If you want to buy a house in five years’ time, how much should you start investing now? While a forecast that says you can hit that goal by investing just $100 each month sounds fantastic, chances are it won’t be of much use to you given the unrealistic underlying assumptions.

At Syfe, we believe in making our forecasts as useful and reliable as possible. This means keeping our portfolio projections realistic so that you get a clearer picture of what to expect and know how best to plan your finances accordingly.

How we forecast your expected returns

After creating your portfolio, you’ll realise that we show you three possible return forecasts: “conservative”, “most likely”, and “optimistic”. These forecasts show how much your portfolio value can potentially grow in a range of market scenarios.

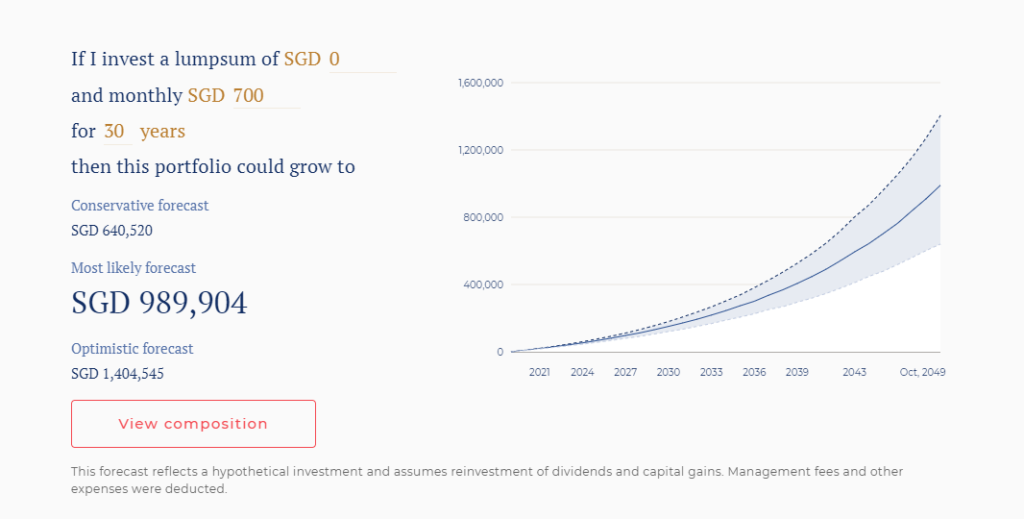

For example, here’s a projection for a hypothetical 35-year-old who wants to start investing $700 per month for his planned retirement in 30 years. He has selected a portfolio with a downside risk category of 17%.

Figure 1: Portfolio Projection for a 17% Downside Risk Portfolio

The shaded area shows the possible amounts he could have in 90% of our forecasted scenarios (more on that below). The blue solid line represents our most likely forecast – our estimate of how much money he could expect to have on average at the end of the investment period. The top dark blue dotted line and bottom light blue dotted line represent our optimistic and conservative forecasts respectively; these respective forecasts show the extreme 5% of our market scenarios.

Our “most likely” forecast is what you can realistically expect to get. This matters because when you are planning your life – budgeting for a house, starting a family, or saving for retirement – you want to be able to rely on projections you can trust.

What goes into our forecast

But how do we estimate the expected returns we use in our forecast? The approach we use is based on the Black-Litterman model for asset allocation developed in 1990 by Fischer Black and Robert Litterman at Goldman Sachs.

Simply put, we generate our forward-looking returns estimates based on the market’s views on expected returns. The Black-Litterman model looks at how all investors around the world behave to construct a global asset allocation model that reflects where investors are investing their money at any given time. In other words, the Black-Litterman model factors in the investor’s views on the expected returns of different asset classes, and how confident they are of such views to derive a market-implied return forecast.

Our forecast takes into account expected returns as derived through the Black-Litterman model and risk estimates as measured by the estimated volatility of our portfolio assets and the latest portfolio weights at each downside risk category.

10,000+ simulations

To be sure, no one can predict what will happen in the markets tomorrow. As such, we use a powerful tool known as the Monte Carlo simulation to predict thousands of possible future market scenarios and calculate the probability of each one happening.

Unlike other Monte Carlo techniques where the scenarios are generated on an ad hoc basis, we use an advanced form of non-parametric Monte Carlo simulation known as Filtered Historical Simulation (FHS). FHS is a systematic scenario generating technique that builds a probability distribution of possible values that asset prices could take in the days ahead.

To arrive at the forecast shown in Figure 1 above, we will simulate more than 10,000 different market scenarios over a 30-year investing horizon. We stress-test our hypothetical investor’s selected 17% Downside Risk Portfolio in these conditions to project the expected portfolio performance over a broad range of potential market outcomes.

A robust forecast

In short, we don’t believe in showing higher portfolio projections that may look good on paper but ultimately won’t serve its purpose in helping you plan for your future. Our “most likely” forecasts are built to be as realistic as possible so that they can reliably guide you towards achieving your financial goals.

You must be logged in to post a comment.