Factor investing – or smart beta – is on the rise. And with good reason. Factors are long-term drivers of investment returns. This means that investors can potentially enhance returns or reduce risk by exposing their portfolios to meaningful factors.

Last week, we hosted a webinar with Alvin Chow, CEO of Dr Wealth, to get his take on factor investing. Alvin is a firm believer in factor investing and has been using this strategy in his portfolio for the past seven years. Here are the highlights of our conversation.

What are factors?

Very simply, factors are drivers of investment returns – they provide investors with a higher probability of returns. Factors are grounded in decades of academic research. In fact, factors are becoming so numerous that some have referred to the universe as a factor zoo.

Alvin noted that although there are thousands of factors, not all factors are significant. Only a few key factors such as value, size, momentum and volatility have a meaningful impact on portfolios.

“Factors can help you lower your risk and improve your returns,” he explained. “Instead of just diversifying by asset classes, you can use factors to improve your diversification. Within stocks, you can diversify not just by countries and sectors, but also factors,” he added.

The importance of factor diversification

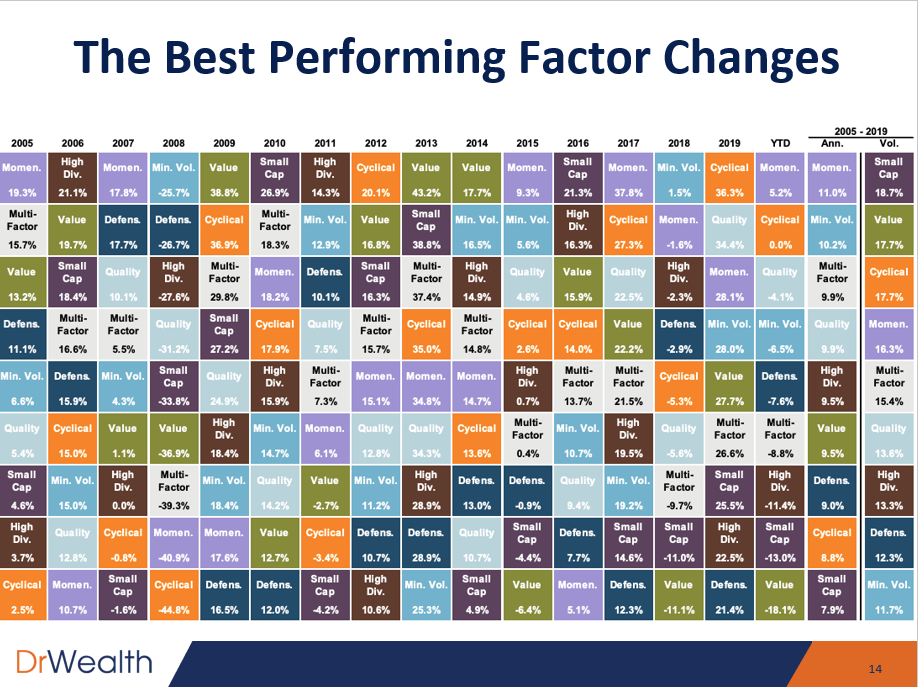

This is largely because individual factor performance can be very cyclical. During the webinar, Alvin pointed out that the best performing factor frequently changes year to year. In 2017, the top performer was the momentum factor. Minimum volatility topped in 2018. In 2019, it was cyclical’s turn. Year to date, the best performing factor currently is once again momentum.

“If you stick to just one factor, you will never be able to outperform all the time. By diversifying across a couple of factors, you can catch winning factors in any given year,” Alvin shared.

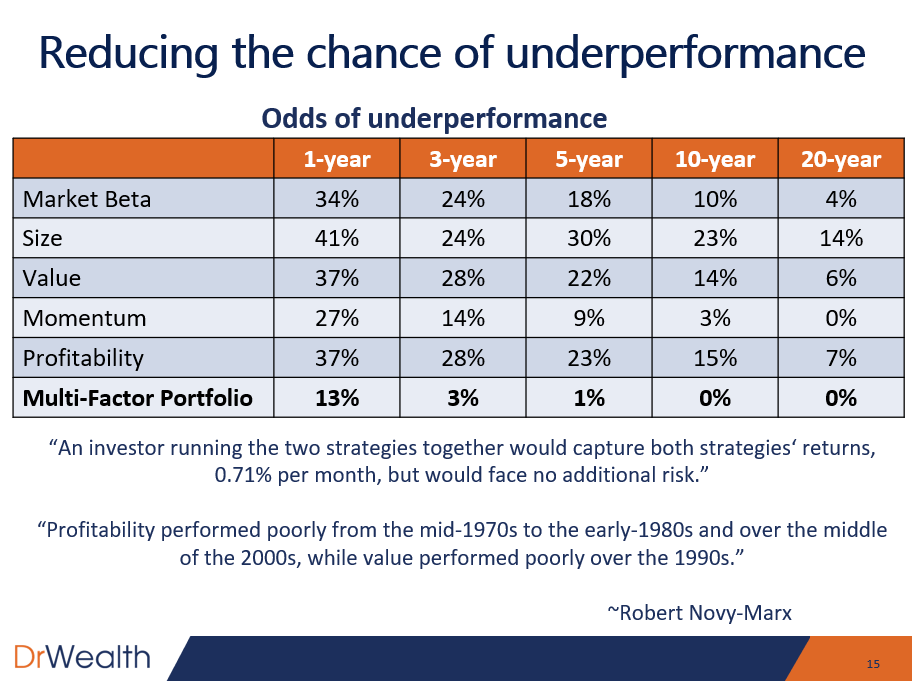

Moreover, a single-factor strategy can increase your odds of underperformance. In their book Your Complete Guide To Factor-based Investing, Larry Swedroe and Andrew Berkin found that a combination of factors performed better than a single factor alone.

For instance, an investor who is only exposed to the value factor has a 37% chance of underperforming the index in a given year. With a multi-factor portfolio however, the chance of underperformance is reduced by 3 times to just 13%. And over a period of more than five years, the odds of underperformance becomes almost insignificant.

In a nutshell, because single factors like value or momentum do not always work well all the time, it pays to diversify your factor exposure and adopt a multi-factor strategy.

How can investors implement factors in their portfolios?

Alvin recommends three ways for an investor to get factor exposure. The easiest – and probably most affordable – way is through a robo-advisor like Syfe. Syfe’s Core Equity100 portfolio provides automatic exposure to three factors: growth, large-cap, and low volatility (more on that below).

There is no need to analyse factors or decide which factor to tilt towards. If you don’t have the time or interest in studying factors, Core Equity100 is an easy, fuss-free option. Moreover, Core Equity100 comes with absolutely no brokerage fees and no investment minimums.

For investors who prefer a little more control, they can choose to invest in factor ETFs. For example, if you believe in the momentum factor, you can choose a momentum factor ETF that tracks the performance of an index measuring the performance of stocks that exhibit relatively higher momentum characteristics.

DIY may not be for everyone

It is also possible to create your own multi-factor portfolio via a DIY approach. However, this requires a lot of time and effort. To be successful, you will need to know how to rebalance, pick the right factors, and choose the best stocks for each factor. If you are an investor already busy juggling work and family commitments, you may find that the time required for DIY factor investing may be more enjoyably spent elsewhere.

Alvin also noted that some investors use factors as a preliminary stock screener, followed by more vigorous analysis of which stocks to buy. This could work well for investors who are truly passionate about the stock market. Such an approach typically means that the investor will not diversify too much and instead concentrate on a few key ideas. But this is not suitable for everyone. “You will take on more risk and you must know what you are doing. Otherwise, the consequences of picking a wrong stock in a concentrated portfolio can be disastrous,” Alvin warned.

If factors are cyclical, how can we get the right exposure?

Individual factors perform differently at different stages of the economic cycle. This is quite evident when you look at the value factor. Value investing has a long historical record of strong performance dating back decades. But in recent years, value investing has underperformed relative to growth investing.

This is a reason why the Core Equity100 portfolio is tilted towards the growth factor. Much of growth investing’s outperformance has been driven by technology stocks the likes of Facebook, Amazon, Apple, Netflix and Alphabet (FAANG).

Given the current market cycle, Syfe does not expect the growth, large-cap and low-volatility factors to underperform in the near future. Over the longer term however, we recognize that a factor that may be compelling now may be less so in another market cycle.

Dynamic factor selection

To address this limitation, Syfe has implemented a dynamic factor selection and weighting methodology for the Core Equity100 portfolio. For example, if value investing makes a comeback in the future, we might reduce the exposure to the growth factor and overweight the value factor to generate higher risk-adjusted returns.

In other words, Syfe manages the rotation of factor exposures towards the top-performing ones for you, based on broader cyclical trends and changing market conditions. To be sure, this does not mean that Syfe will be rushing in and out of factors. Rather, it means that there is no need to worry about missing out on strategic factor exposures. The Core Equity100 portfolio is optimised to tilt towards factors that drive outperformance in whatever market cycle we are in.

For investors looking for a systematic investing strategy, factor investing fits the bill. Ready to get started? Use the promo code “DRWEALTH” and receive up to $100 bonus when you invest.

You must be logged in to post a comment.