Over the past weeks, there has been a lot of talk about the rotation from growth stocks – companies expected to grow sales and earnings at a faster rate than the market average – into value stocks.

On the surface, that appears to be the case. In November, value stocks – shares that trade at a lower price relative to a company’s fundamentals – enjoyed a resurgence after news of a potential vaccine breakthrough was announced.

Investors sold some of the biggest growth names in the market from Amazon to Microsoft, and pivoted to value stocks in the financial, industrial and energy sectors. In a client note published mid November, investment bank Goldman Sachs noted that a “powerful tactical rotation” into value stocks was underway.

There’s more to it than meets the eye

Dig a little deeper however, and a different perspective emerges. The move to value has also been accompanied by a marked rotation towards small-cap stocks. In fact, it is the small-cap factor, not the value factor, that has been the major driving force behind the strong performance of the Invesco S&P 500 Equal Weight ETF (RSP) the past months.

RSP is an equal weighted ETF that invests in all S&P 500 component stocks equally. As such, it offers greater exposure to value and small-cap stocks. In comparison, a traditional market capitalization weighted ETF like the SPDR S&P 500 ETF (SPY) will allocate larger percentages of the index to larger companies. For this reason, SPY tends to give a large-cap tilt.

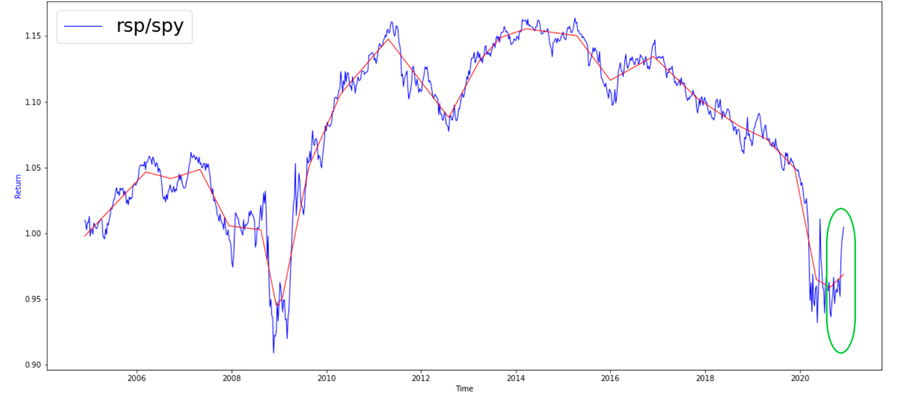

Based on Syfe’s analysis, we can see that the RSP has outperformed the SPY in recent months. The chart RSP/SPY shows the relative performance of both funds. An uptrend indicates that RSP is performing better than SPY and vice versa.

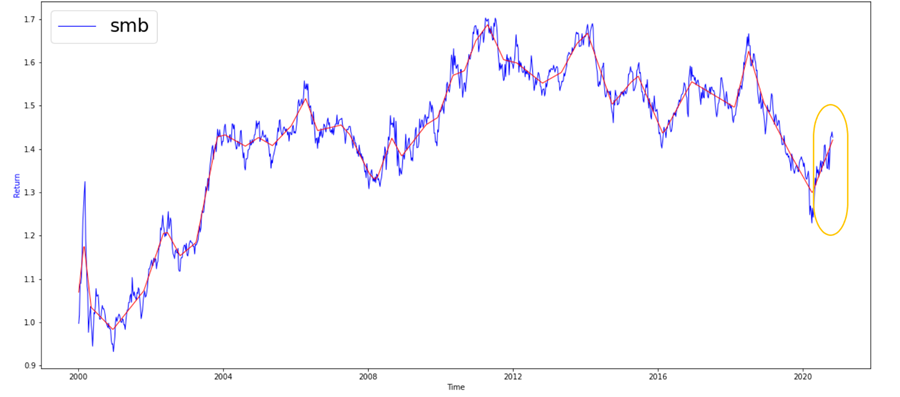

As circled in green, RSP has delivered strong gains over the past months. This has coincided with the uptrend in the small-cap factor, as represented by the yellow circle on the SMB chart below.

Put simply, SMB stands for small minus big (SMB), one of the three factors used in the Fama-French three-factor model. SMB is known as the “small firm effect” and argues that smaller companies outperform larger ones over the long-term.

However, the outperformance of RSP does not seem to be explained by the value factor, or high minus low (HML). HML is another factor in the Fama-French model. It accounts for the spread in returns between value stocks and growth stocks and posits that value stocks outperform their growth counterparts.

We can see that value stocks (represented by HML) have been on a downward trend since 2007. Throughout 2020, value experienced brief moments of strong performance before receding again. Such moments notwithstanding, the overall trend for value is still down in 2020 as circled below.

Looking across the three charts, it is clear that the uptrend for both the small-cap factor and the outperformance of RSP over SPY are aligned. On the other hand, the surge in RSP has coincided with a dip in the value factor.

The takeaway is that we are seeing the beginning of a rotation from large-cap stocks to small-cap stocks, and not so much a growth to value rotation.

Why small-cap stocks are surging

History suggests that small-cap stocks tend to benefit coming out of recessions. A global recovery in 2021 looks increasingly likely, supported by mass vaccine roll-out plans. Small-cap stocks are also largely concentrated in cyclical sectors such as financials, materials, and energy. These sectors tend to do well as the economy reopens.

In the US, a worsening COVID-19 situation and slowing job growth could signal that more economic stimulus will be in the making once president-elect Joe Biden takes office next January. Stimulus is viewed as a boon for small-cap stocks which tend to be tied closely to the US economy, as compared to large-cap stocks which have more international presence.

Can this rotation last?

The question now is whether this rotation can be sustained.

JPMorgan analyst Michael Feroli recently forecast an economic contraction of a 1% annualized rate in the first quarter of 2021, down from the previous forecast of a 1.5% increase. The economic outlook for the next few months could be uneven, suggesting some volatility ahead for small-cap stocks.

While a longer-lasting rotation is certainly a possibility, we continue to caution investors from making sudden and significant changes to their asset allocations. The market right now is catalyst driven; any rotation could fizzle out or gain momentum depending on news headlines.

What does this mean for Core Equity100?

Syfe’s Core Equity100 portfolio is built on three factor tilts: growth, large-cap, and low-volatility. From our analysis, we see that growth is still dominating value. The top growth stocks today all have relatively healthy balance sheets, positive cash flow, and resilient profits. Growth stocks are still well-positioned for the economic recovery in 2021.

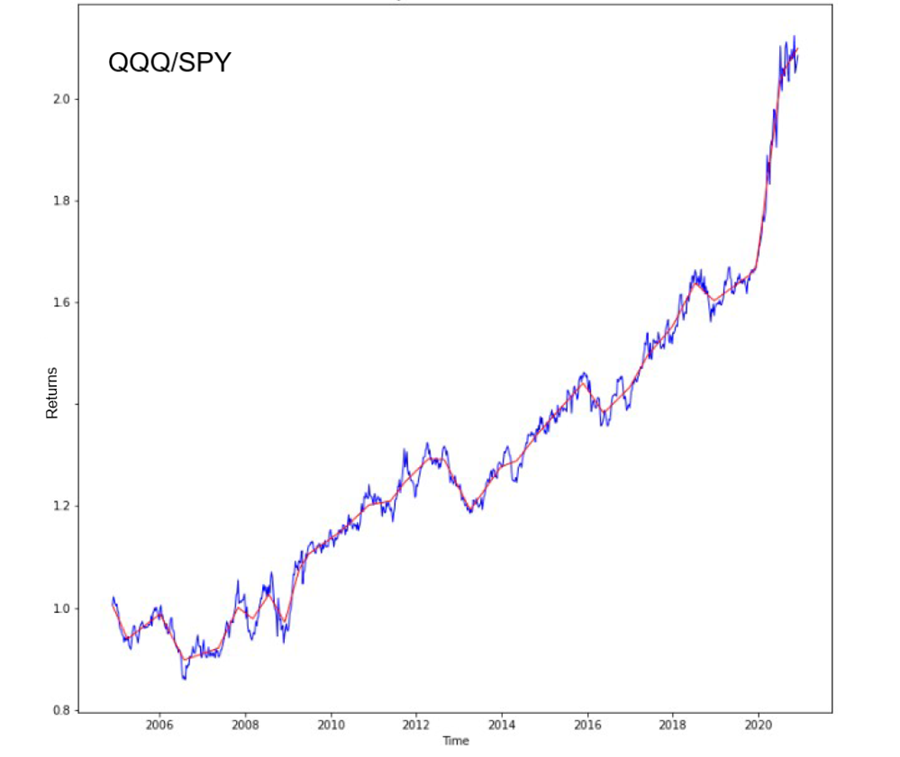

Our research also shows that the impact of the small-cap factor has been dwarfed by growth’s relative outperformance against value. This is evident in the performance of the Invesco QQQ ETF so far.

QQQ gives the Core Equity100 portfolio both growth and large-cap factor tilts. It holds 100 of the largest international and domestic companies listed on the Nasdaq stock exchange, making it simple for investors to invest in global stocks from Singapore. Our analysis indicates that the large-cap factor has not significantly impacted QQQ’s relative performance vis-a-vis the broader market to date. In other words, growth is still dominating value more than small-cap over large-cap.

That said, one unique feature of Core Equity100 is our dynamic factor strategy, which you can read more about here. We will be monitoring how the small-cap factor performs going forward, and may look to increase our exposure to this factor during our next rebalancing cycle in April 2021.

By Richard Yeh, Head of Portfolio Construction and Risk Management, Syfe

You must be logged in to post a comment.