#USRating #AMZN_AAPL #ChinaPrivateSector

Fitch downgrades United States, but no major impact anticipated

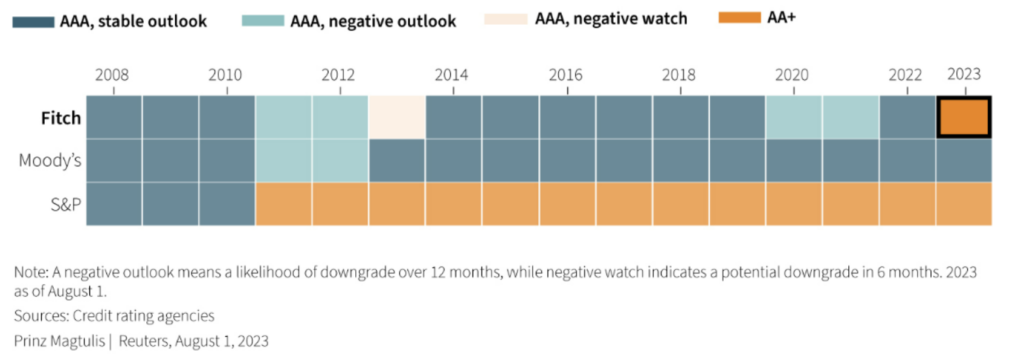

US credit ratings from various agencies

What Happened?

In a significant move, Fitch Ratings, one of the major credit-rating agencies, downgraded the United States government’s credit worthiness from AAA to AA+. This decision marks the second time in recent years that the country’s top-tier credit rating has been lowered, with Fitch citing mounting debt levels and political challenges in tackling spending and tax policies as the primary drivers behind the downgrade.

Why did it happen?

The downgrade comes on the heels of a recent resolution between the White House and Congress, temporarily suspending the government’s borrowing limit and enacting about $1.5 trillion in spending cuts over the next decade. Fitch’s assessment underscores the expected decline in fiscal health over the next few years, emphasizing the growing burden of general government debt and a weakening governance environment when compared to nations with similar debt ratings.

Implications for the investors

While concerns might arise about potential negative consequences for financial markets and borrowing costs, experts indicate that the impact on investors is likely to be limited. Fitch’s move is expected to have minimal effect on the interest rates the U.S. government pays, as major pension funds and investment vehicles are not solely bound to holding triple-A rated securities.

The size and stability of the U.S. economy, along with the extensive reach of its government bond market, mitigate the need for undue reliance on credit ratings. Consequently, investors are not anticipated to significantly adjust their holdings of U.S. Treasury securities due to the downgrade, and regulatory requirements for large banks to hold Treasurys are expected to remain unchanged.

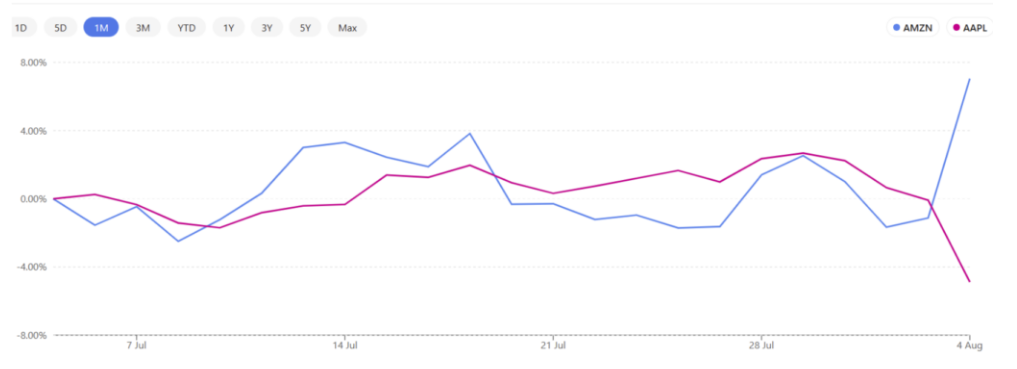

Amazon and Apple beat earnings expectations for Q2

Source: Amazon and Apple comparison chart (Google Finance)

Amidst the busy earnings week, tech giants Apple and Amazon delivered robust earnings reports. Apple (AAPL) exceeded expectations for fiscal Q3 earnings, beating estimates by $1.26 per share, with revenues of $81.8 billion — a slight YoY dip but surpassing projections.

The company’s Services segment stood out, boasting an impressive +8% YoY growth to $21.21 billion. Though iPhone sales slightly missed estimates at 39.67 million units, analysts predict a return to revenue growth in fiscal Q4. Despite concerns about Apple’s relative absence in the AI realm, its performance reaffirms its steadfast market presence.

Meanwhile, Amazon (AMZN) outperformed predictions across the board. The company reported earnings of 65 cents per share, well above the Zacks consensus of 34 cents, and generated revenues of $14.4 billion, surpassing expectations. Amazon Web Services (AWS) demonstrated a +12% YoY growth, amassing $22.1 billion in revenue.

The company’s forward guidance projects Net Sales of $138-143 billion for the next quarter, with Operating Income anticipated to reach $5.5-8.5 billion. This strong performance propelled Amazon shares up by over +6%, marking a notable rise from recent levels.

As both Apple and Amazon continue to exhibit resilience and adaptability in their respective sectors, investor focus remains on these industry giants. While Apple’s Services growth and Amazon’s impressive earnings uplift sentiment, market participants are keenly awaiting further insights on Apple’s AI initiatives during the conference call. Additionally, Amazon’s robust outlook and share price surge indicate optimism surrounding the e-commerce behemoth, suggesting a potentially upward trajectory in the coming months.

China boosts support for private companies, leading to surging stock prices

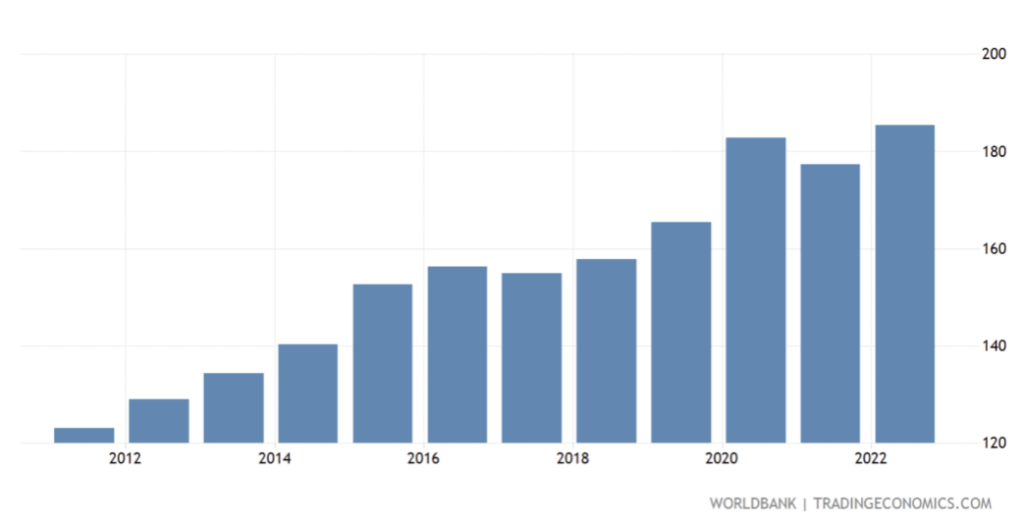

China Domestic Credit to Private Sector (as a % of GDP)

In response to a weakening economic momentum, China’s central bank governor, Pan Gongsheng, has affirmed a commitment to direct increased financial resources towards the private economy. During a meeting with representatives from diverse sectors including property, aluminum, and agribusiness, Pan announced the forthcoming release of guidelines aimed at bolstering support for private firms.

Notably, the People’s Bank of China (PBOC) plans to broaden bond financing channels and expand debt financing tools, referred to as “the second arrow,” launched in 2018 with PBOC refinancing.

Pan emphasized the importance of nurturing private firms as a key component of supply-side structural reform in the financial sector. The PBOC aims to cultivate a conducive environment for the growth of private businesses, encouraging financial institutions to adopt a proactive stance in facilitating development and lending.

This commitment aligns with China’s recent policy measures unveiled last month, aimed at alleviating challenges faced by private businesses, particularly in light of the dual impacts of COVID-19 restrictions and a regulatory clampdown spanning various sectors.

To further instill confidence within the private sector, economic planners have conducted several engagements with private firms to comprehend operational hurdles. This move is part of a broader initiative, as the Chinese cabinet recently called on the public to report hindrances to private economic growth.

As China seeks to stabilize its economy amid evolving challenges, the central bank’s commitment to channeling financial resources into the private economy is poised to provide a renewed sense of support for private firms. The expansion of debt financing tools and broader bond financing channels is anticipated to invigorate economic activity, potentially aiding the recovery of sectors such as property that have been grappling with debt-related concerns.

Source: Google Finance, Bloomberg, Yahoo Finance, CNBC, Financial Times, Reuters, Business Times, CNN, Fashion United

You must be logged in to post a comment.