Peak Inflation?

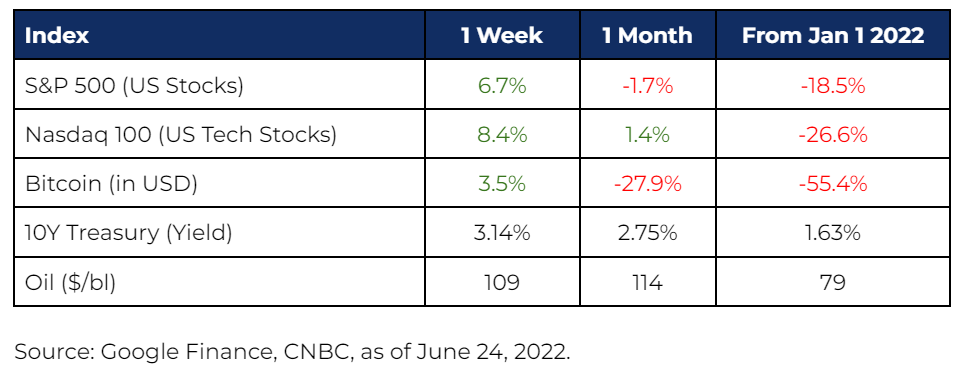

Markets rallied on Friday, S&P 500 gained 3%, ending the week almost 7% higher as recessionary fears receded slightly. Even with the gains, the S&P 500 is still down 18% year to date.

The latest consumer inflation expectations came in lower, settling lower than the 14-year high. The survey, from the University of Michigan, said consumers expect the prices to rise by an average of 3.1 percent over the next five to 10 years. Inflation expectations are generally used to gauge consumer behaviour – rising inflation may make consumers think that prices could be higher in the future, so they will front-load their consumption and demand higher wages, thereby contributing to even higher inflation rates.

Federal Reserve Bank of St. Louis President James Bullard said fears of a recession are overblown, while Chair Powell acknowledged that it is proving to be increasingly challenging to engineer a soft landing.

Soft-ish Landing?

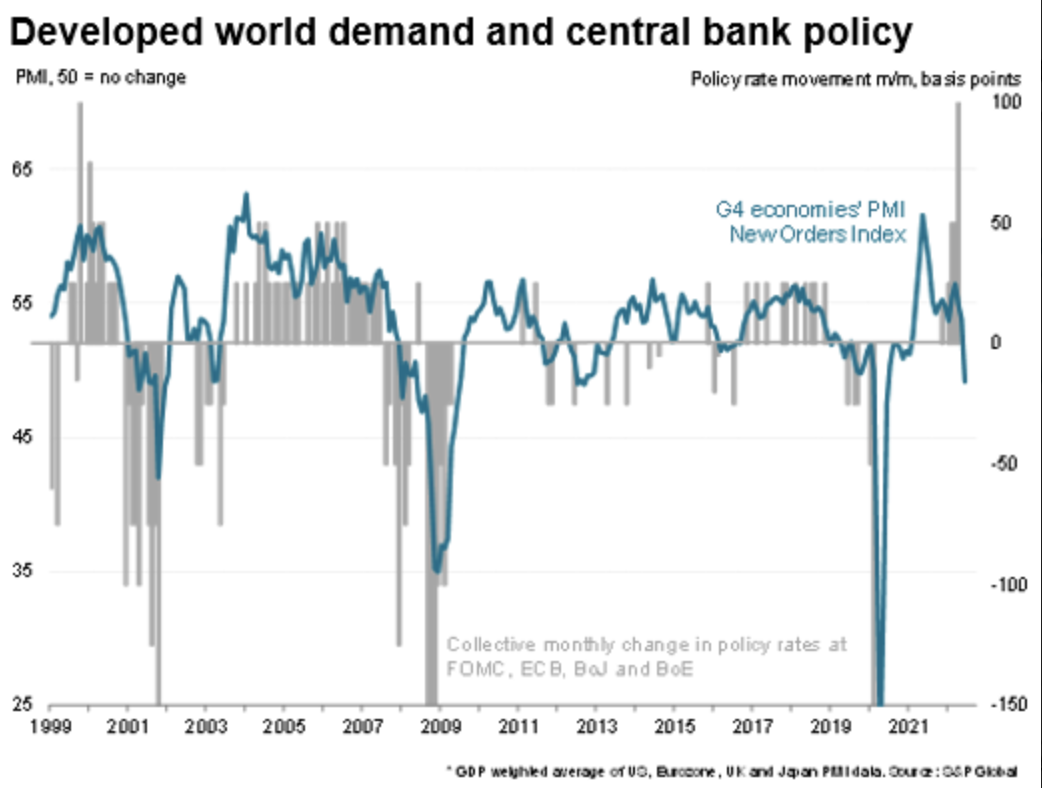

Multiple PMI readings from developed economies showed that new orders declined for manufacturing. This fall could be driven by higher interest rates, energy insecurity, Chinese lockdowns and Russia’s invasion of Ukraine.

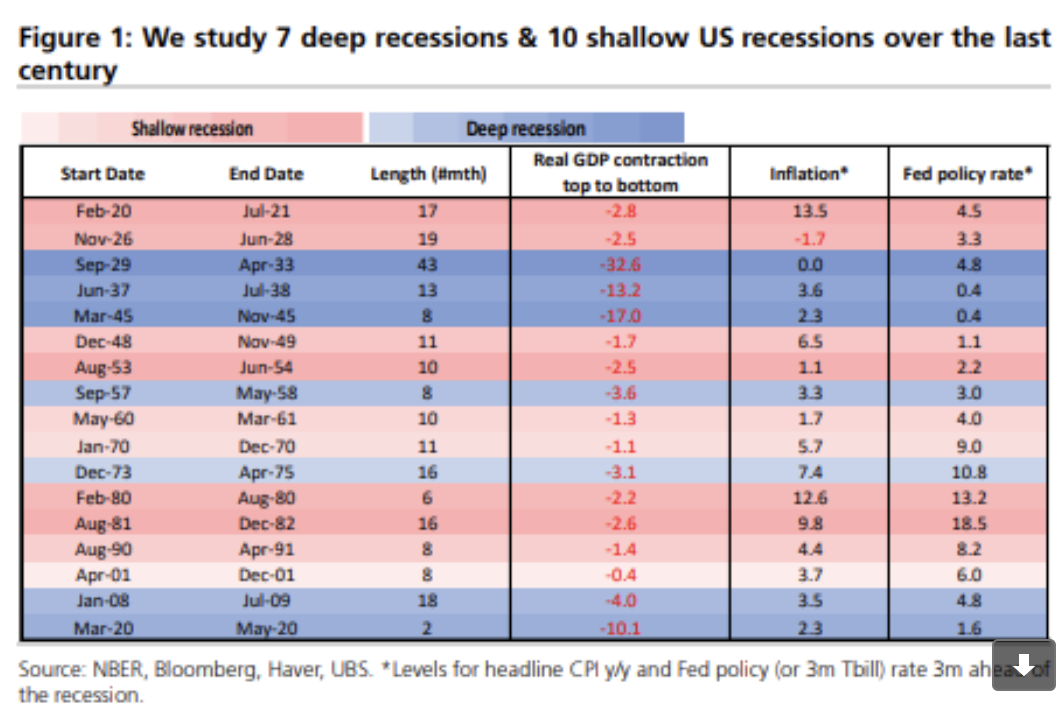

Analysts at UBS looked at US recessions in the last 100 years and categorised them as shallow (US GDP fell by 3% of less) or deep recessions (US GDP fell by more than 3%). Shallow recessions were often associated with central banks raising interest rates – a situation we’re currently facing.

Data shows that in a shallow recession, markets fall by about 11% on average and bottom out about 4 months after the start. In a deeper recession, markets tend to fall about 24% and bottom out about nine months from the start.

Given that the labour market remains robust, even if the US economy were to head into a recession, evidence suggests that it could be a shallow one.

Bulls in China

The Chinese equity market fared well too, with internet companies, represented by Kraneshares CSO China Internet ETF (KWEB) leading the charge and gaining 4% over the week. Since March, when many of these stocks bottomed, Pinduoduo shares have more than doubled, while Meituan is up 80%, followed by JD.com and Kuaishou that are up close to 50%.

The shopping festival 6.18, hosted by JD.com saw slower growth but highlighted new consumer behaviour (live streams, greater interest in household appliances and outdoor gear). Despite slower growth, sales volumes were still 10% higher. The next large shopping event to watch would be 11.11, but Alibaba, the largest ecommerce player, does not disclose figures.

Electric vehicle sector got a boost from a State Council meeting chaired by Premier Li Keqiang, who reiterated support for the sector and extension of tax breaks for new electric vehicles.

Earning Insights

We covered market moves here.

Market Stats

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.