The content of the article is provided by PIMCO.

Are you seeking a reliable source of income amidst the current market volatility? Bonds might be the perfect answer, even if their 2022 performance has left you somewhat sceptical. In this article, we tackle some common reservations around investing in bonds and reveal why now is an excellent time to embrace the opportunities they offer.

Reservation 1: Bonds underperformed in 2022 and there’s still a lot of market uncertainty. Why should I invest in them now?

Bonds faced a tough year in 2022, but this was an outlier in the broader context of market history, where bonds have played a key role in portfolio diversification.

While it’s true that bonds faced a tough year in 2022, Chart 1 shows this was an outlier in the broader context of market history. It’s rare for stocks and bonds to both have negative returns in the same year. It’s also worth noting that over the past 30 years, global bond market declines have been smaller and rarer than stock market declines. Therefore, rather than basing your bond return expectations on the anomalous experience of 2022, investors should consider 2023 bond returns as more reflective of bond performance when starting yields are already elevated.

Over the long term, bonds have played a crucial role in portfolio diversification, typically helping to mitigate volatility, and they remain a key component of a well-diversified portfolio. They can act as a buffer during times of volatility, and with higher yields now available, they offer a compelling income proposition. Additionally, if interest rates were to decline, the value of bonds purchased at current yields would increase, providing a dual benefit of income and capital appreciation. While the value of bonds could fall somewhat if central banks were to hike rates, returns are likely to remain positive even with modest further increases in rates.

Reservation 2: Time deposit rates are really attractive right now. Why shouldn’t I take advantage of them?

If your funds are tied up in a time deposit, you might miss the chance to secure current higher bond yields and the related potential for price appreciation.

It’s true that time deposit rates are appealing at the moment and it’s understandable that investors are drawn to them, given they are viewed as safe investments and are offering higher returns today compared to the near-zero rates from a few years back. However, while there are many valid reasons for wanting to hold some of your portfolio in cash, it’s worth considering whether or not you can redeploy some of that for improved portfolio efficiency over the longer term.

Currently, bonds are offering some of the most attractive yields we’ve seen in a decade, and these opportunities may not last. Even if rates rise slightly, the higher interest payments you receive can help offset decreases in bond prices. And if rates fall, you’re already locked in at the higher rate, which could increase the value of your bonds. This approach is about playing the long game, focusing on steady income and the potential for growth, rather than trying to outguess the market’s every move.

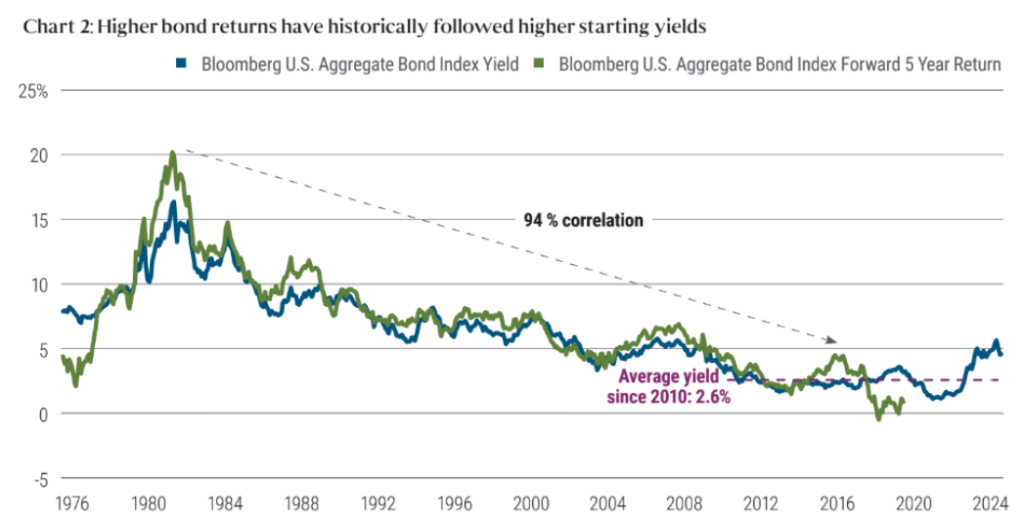

Chart 2 shows that there’s historically been a 94% correlation between the yields at the time of bond purchase and the five-year return on those bonds. In other words, the higher the yield you lock in now, the greater the potential for your investment to accumulate returns over time.

If your funds are tied up in a time deposit, you might miss the chance to secure these higher bond yields and the accompanying potential for price appreciation. While there is no guarantee that the correlation between starting yields and 5 years returns will persist in the future, it may be worth considering a more flexible approach that allows you to respond to changing market conditions and take advantage of diverse investment opportunities as they arise.

Reservation 3: I’m waiting until the Fed starts cutting rates before I invest in bonds again.

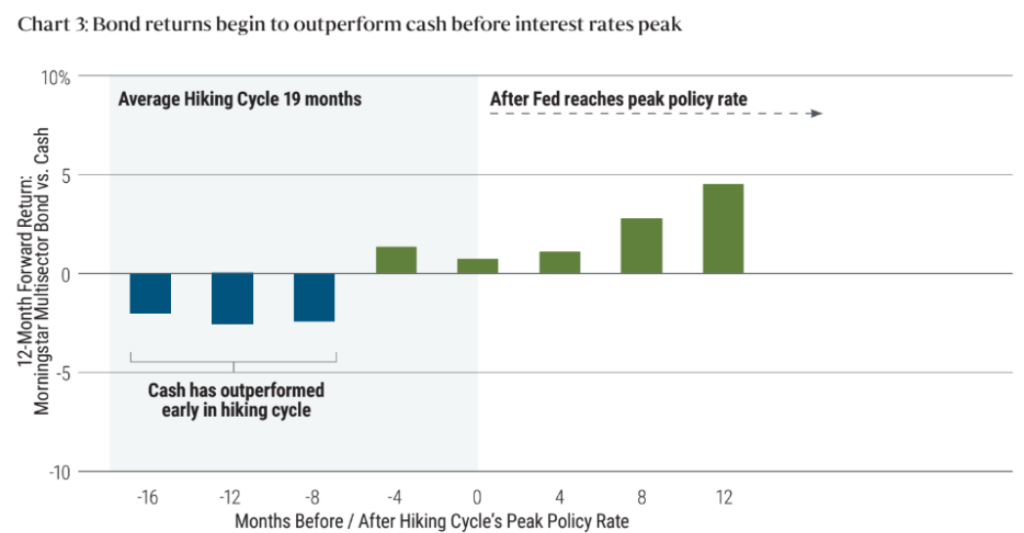

Timing the market is notoriously difficult, and waiting for rates to peak can result in missed opportunities.

Historical trends indicate that the gains in fixed income markets often begin to occur before, not after, interest rates have peaked. If you wait for the perceived perfect moment, you risk missing out on the period of strongest performance for bonds. Chart 3 shows that bonds underperform cash while rates are rising but start to turn positive around four months before peak rate is reached. They turn really positive around 8 months after the peak is reached.

With the growing consensus among financial experts that inflation – and consequently interest rates – may have peaked, some investors may want to consider the benefits of investing in bonds now rather than trying to time the market.

Investing in bonds now, amidst market uncertainty, can be a strategic move for long-term investors. It’s about looking beyond the recent past and focusing on the role bonds can play in achieving financial goals over the decades.

Speak to our dedicated advisory team to understand more about investing in bonds.

Disclaimer: This material contains the current opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2024, PIMCO

You must be logged in to post a comment.