Investing in real estate—whether flipping properties or renting them out—can be highly rewarding. However, the high upfront capital, ongoing costs, and active management often make direct property investing inaccessible for many.

For those seeking a simpler, more affordable way to invest in property, Singapore Real Estate Investment Trusts (S-REITs) offer exposure to a diversified portfolio of income-generating properties without the hassle of direct ownership.

With consistent dividend payouts and lower entry costs, S-REITs can be a valuable addition to your portfolio. This guide outlines a REIT Investing Strategy Singapore prospective investors can apply with clarity. You will learn how S-REITs work, the key metrics that help distinguish sustainable income from yield traps, the major risks to manage, and a repeatable way to build REIT exposure.

A Simpler Way to Invest in S-REITs with Syfe REIT+

If you prefer a hands-free, diversified approach, Syfe REIT+ gives you convenient exposure to Singapore’s REIT market in a single managed portfolio.

It invests in the 20 largest SGD-denominated S-REITs, selected for liquidity, market size, and backing by reputable management teams—including names like CapitaLand Integrated Commercial Trust, Mapletree Logistics Trust, and Keppel DC REIT.

You can start with no minimum amount, choose automatic dividend reinvestment (or receive quarterly payouts), and avoid per-trade brokerage fees for more cost-efficient implementation.

Table of Contents

- What Are S-REITs?

- Why Invest in REITs in Singapore?

- 10 Years of Singapore REITs Performance: Trends and Takeaways

- How S-REITs Work and Key Roles Explained

- Risks Associated with Investing in REITs

- Should You Invest in S-REITs?

- What a REIT Investing Strategy Singapore Should Achieve

- How to Buy Singapore REITs

- Quick Takeaways

- Conclusion

- Frequently Asked Questions (FAQs)

- Resources & Further Reading

What Are S-REITs?

S-REITs are investment trusts that invest in a portfolio of income generating assets such as shopping malls, offices, industrial parks, hotels, and healthcare properties.

Most of these properties are based in Singapore. S-REITs pool together money from investors to purchase these properties, which are then leased out to tenants to generate revenue (primarily rental income). Unlike directly owning a rental property, where landlords must manage tenants and maintenance, investing in S-REITs provides exposure to real estate with lower capital, less effort, and greater diversification.

Read our comparison between REITs and rental properties to see which is the better investment.

S-REIT investors, also known as unit holders, usually receive this rental income in the form of quarterly or semi-annual dividends. The average dividend yield for S-REITs is about 5% to 6%.

Apart from dividends, unit holders typically also earn returns through capital gains when the price of the REIT appreciates due to rising property values, or when they sell the REIT at a higher price than they purchased it for.

Similar to stocks, S-REITs are listed on the Singapore Exchange and you can invest in them the same way you would in a stock. But do note that S-REITs have a unique structure and regulatory framework that differentiates them from traditional listed companies.

Why Invest in REITs in Singapore?

S-REITs offer an easy and cost-effective way to invest in real estate while enjoying passive income and liquidity. With lower capital requirements, steady dividend payouts, and diversification benefits, they provide a compelling alternative to physical property investments.

Here’s why they stand out:

Lower Capital Requirements

S-REITs require minimal upfront investment, allowing investors to start with as little as 100 shares, unlike physical property, which involves high down payments and taxes.

Passive Income Through Distributions

With mandatory dividend distributions of at least 90%, S-REITs provide consistent passive income, averaging 5% to 6% dividend yields, higher than traditional savings options.

Better Liquidity for Investors

Unlike illiquid real estate, S-REITs are traded on SGX, enabling investors to buy or sell instantly without the long wait times associated with selling physical property.

Portfolio Diversification Within Real Estate

Instead of concentrating capital in a single property, S-REITs spread risk across multiple assets and sectors, including retail, industrial, and hospitality properties. Over 90% of S-REITs and property trusts hold overseas properties, reflecting the market’s international footprint.

Tax Treatment for Singapore Investors

S-REIT dividends are not taxed, whereas rental income from property is subject to income tax and property tax, making REITs a more tax-efficient investment option.

S-REITs vs. Physical Property: Are REITs a Good Investment?

For investors choosing between S-REITs and physical property, the table below highlights key differences:

| Factor | S-REITs | Physical Property |

| Capital required | Low | High – down payment, stamp duty, taxes |

| Management effort | None – managed by professionals | High – leasing, maintenance, and repairs |

| Liquidity | High – can be sold anytime on SGX | Low – property sales take months |

| Diversification | High – invests in multiple properties | Low – usually limited to one property |

| Taxation | Dividends are not taxed for individuals | Rental income is taxable, property tax applies |

A practical perspective: S-REITs can be a more flexible real-estate allocation tool, while property ownership may appeal to investors who want direct control and are comfortable with illiquidity and active management.

10 Years of Singapore REITs Performance: Trends and Takeaways

Over the past decade, S-REITs have demonstrated strong long-term investment potential, driven by stable dividend yields and capital appreciation. As the largest REIT market in Asia (ex-Japan), Singapore’s REIT sector has grown at a compound annual growth rate (CAGR) of 6%, reinforcing its importance in the region.

Overall Trends and Key Performance Metrics

- Market breadth and size: The S-REIT sector now comprises 38 listed REITs and property trusts with a total market capitalisation of S$100 billion (as of late 2025).

- Dividend yields: S-REITs continue to offer attractive dividend yields, averaging 5.59% (as of 22 October 2025), well above the 2.30% yield of Singapore’s 10-year government bonds.

- Global expansion: Over 90% of S-REITs own overseas properties, highlighting their role in global real estate investment.

- Resilience and recovery: Despite periods of market downturn, the sector has remained a strong performer for long-term investors, with many REITs delivering impressive total returns.

Long-term outcomes are driven less by “the highest yield today” and more by whether distributions are supported by durable property cashflows and a resilient financing profile across market cycles.

How S-REITs Work and Key Roles Explained

How S-REITs Work

S-REITs are structured to pool funds from investors to acquire and manage income-generating real estate properties. These properties are then leased to tenants, and the rental income is distributed to investors as dividends.

Here’s a step-by-step breakdown of how the structure works:

- Capital raising: An S-REIT raises capital from investors through an IPO on the Singapore Exchange (SGX). Investors become unit holders by purchasing REIT shares.

- Property acquisition: The funds collected are used to purchase commercial, industrial, retail, or hospitality properties. These properties form the core assets of the REIT.

- Leasing and operations: The acquired properties are leased to tenants, such as businesses, retailers, and corporations. The rental income generated serves as the main revenue source for the REIT.

- Distribution: After deducting management fees, operational costs, and interest expenses, the remaining rental income is distributed to investors as income distributions (dividends). By regulation, S-REITs must distribute at least 90% of their taxable income to qualify for tax transparency benefits.

Important nuance: “90% distribution” is best understood as an incentive-based feature tied to tax transparency, not a guarantee of stable payouts. Distributions can still fall if occupancy weakens, rents decline, or interest expense rises.

Key Roles in an S-REIT

S-REITs involve multiple entities that work together to ensure smooth management, income generation, and regulatory compliance.

Property Manager

The property manager is responsible for the day-to-day management of the REIT’s properties. This includes:

- Collecting rent from tenants

- Marketing and leasing vacant units

- Implementing asset enhancement initiatives to improve property value and occupancy rates

REIT Manager (Trust/Asset Manager)

The REIT manager, also known as the trust or asset manager, sets the strategic direction of the REIT. Key responsibilities include:

- Identifying new properties for acquisition

- Deciding when to divest underperforming assets

- Optimising portfolio performance to maximise returns for unit holders

Sponsor

The sponsor is typically a property developer or investment firm that provides the initial assets and backing for the REIT. The sponsor often:

- Owns a significant stake in the REIT

- Controls both the property manager and REIT manager

- Provides a pipeline of future assets for acquisition

For example, CapitaLand Investment Limited sponsors CapitaLand Ascendas REIT (CLAR, SGX:A17U), Singapore’s largest industrial REIT.

Trustee

The trustee holds the REIT’s assets on behalf of unit holders and ensures the REIT is managed in accordance with the trust deed and regulatory requirements. The trustee’s primary duties include:

- Safeguarding investors’ interests

- Overseeing compliance with REIT regulations

- Ensuring fair and transparent asset management

Why These Roles Matter to Investors

Understanding these roles helps investors assess:

- Management quality — A well-managed REIT with strong sponsors and experienced managers is more likely to deliver consistent returns.

- Risk factors – High levels of sponsor ownership may indicate strong backing, but also pose potential conflicts of interest.

- Long-term stability — A strong trustee and governance structure ensures that the REIT operates in compliance with investor protections.

By evaluating the property portfolio, management expertise, and financial health, investors can make better-informed decisions when investing in Singapore REITs.

Risks Associated with Investing in REITs

While REITs, especially the ones in Singapore offer attractive dividends and capital appreciation, they also come with inherent risks. Understanding these risks can help investors make informed decisions and avoid potential pitfalls.

Market Risk

REITs are publicly traded, meaning their prices fluctuate based on broader economic conditions, interest rate changes, and investor sentiment. For example, Manulife US REIT struggled as declining office demand in the US affected occupancy rates and rental income. Investors should monitor sector trends and macroeconomic factors before investing.

Income Risk (Occupancy and Rental Pressure)

REITs rely on rental income from tenants. If occupancy rates decline due to economic downturns or shifting market trends, distributions to investors may be affected. The hospitality and retail sectors tend to be more volatile, as they are highly dependent on consumer spending and foot traffic. REITs with weak tenant demand or high vacancy rates may experience lower rental income and reduced dividends.

Liquidity Risk (For Smaller Counters)

While REITs are more liquid than physical property, some thinly traded REITs can experience low trading volume, making it harder to exit positions at a favourable price. Investors should check average daily trading volume before investing in smaller REITs.

Leverage and Refinancing Risk

Many REITs use debt to finance property acquisitions, which can amplify returns but also increase financial strain if interest rates rise. For instance, Lippo Malls Trust faced refinancing issues due to its high debt burden, contributing to its sharp decline in value. Investors should assess a REIT’s gearing ratio (debt-to-assets) to ensure it remains at a sustainable level.

Real-world examples (why this matters):

- Manulife US REIT has disclosed periods where distributions were halted amid recapitalisation and restructuring considerations, illustrating how financing constraints can flow through to payouts.

- Lippo Malls Indonesia Retail Trust (LMIRT) has faced heightened refinancing risk highlighted by rating agency actions, showing how maturity walls and funding conditions can materially impact REIT stability.

A practical risk-management insight (often overlooked): sector diversification alone is not enough. Investors should also diversify by debt maturity timeline, so multiple holdings are not forced to refinance heavily in the same year.

Should You Invest in S-REITs?

SS-REITs may be a good fit if you:

- Want steady passive income through dividend distributions.

- Are looking for a lower-cost way to invest in real estate without owning physical property.

- Prefer liquid investments that can be traded easily on the stock market.

- Seek diversification beyond traditional stocks and bonds.

While S-REITs are a good investment for many, they still come with risks, such as market fluctuations, leverage exposure, and sector-specific challenges. Before investing, ensure that S-REITs align with your financial goals and risk tolerance.

What a REIT Investing Strategy Should Achieve

A robust REIT Investing Strategy Singapore investors can rely on should go beyond selecting a few high-yield tickers. It should provide a repeatable framework for decision-making and align REIT exposure with your broader financial plan.

Clarify the Role of REITs in Your Portfolio

Most investors approach REITs for income, but REITs are also real-asset securities. Returns reflect a combination of:

- cashflow stability (occupancy and rents)

- financing structure (leverage and interest costs)

- market valuation (yield expectations and risk appetite)

Start by choosing the objective that matters most:

- Income objective: prioritise resilient distributions

- Diversification objective: add property-linked cashflows alongside other assets

- Total return objective: combine distributions with long-term value growth

Avoid “Yield-First” Decision-Making

A high yield can be a value—or a warning. Sustainable income is supported by:

- stable occupancy and defensible rents

- manageable leverage and refinancing timelines

- disciplined capital allocation that protects DPU (distribution per unit) over time

In other words, yield is an output, not a foundation.

Keep the Strategy Executable

A practical REIT Investing Strategy Singapore approach should include:

- a defined allocation range

- a diversification rule (sector and refinancing timeline)

- a contribution schedule (often DCA-based)

- a review checklist based on metrics, not market noise

Tip: Treat REIT investing as “owning cashflow structures” rather than “chasing yields”. The cashflow structure that survives rate cycles is the one that compounds.

How to Buy Singapore REITs

Investors can buy S-REITs through brokerage platforms like Syfe’s Brokerage, ETFs, or managed portfolios such as Syfe REIT+.

Buying Individual REITs or REIT ETFs

If you prefer a hands-on approach, this route gives you market-listed REIT exposure, with two implementation paths.

Path 1: Individual S-REITs

Best suited for: investors who are comfortable analysing fundamentals and reviewing REIT-specific risks.

Advantages

- Control over portfolio construction: You decide exactly which REITs you own, how much to allocate to each, and how you diversify by sector, geography, and tenant profile.

- Ability to target specific quality factors: You can prioritise stronger balance sheets, better refinancing ladders, or more defensive cashflows rather than following an index.

- Potential valuation selectivity: You can avoid REITs you view as expensive or structurally weaker, and add exposure when valuations are more attractive.

Trade-offs

- Higher single-name risk: A tenant issue, acquisition misstep, rights issue, or refinancing pressure can materially impact one REIT—and therefore your portfolio if position sizes are meaningful.

- Higher monitoring burden: You need to track fundamentals (occupancy, rental reversions, WALE), financing profile (maturities, hedging), and corporate actions (placements/rights issues).

- Diversification depends on you: If you do not construct the basket thoughtfully, you may end up over-concentrated (i.e., different tickers but same sector/risk drivers).

Path 2: REIT ETFs

Best suited for: investors who want broader REIT exposure with reduced single-name monitoring.

Advantages

- Built-in diversification: Exposure is spread across a basket of REITs, reducing the impact of any single REIT-specific shock.

- Lower maintenance: The ETF’s index methodology and rebalancing process reduces the need for ongoing single-name monitoring.

- Consistency and simplicity: Easier to implement systematic investing (e.g., regular contributions) without repeatedly selecting and sizing individual names.

Trade-offs

- Less control over holdings: You own what the index includes, even if some constituents have weaker balance sheets, sector exposure you dislike, or frequent dilution risk.

- Index concentration can still exist: Some REIT indices can be skewed toward larger constituents or particular segments, which may create unintended concentration.

- Valuation selectivity is limited: You cannot easily avoid expensive constituents or overweight your highest-conviction names without adding additional positions outside the ETF.

Steps to Buying Individual REITs or REIT ETFs in Singapore

Step 1: Open a brokerage account with an SGX-approved platform (e.g., Syfe).

Step 2: Research S-REITs or REIT ETFs based on dividend yield, property sector, and financial stability.

Step 3: Place an order via your brokerage account (minimum investment is typically 100 shares per REIT).

Step 4: Monitor your investments and reinvest dividends for long-term growth.

Tip: REIT ETFs provide instant diversification, making them ideal for investors who want exposure to multiple REITs without selecting individual ones.

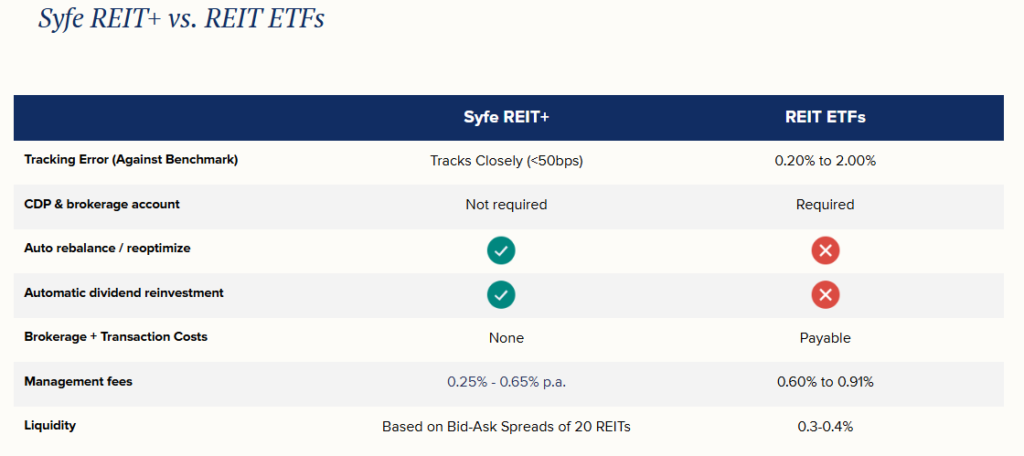

Investing Through Syfe REIT+ Portfolio

For investors who prefer a hands-free, diversified, and cost-efficient approach, Syfe REIT+ is a managed portfolio designed for easy access to Singapore’s top-performing REITs.

Why Choose Syfe REIT+?

- Diversification – Invest in the 20 largest SGD-denominated Singapore REITs, including CapitaLand Integrated Commercial Trust, and Mapletree Logistics Trust and Keppel DC REITs. These REITs are selected for their SGD denomination, liquidity, large market capitalisations, and strong backing by reputable management teams.

- No minimum investment amount – Start investing with any amount at any time.

- Automated reinvestment – Dividends are automatically reinvested to enhance long-term returns. Quarterly dividend payouts are also available.

- Lower fees – No brokerage fees per transaction, making it more cost-effective.

Start investing in S-REITs effortlessly with Syfe REIT+ today!

Quick Takeaways

- Singapore’s REIT market is one of Asia’s deepest, with around S$100 billion in market capitalisation (counts vary over time).

- S-REIT yields vary by cycle; historical averages have often been 5%–6%, with periods where sector yields have moved higher.

- A durable REIT investing strategy approach focuses on sustainable income, not just the highest headline yield.

- REIT distributions are supported by property fundamentals and can fall when tenant demand weakens.

- Choose an implementation method you can maintain: individual REITs (more control, more monitoring) or REIT ETFs (more diversified, lower maintenance).

A practical edge comes from reducing hidden concentration—especially refinancing concentration risk—not from perfect market timing.

Conclusion

S-REITs can be a practical way to gain real estate exposure with liquidity and income potential, without the capital intensity and operational burden of owning physical property. However, long-term outcomes depend less on choosing the highest yield and more on applying a disciplined investing strategy framework that prioritises cashflow durability and financing resilience.

A sound strategy begins with clarity: define whether REITs are meant to support income, diversification, or total return. From there, choose an approach you can realistically maintain. Investing in individual S-REITs offers control and the ability to target quality, but requires ongoing monitoring of occupancy, rental reversion, leverage, and refinancing timelines. A REIT ETF approach offers built-in diversification and lower maintenance, but reduces your control over holdings and valuation exposure.Most importantly, treat REIT investing as a process. Invest systematically where appropriate, and review quarterly based on fundamentals. This is how a REIT investing strategy stays consistent through rate cycles, without being driven by short-term headlines.

Frequently Asked Questions (FAQs)

1) What is a sensible REIT Investing Strategy beginners can start with?

A sensible starting point is to prioritise diversification and simplicity: begin with a REIT ETF or a diversified basket, invest in a measured allocation, and track a short checklist (DPU trend, gearing ratio, ICR, and refinancing timeline).

2) Is dividend yield enough to choose the best Singapore REITs?

No. Yield should be evaluated alongside sustainability. Review occupancy trends, rental reversion, WALE, debt maturity profile, hedging, and whether distributions are supported by resilient cashflows rather than short-term boosts.

3) Are S-REIT distributions taxable for Singapore individuals?

Many individual investors receive tax-exempt REIT distributions, subject to conditions and depending on the distribution’s nature. For accuracy, refer to official guidance and the REIT’s distribution breakdown.

4) Should I buy individual REITs or a Singapore REIT ETF?

Individual REITs offer more control and valuation selectivity but require more monitoring and carry higher single-name risk. A Singapore REIT ETF offers diversification and lower maintenance but gives you less control over holdings and index concentration.

5) What is the biggest risk investors underestimate in a REIT portfolio Singapore investors build for income?

Many underestimate refinancing concentration risk—i.e. owning multiple REITs that refinance heavily in the same period. A simple maturity-ladder review can meaningfully reduce this hidden risk.

Resources & Further Reading

- Syfe REIT+ vs REIT ETFs: What’s The Difference?

- The Definitive Guide to Investing In REITs

- The Great Rebound: Singapore REITs Q3 2025 (Outlook)

- Singapore Industrial REITs Outlook 2025: Market Trends, Performance, and What Investors Should Know

- Why Healthcare S-REITs Are a Hidden Gem for Defensive Investors

- Singapore Office REITs: Why Prime Office Assets Remain a Compelling Investment in 2025

You must be logged in to post a comment.