Growing up, the first bit of financial advice our parents gave us was probably to save money – and as much of it as possible for a rainy day. As grown-ups, we go to work, try to climb the corporate ladder and each month, continue to set aside a percentage of our salary in a savings account. This all sounds great until you realise that while you’ve been hard at work, the money in your bank account has been collecting digital dust and losing value.

Sure, you can try to save even more to make up, but why not make your money work harder?

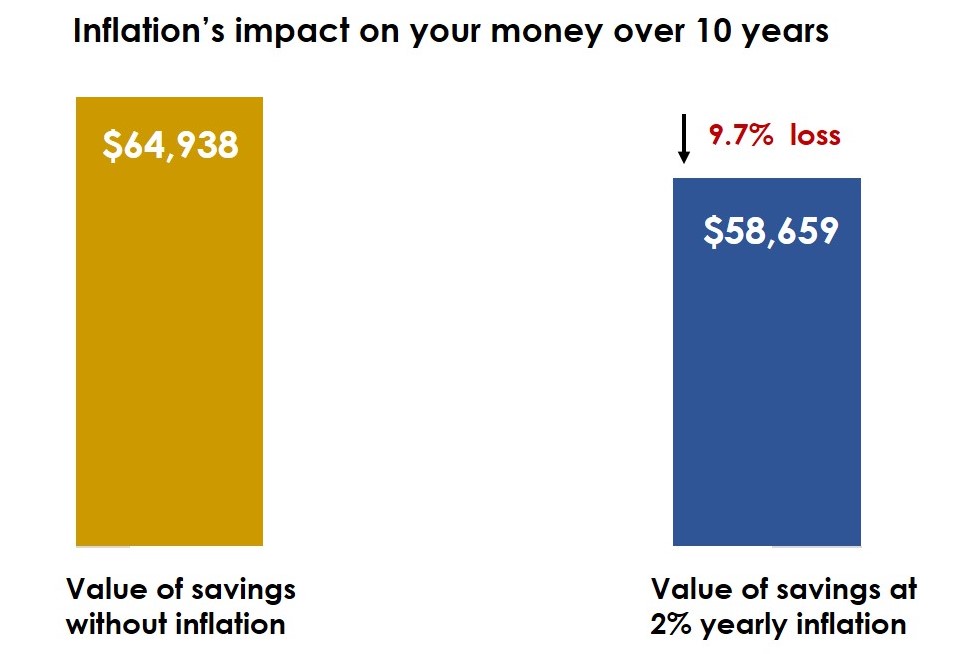

Your savings vs inflation

Many of the popular savings accounts in Singapore offer interest rates that range from around 1% to 2% per annum, depending on whether you meet certain criteria such as salary credits and / or credit card spend. A realistic interest rate to expect could be what the DBS Multiplier Account offers: an interest rate of 1.55% per annum if you make $2,600 worth of transactions (salary credit of $2,000 and credit card spend of $600 for instance).

While better than the 0.05% a basic savings account offers, the interest offered by these high-interest rate savings accounts is hardly enough to hedge against inflation over the long term.

Consider this: If you deposit $500 every month to a savings account that offers 1.55% per annum, in 10 years, you’d have saved up $64,938. At the current rate of 2% yearly inflation in Singapore however, the real value of your savings drops to only $58,659. In other words, your money lost 9.7% of its value in just 10 years.

If these rates remain unchanged, the value of your savings will continue to be eroded by inflation over the next decades. That means if retiring comfortably at 65 is one of your life goals, your savings alone may not be enough to get you there. To grow your wealth and achieve your goals, you need to invest.

What to do with your cash

If you’re ready to put your money to work, here’s how you can start.

First, determine how much of your savings you would want to set aside as emergency cash reserves and how much of the surplus would be available for investing over a longer duration. A good rule of thumb is to put away about 3 to 6 months’ worth of living expenses for an emergency fund. To grow your money, your surplus savings should then be invested instead of being left in your savings account.

Second, let time be your friend when it comes to investing. Investing early gives compound interest more time to work its magic. The sooner you start investing, the more time your money has to grow.

Finally, understand your risk appetite. All investments contain an element of risk – the heart of successful investing lies in knowing and managing these risks. If you tend to be more risk-averse for instance, consider investing in the Singapore Savings Bond. Guaranteed by the Singapore government, the bonds are virtually risk-free. If you’re more comfortable with risk, investing in equities may be a good option since they tend to offer higher returns over the long term.

Consider A Risk-based Investment Strategy

While no one can predict the financial markets, we can tip the balance in your favour through a holistic approach to managing risk. Syfe’s risk-based investment strategy can help you earn the returns to achieve your financial aspirations and grow your wealth. Not investing your money is a missed opportunity. You can start small but start soon – small amounts if invested add up to large sums over a long term.

To help you feel more confident in your investment decisions, take Syfe’s custom-built risk questionnaire to receive a portfolio recommendation tailored to your risk appetite and investment needs. New clients can receive up to $100 bonus when they open their account.

You must be logged in to post a comment.