Russian Foreign Minister Sergei Lavrov next week.

Earnings Highlight

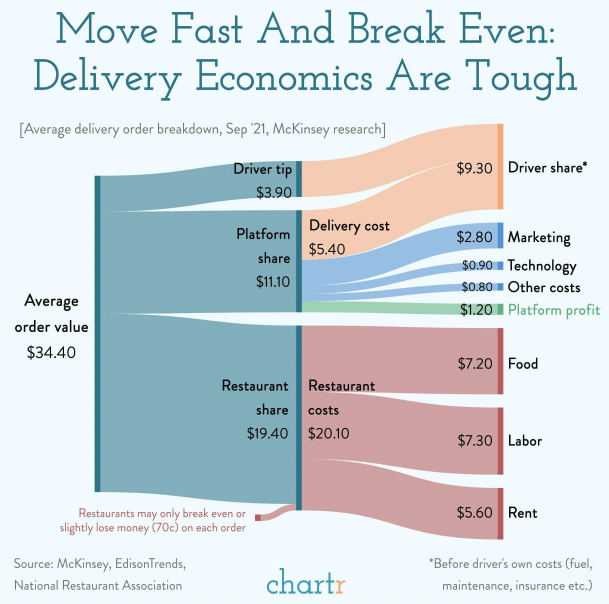

We covered market moves here and wanted to highlight DoorDash (DASH) which had been operating in a highly advantageous environment in the last two years. Now, with re-opening on track and rising inflation and wage costs, plus stiff competition from Uber Eats (UBER) and Grubhub (GRUB) on food deliveries and Walmart (WMT) and Amazon (AMZN) on last mile deliveries, companies like DoorDash could find it challenging to turn a profit.

This chart based on research from McKinsey shows thin margins in food delivery, particularly for restaurants that are just breaking even or losing some money on each order.

What’s Ahead

Many large cap companies are done with earnings for the quarter. Here are companies we are watching next week:

Alibaba (BABA): Alibaba is set to report earnings on Feb 24, 2022. BABA has fallen more than 50% from its peak in October 2020 and we could see a potential “bottom-fishing” on better-than-expected results.

Investors will be weighing current valuations against BABA’s slower growth trajectory due to regulatory and consumption shifts. Many analysts now believe that the stock’s valuation is cheap relative to its fundamentals citing that BABA’s free cash flow (FCF) margin is ahead of its US and Chinese peers.

However, this will have to be weighed against the backdrop of continued regulatory risk and deteriorating margins over the last two years due to tougher competition and investments in new but less profitable business lines.

Beyond Meat (BYND): Beyond Meat sells plant-based meat substitutes. It IPO-ed at $25 before surging to a high of $220 and is now trading at around $52 as the market has crushed valuations of once high-flying, unprofitable companies with lofty growth ambitions in the face of rising interest rates.

Beyond Meat sets out to address high meat consumption and its impact on climate change. Expectations for the company were extremely high two years ago. Now it has become less clear that Beyond Meat has or will capture a significant share of the global meat market. Given analysts are not expecting Beyond Meat to turn a profit this year, proof of growth sustainability will be key to near-term stock price performance.

Norwegian Cruise (NCLH): Norwegian Cruise Line Holdings is one of the largest cruise operators globally. It had a turbulent 2 years as cruise ships were seen as Covid-19 hotspots and borders were closed. Operating “Cruise to nowhere” services helped marginally. Profits were undoubtedly lower and operations became more complicated with additional measures and flexibility with cancellations. NCLH has high debt levels and ambitious plans for expansion – adding 40% more berths through 2027.

“Cruise to nowhere” services have gained a number of new customers who would not have considered going to a cruise holiday. With holiday bookings across the US and many European regions returning to pre-COVID levels the market will be looking for further signs of revenue recovery.

Important Information and Disclosure

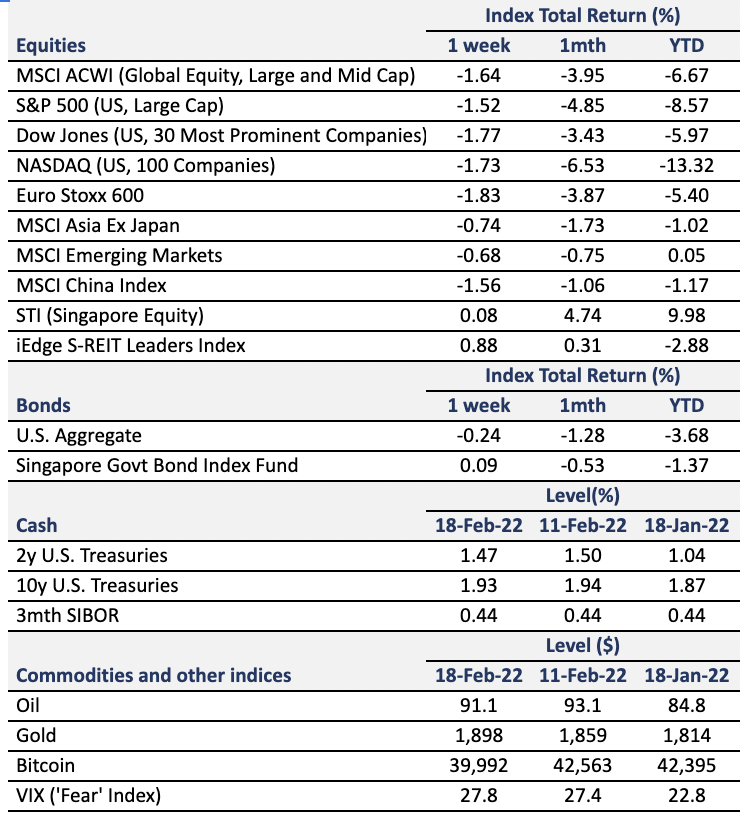

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total

return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.