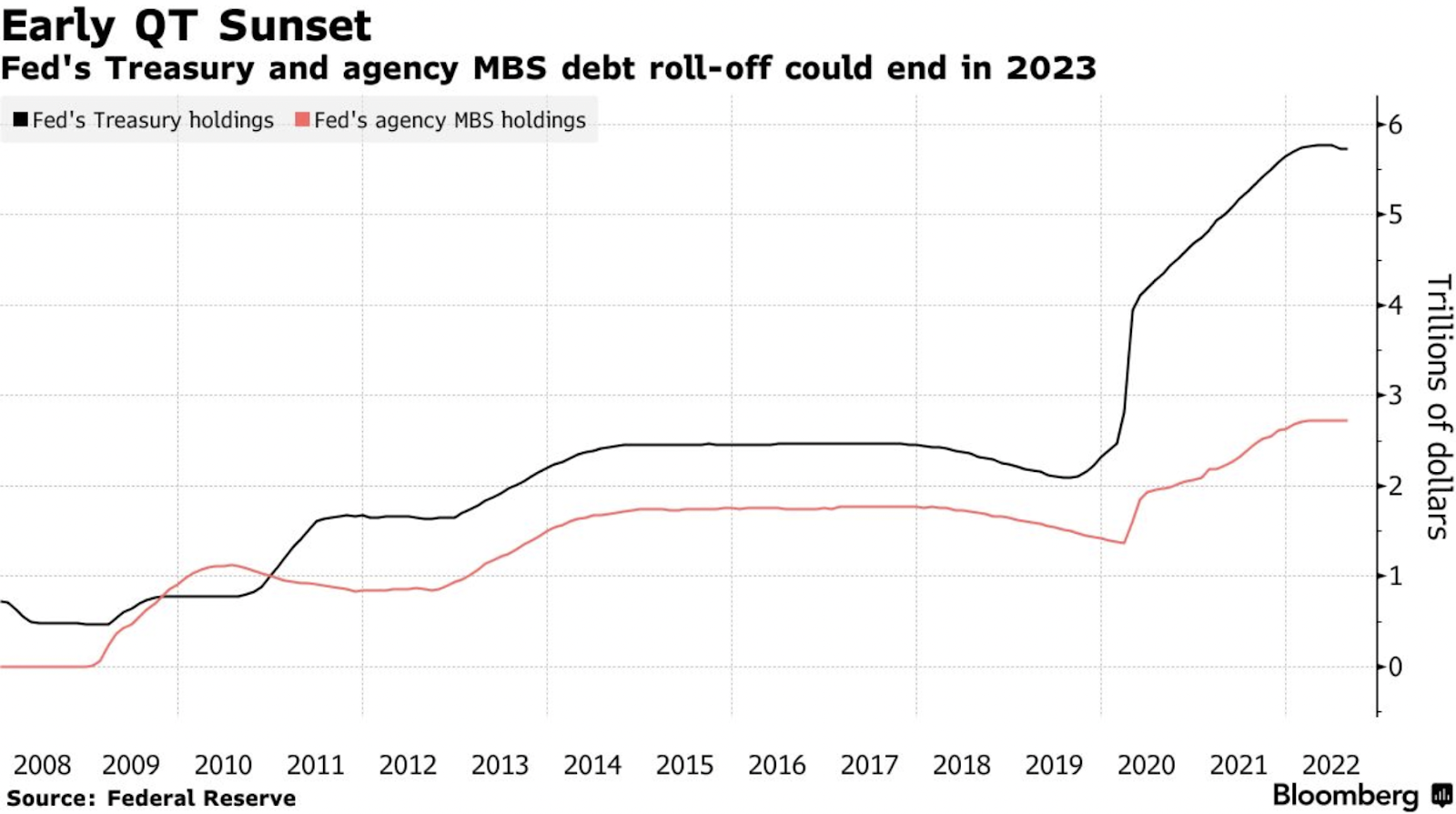

The Other Half of Quantitative Tightening (QT)

Besides rate hikes, the Federal Reserve has another tool to combat inflation: balance sheet runoff. Up to 60 billion of Treasuries and 35 billion of mortgage securities are expected to come off of the balance sheet, almost double the cap of the last time the Fed reduced its balance sheet.

Chair Powell expects this process to take “between two, two and a half years” for the balance sheet to get to a “new equilibrium”. Economists are now of the view that if the economy tips into a recession in 2023, the pace of balance sheet runoff could stall and the Fed may have to consider easing again.

The last time when balance sheet unwinding happened in 2018, stocks slid as market participants were worried that the Fed was draining liquidity too quickly. This time, there is more consensus that this has to be done and perhaps even more needs to be done given the relatively bullish sentiment lately, signalling that financial conditions have not tightened as much as the Fed might have liked.

Bear Market Bounce or Bull Market?

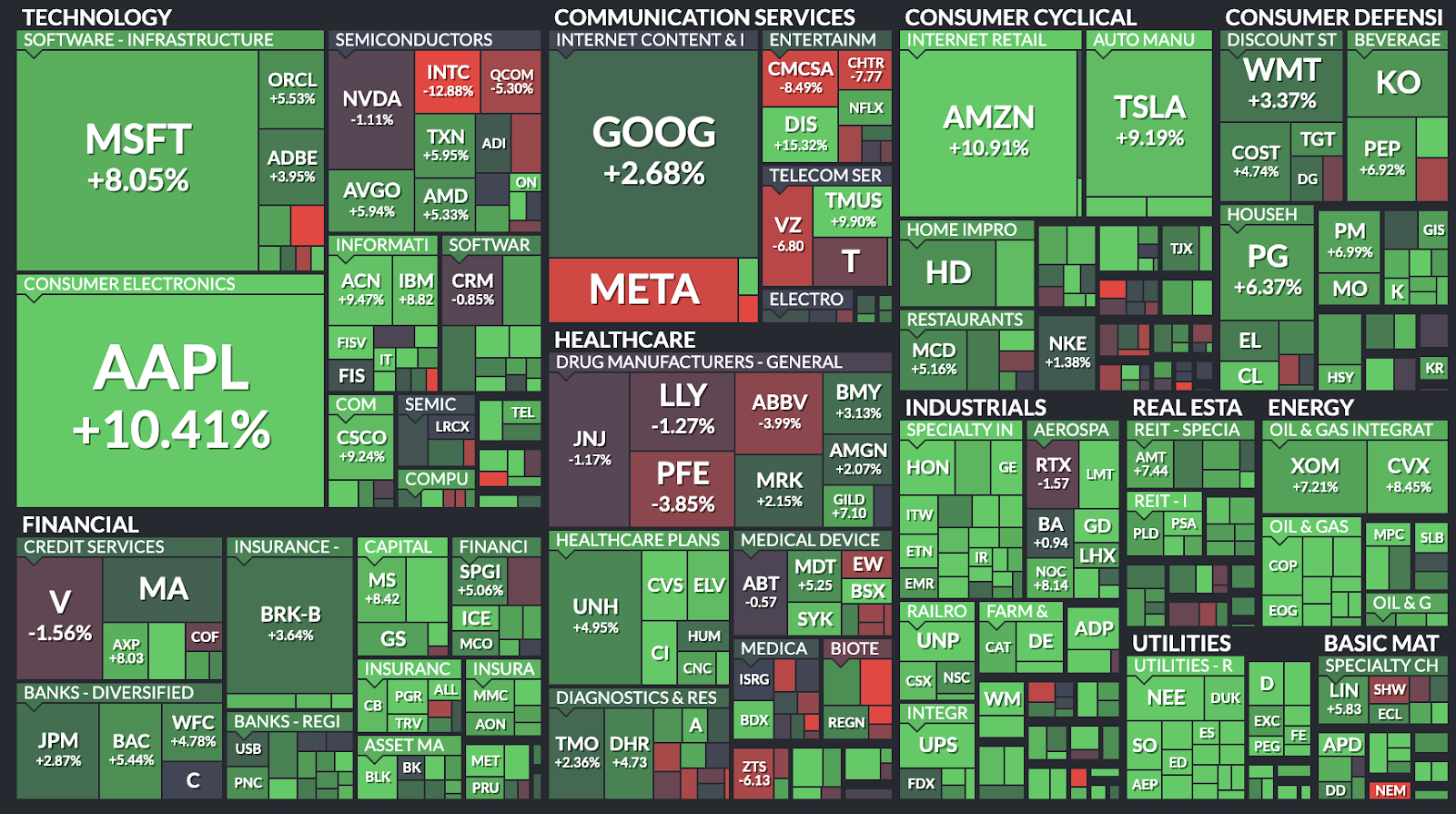

There has been much chatter whether we are in a bear market bounce or the beginning of a new bull market. The S&P 500 broke its four week winning streak this week, ending 1% lower.

Read more: Bear Market Rally Or New Bull Run: What Should Investors Do?

Still in the last month, the rally in US stocks has been broad-based across various sectors, as shown below.

The bottomline: As we exit the summer months and head into the September FOMC meeting and US midterm elections in November, more market volatility could be expected as investors wait for clarity on where inflation and growth is headed.

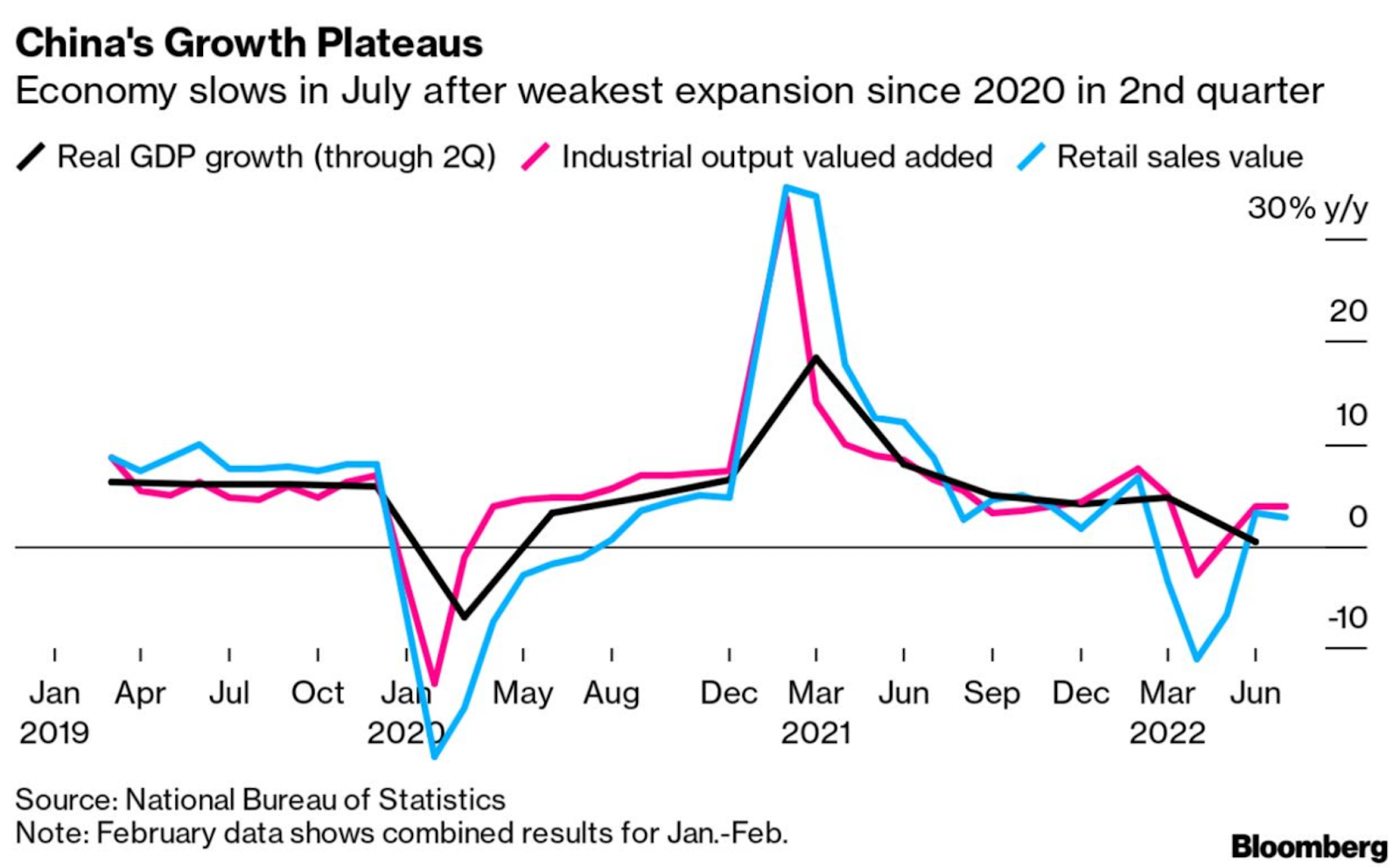

Not coming up close to 5.5%

As expected, Chinese retail sales, direct investments and industrial output data showed a slowdown down in July. Consensus puts 2022 GDP growth at 3.8% currently.

Besides falling real estate sales, potential debt issues and mortgage boycotts, China’s manufacturers are also dealing with a potential slowdown in new factory orders. We will be looking at how the Chinese government will continue to stimulate the economy – particularly as we come closer to the National Congress later this year.

The bright spot has continued to be auto sales, and electric vehicles in particular – a boon for consumption and also for the related high tech manufacturing sector.

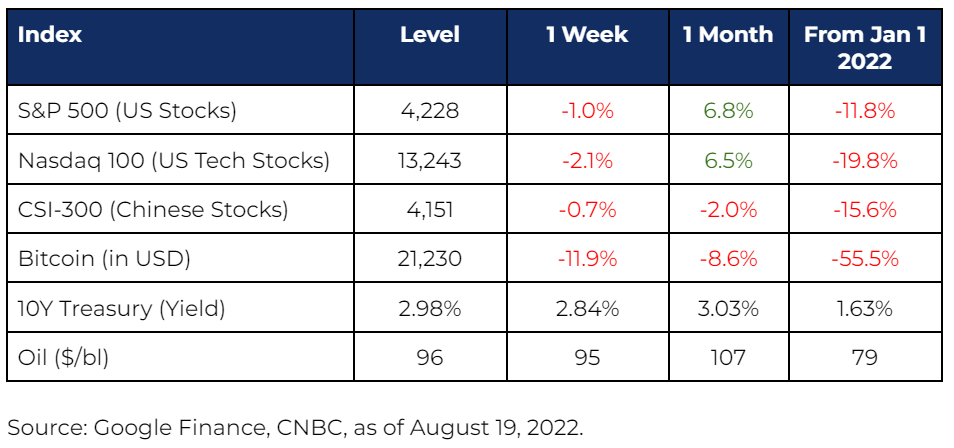

Market Stats

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.