By now, you should have seen the headlines. The Federal Reserve has raised US interest rates by another 0.75% and vowed to keep hiking rates for longer.

Need a quick lowdown on what’s happening? We’ve got you covered.

- The September rate hike

- Will interest rates continue to rise?

- The Fed dot plot, explained

- Is a recession coming?

- Why did the stock market fall?

- How will Singaporeans be affected by the rate hikes?

1. Another jumbo rate hike

On Wednesday, the Federal Open Market Committee (FOMC) raised benchmark interest rates (also known as the federal funds rate) by another 0.75%, its third straight rate hike of this magnitude.

The move is intended to combat inflation, which is now at a 40-year high in the US and running at more than three times the Fed’s 2% inflation target.

The Fed’s benchmark interest rate – which is what banks charge each other for overnight loans – is now at a range of 3% to 3.25%, the highest level since the 2008 global financial crisis.

For a sense of how quickly the rate has climbed this year, the federal funds rate was set at near-zero as recently as March 2022.

2. Will the Fed raise interest rates further? By how much?

Fed projections indicate that officials expect to raise rates by at least 1.25% during the remaining two policy meetings of 2022. This suggests that another 0.75% rate hike could be possible at the November FOMC meeting, followed by a 0.50% hike at the December meeting.

Based on the Fed’s dot plot, the central bank is likely to keep raising interest rates well into 2023, and rate cuts are not foreseen until 2024.

“The FOMC is strongly resolved to bring inflation down to 2%, and we will keep at it until the job is done,” Fed Chair Jerome Powell declared during his press conference.

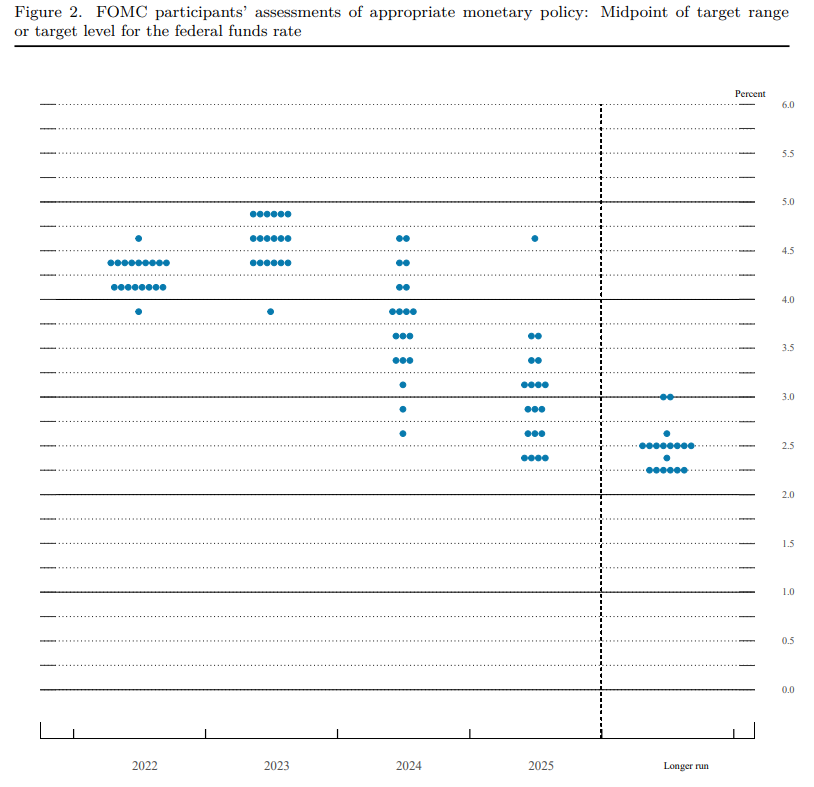

3. Wait… What is the Fed dot plot?

The dot plot shows the Fed’s outlook for the path of interest rates going forward. Each “dot” represents where each Fed official thinks the rate should be.

Here’s how to read the dot plot.

- The median forecasts show that Fed officials expect interest rates to hit 4.25% to 4.5% by the end of 2022

- By the end of 2023, rates are expected to climb to 4.50% to 4.75%. (This is a jump from the June dot plot which projected rates to rise to 3.8% by end 2023)

- For 2024, projections are more dispersed. Fed officials predict rates to be somewhere between 2.75% to 4.75%

- In the longer run beyond 2025, most officials expect interest rates to settle at 2.5%

In essence, the Fed is saying that interest rates are going to stay elevated for longer – at least until 2024.

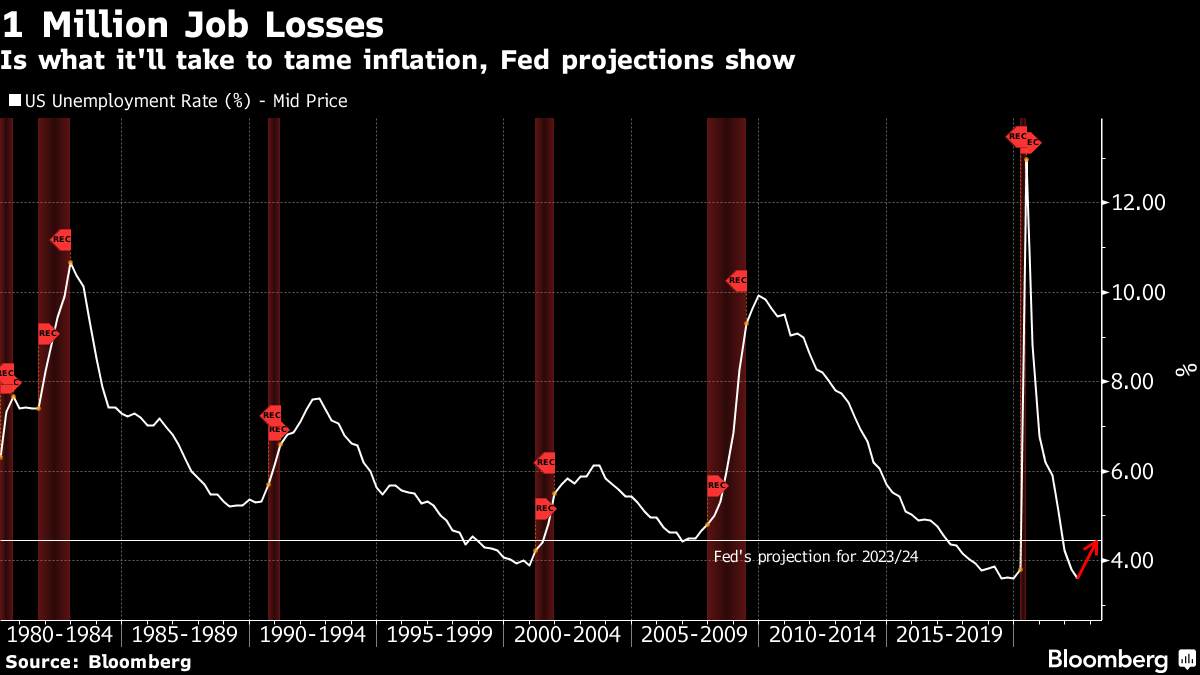

4. Will there be a recession?

The aggressive rate hikes could increase the odds of a recession happening, but it seems that is a price the Fed is willing to pay to crush inflation.

“We have got to get inflation behind us. I wish there were a painless way to do that. There isn’t,” Powell said in his press conference.

The Fed’s higher unemployment forecasts is yet another indication of their resolve. The new projections show unemployment rates rising to 4.4% by the end of 2023, up from 3.9% predicted in the June forecast.

At present, US unemployment sits around 3.6%. A jump to 4.4% would meet the “Sahm Rule” for identifying the start of a recession, according to Bloomberg economists. Plus, it could mean job losses of more than 1 million.

Although that’s a tough pill to swallow, taming inflation ultimately means the economy has to slow.

To do that, the Fed needs to push interest rates higher. The idea is that as consumers and businesses spend less given higher borrowing costs, demand begins to wane, the economy cools, hiring and wage growth slows, and price increases moderate.

5. Why did the stock market drop after the Fed’s rate hike?

On Thursday (22 September), the major US indices slid for the third consecutive day amid mounting fears of a recession. Growth and tech stocks took a hit, but defensive stocks outperformed with drugmakers and consumer staples in the green on Thursday.

Generally speaking, growth and tech companies (especially those that are not profitable yet) are particularly vulnerable to high interest rates. That’s because they are valued on their future earnings estimates, but the present value of those future earnings are worth less when interest rates rise.

6. How will Singaporeans be affected by rising interest rates?

Interest rates in Singapore closely track interest rates in the US. Higher interest rates mean that Singaporeans could find their car loans and home mortgages becoming more expensive.

But higher interest rates also mean that your cash savings can work harder for you. Cash management accounts like Syfe Cash+ have already started raising their projected returns, and will continue adjusting them higher as interest rates climb. In fact, Syfe Cash+ has again raised its projected yield to 2.4% p.a. from 1.9% p.a.

Although fixed deposit rates have also risen in recent weeks, you’ll be locked in at that rate for the duration of the product. This rigid lock-up may not be ideal as interest rates continue to rise.

Read next: Worried about a downturn next year? Here’s how to recession-proof your portfolio

You must be logged in to post a comment.