Strong Hiring Continues

The US economy added 390k jobs for the month of May, a strong showing despite three 0.25% rate hikes. The unemployment rate remained at 3.6%. In pre-pandemic times, a figure above 200k was regarded favourably. This also means that the Fed will likely continue on its current glide path of hiking to show down the economy without causing a recession. As we head into the summer travel season, the Leisure and Hospitality sector recorded the most gains.

The S&P 500 lost ground on Friday, falling 1.6% after the release of payrolls to end the week 1.2% lower. Market participants got their hopes up that the Fed might ease up on large rate increases after delivering one in May. Lael Brainard, the Fed’s vice chair, said that the Fed still “had a lot to do” and that it was “hard to see the case for a pause” on rate hikes in order to bring inflation down to its 2% goal.

In the right direction, but too soon to tell

Average hourly wages rose 0.3% in May, the same level as in April and 5.2% higher than a year before. This is a slight moderation as compared to 5.5% in April. There are still nearly two job openings for each person seeking employment, but the total number of vacancies have started to decline. Looking at data collected by the Labour Department on the last business day of April, employment gaps are the widest in the services sector, where consumers have or will shift their spending with the lifting of pandemic restrictions. In the Leisure and Hospitality sector, the vacancy fell from 9.7% to 8.9% in April.

Hurricanes?

Pessimistic comments from top brass at JP Morgan, Wells Fargo, BlackRock and Morgan Stanley sent markets down on Tuesday when they spoke at an investor conference. Factors such as business confidence, consumer confidence, inflation, rising cost of capital and inputs, as well as unprecedented factors like the war in Ukraine are causing a storm that could be a “minor one or [a] superstorm”.

Their comments are generally used to guide analyst earnings expectations for the coming quarters. When markets are down, large banks typically expect to see less revenue from higher margin activities like investment banking (IPOs, underwriting etc.), even if consumer banking remains relatively stable, however during periods of market volatility, trading revenue is expected to increase.

Released and Revenge Spend

Shanghai, the economic hub of China, announced the end of their two-month long lockdown this week, taking a step towards the return to normalcy. Shanghai residents were seen engaging in ‘revenge spending’. Many went on shopping sprees with snaking queues forming outside shopping malls, suggesting an inevitable retail bounce-back.

Shares of Chinese internet companies, represented by KWEB, advanced 5.5% and Chinese stocks overall (MSCI China) advanced 3.4% for the week. Accompanying this news, officials also unveiled the Shanghai Action Plan to Accelerate Recovery and Revitalization of the Economy to eliminate unreasonable restrictions on enterprises’ resumption of work, production and business. More details emerged about the state plan to support the Chinese economy. Most policies initiatives were expansions of previous support measures, such as tax relief, subsidies, as well as increased investment and infrastructure spending – supporting specific industries like automobiles, technology platforms and property development.

Earning Insights

We covered market moves here.

The Q1 earnings session has concluded and unsurprisingly, inflation and supply chain concerns appeared frequently as headwinds. Business sentiment worsened and analysts started to cut down Q2 EPS estimates for companies in the S&P 500. Q2 earnings are expected to grow at 2.1%, as compared to 9.4% a year ago. It is worth pointing out that 6 sectors enjoyed positive earnings revisions: Autos, Basic Materials, Construction, Consumer Staples, Energy, and Transportation.

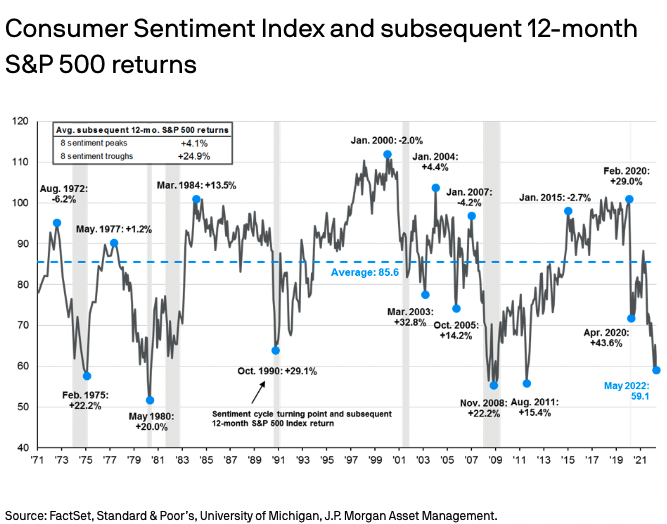

In the last few months, it is undeniable that consumer sentiment has taken a significant hit. The chart below shows that during periods where consumer sentiment is at its lowest, in the subsequent 12 month period, the S&P 500 returned just under 25% on average.

When investors were similarly or more pessimistic than they are now, for example during the oil crisis in 1970s, high inflation in the 1980s, the Great Financial Crisis in 2008 and when the US was downgraded to AA by S&P over debt ceiling concerns, the S&P 500 still made significant double-digit gains in the subsequent 12-month period.

Where could markets go from here?

Risks to growth have increased lately but the worst case scenario has not materialised. Companies and households are entering this next stage of the economic cycle with good fundamentals and strong balance sheets (and wide profit margins vs. historical levels for many corporations).

While growth may be held back by persistent inflationary pressures in the short term, investors can take a diversified approach: seeking balance between value and growth, and US and international. During times of market volatility, it becomes even more important to pay greater attention to the things one can control: diversification, asset allocation and cost.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.