Building passive income in Singapore is a smart way to boost financial security, supplement your salary, and plan for retirement. But many people make common mistakes that can erode returns and waste time.

In today’s climate of rising costs of living, relying solely on a salary is often not enough to meet long-term financial goals. Passive income—earnings that require little to no active work—has become an increasingly popular way to grow wealth, secure financial freedom, and prepare for retirement.

But generating passive income isn’t always straightforward. Many Singaporeans fall into traps that reduce potential returns or expose them to unnecessary risk. Avoiding these mistakes is key to building a reliable, long-term income stream.

Here are the five most common mistakes Singaporeans make when pursuing passive income, and ways you can avoid them.

Mistake 1: Chasing High Returns Without Understanding Risk

It’s easy to get tempted by investments that promise unusually high returns, from high-yield bonds and dividend stocks to peer-to-peer lending platforms. But high returns usually come with higher volatility or credit risk. Many investors overlook these factors and end up taking on far more risk than they realise, which can lead to inconsistent income or outright losses.

How to avoid it:

Focus on stable, well-researched, and diversified income sources rather than chasing the next high-yield idea. Always take time to understand what you’re investing in, whether it’s the credit rating of a bond, the track record of a company, or the underlying business model of a platform.

Passive income works best when you prioritise consistency over speculation. Portfolios that emphasise quality bonds and established dividend-paying equities can help deliver steadier income while managing downside risk.

Mistake 2: Failing to Diversify Your Income Sources

Another common mistake is concentrating all your investments into a single stock, REIT, or property.

When your income relies heavily on one asset or sector, any downturn can have an outsized impact on your returns. Lack of diversification is one of the biggest contributors to unstable passive-income results.

How to avoid it:

Build a portfolio that spreads risk across asset classes—such as bonds, equities, and different property sectors—as well as across geographies. This helps smooth out income fluctuations and reduces reliance on any single source.

Diversified REIT portfolios, broad-based equity income funds, and multi-asset income strategies are useful tools for investors who want stability without the effort of managing multiple individual positions. Remember: diversification is the cornerstone of sustainable passive income.

Mistake 3: Ignoring Fees and Hidden Costs

Many passive-income strategies appear straightforward until you account for the fees involved—maintenance costs, brokerage fees, platform charges, and more. If you ignore fees, your net income may be far lower than expected. This can quietly erode long-term returns and make an otherwise decent strategy ineffective.

How to avoid it:

Look for investment platforms and products that offer transparent fee structures. Fewer hidden costs and lower ongoing charges mean more income stays in your pocket.

Automated portfolios with periodic rebalancing can also reduce unnecessary trading (and therefore trading costs), helping keep your income strategy efficient.

Pro tip: Always assess net returns—after fees.

Mistake 4: Expecting Overnight Results

Passive income is not a shortcut to wealth. Unrealistic expectations often cause investors to abandon sound strategies too early. Some investors become impatient when returns don’t appear immediately, leading to frequent switching between investments or poorly timed decisions.

How to avoid it:

Adopt a long-term mindset. Compounding, reinvested dividends, and consistent contributions take time to build meaningful passive income.

Whether you’re using dividend-focused funds, REIT portfolios, or bond ladders, the real power comes from staying invested through market cycles. Patience and discipline are essential.

Mistake 5: Not Considering Liquidity Needs

Some passive-income strategies involve locking funds into illiquid assets such as private real estate, long-tenor bonds, or private REITs. If an emergency arises and you need cash, you may be forced to sell at an unfavourable time or at a discount.

How to avoid it:

Ensure your passive-income plan includes a mix of liquid investments. Publicly listed REITs, bond funds, and multi-asset portfolios typically offer better liquidity than private or highly niche investments.

A balanced approach helps you maintain income while still having quick access to cash when needed. Income should support your lifestyle—not restrict your flexibility.

Build Smarter Passive Income in Singapore

Passive income can be a powerful tool for Singaporeans seeking financial security, supplementary income, or retirement planning. But success depends on five key factors:

- Understanding risk

- Diversifying assets

- Controlling costs

- Staying patience

- Maintaining liquidity.

For those who want a hands-off yet effective approach, portfolios like Syfe’s Income+ and REIT+ offer easy, managed ways to generate steady passive income.

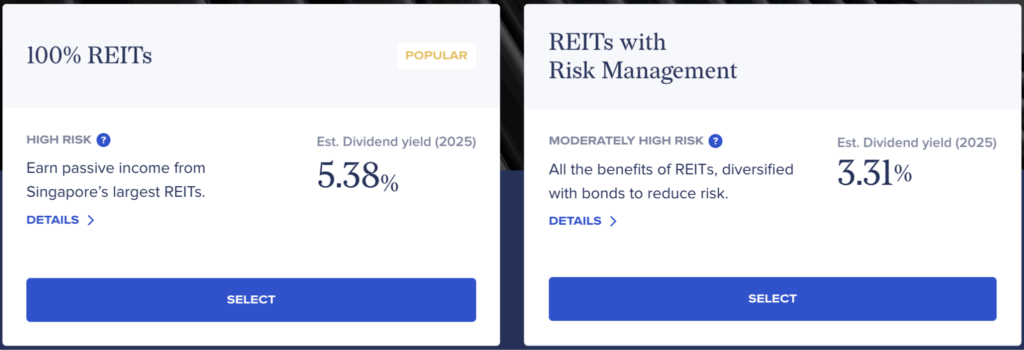

REIT+

Comprising the top 20 S-REITs (SGD-denominated) and offering broad exposure across key property sectors, the REIT+ portfolio is professionally managed and mirrors the iEdge S-REITs leader index. It is optimised based on liquidity and market cap, with automatic reinvestment of dividends.

Currently, the REIT+ (100% REITs) portfolio offers an estimated dividend yield of 5.38% p.a., well above other yield-generating instruments, such as 10-year Singapore government bonds, which has a yield of 2.01%.

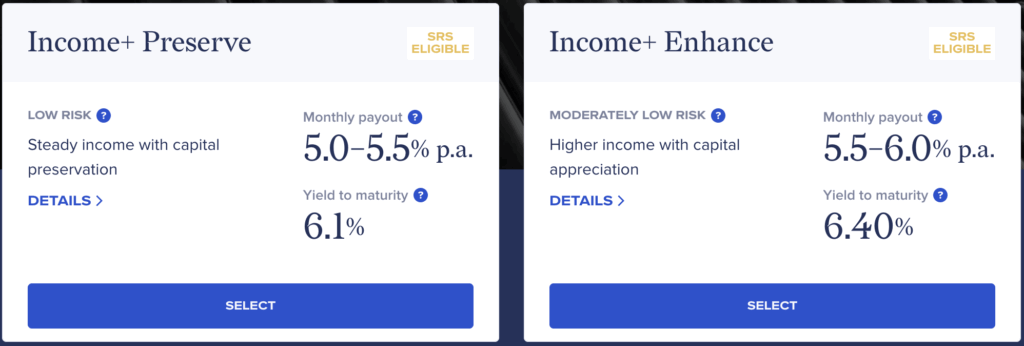

Income+

Income+ is a professionally managed, globally diversified bond portfolio designed to generate passive income. It offers two main options, Preserve and Enhance, to cater to different risk appetites, providing regular monthly payouts with no lock-in periods, minimum balance required, or withdrawal penalties.

The portfolio is powered by actively managed funds from PIMCO and comprises SGD-hedged, investment-grade funds. It provides a distribution yield (i.e. monthly payout) of 5.0%-5.5% for Preserve and 5.5%-6.0% for Enhance, and a yield-to-maturity of 6.1%-6.4%.

With these professionally managed portfolios and diversified holdings, you can focus on your life while your money works for you.

Explore Syfe Income+ and REIT+ today to build a smarter, safer passive income portfolio that grows with you.

Read More:

- Passive Income Streams That Work for Singaporeans (and How to Start Earning)

- The Best Passive Income Investments in Singapore

- How To Earn $1,000 In Passive Income Each Month: A Singaporean’s Guide

- The Great Rebound: Singapore REITs Q3 2025

- How to Pick Resilient REITs in Singapore’s Property Market Recovery

You must be logged in to post a comment.