Oil-driven inflation has sent bond yields to multi-decade highs. For long-term investors, however, the turbulence could present an opportune moment to lock in extra income and capture the next phase of growth.

What Happened

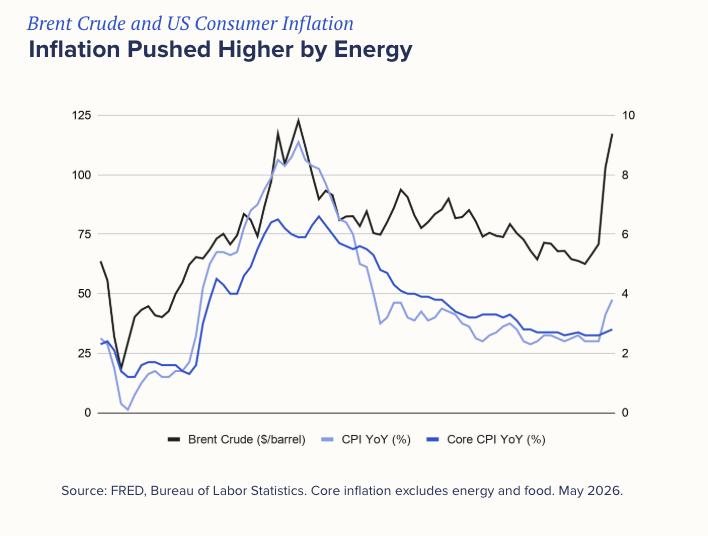

The inflation threat is back. Consumers around the world are starting to feel the effects of months of disruption in the Strait of Hormuz — the chokepoint for roughly 20% of global oil and gas supply – as the Iran War drags on. April US headline CPI came in at 3.8% year-on-year, the highest since May 2023.

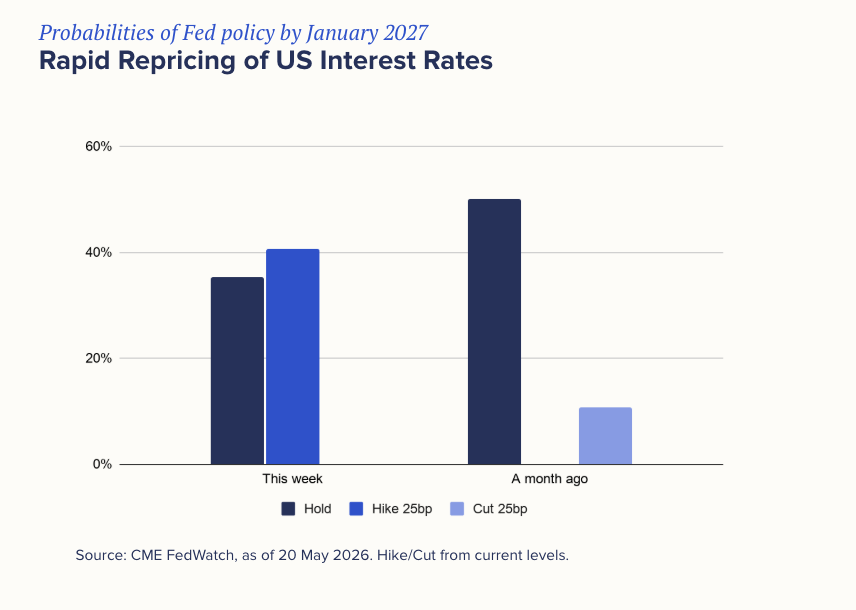

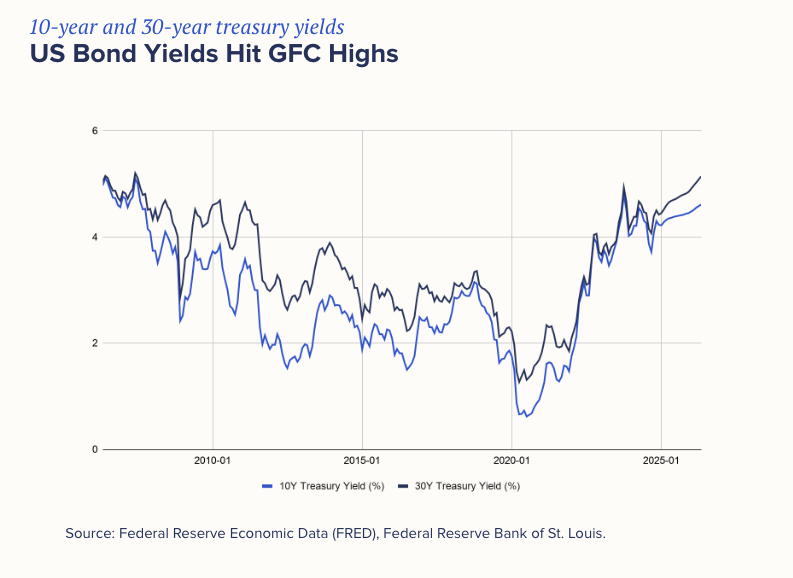

The impact on financial markets is most notable in interest rates. Markets have aggressively repriced their expectations of US interest rates – from betting on two cuts in 2026 at the start of the year, to coming close now to pricing in one hike by January 2027. This week, the correction pushed US 10-year Treasury yields to 4.6% and 30-year yields above 5%, to levels not seen since the Global Financial Crisis.

At the same time, the stock market is looking past these risks to notch record highs. Earnings have been exceptional. Nvidia just delivered another blockbuster quarter. Bond and equity markets are sending mixed messages. Both extremes can’t hold. Something has to give.

Why It Matters

Near-term, we expect more volatility. Historically, bond investors tend to be optimistic before 10-year yields cross 4.5%, which provides a comfortable income cushion above the average level of yields since 1990. Once that barrier is crossed, however, investors start to wonder if the risk is worth it.

A rapid run-up in interest rates is also bad for equities and the economy. When borrowing costs exceed the economy’s long-run growth rate – as they do now – it’s a reliable sign that monetary policy is restrictive, and that’s historically been a headwind for equities.

Crucially, the near-term trajectory is almost entirely hostage to geopolitics. Each day without a US-Iran agreement gives the Treasury market impetus to push yields higher still.

Where Markets Could Be Wrong

While markets are bracing for a hike, the bar for it is high – much higher than a cut. The Federal Reserve has been data-driven and deliberate in its decision-making, not reacting to short-term market swings or news headlines. And when you strip energy out of the inflation numbers, US “core” inflation (ex-food and energy) through March has actually been moderating. That means, unless inflation returns to 2022 levels of ~7%, it’s unlikely that policymakers will rush to tighten. Disinflationary forces, from shelter to productivity gains, remain prevalent in the US economy.

Another difference is that borrowers’ fundamentals continue to be strong. Credit spreads, the additional borrowing cost for companies above the key interest rates (e.g. government bonds), are tight right now. Global bonds fell only 1% during the “correction” in the first half of May.

What It Means for You

INCOME

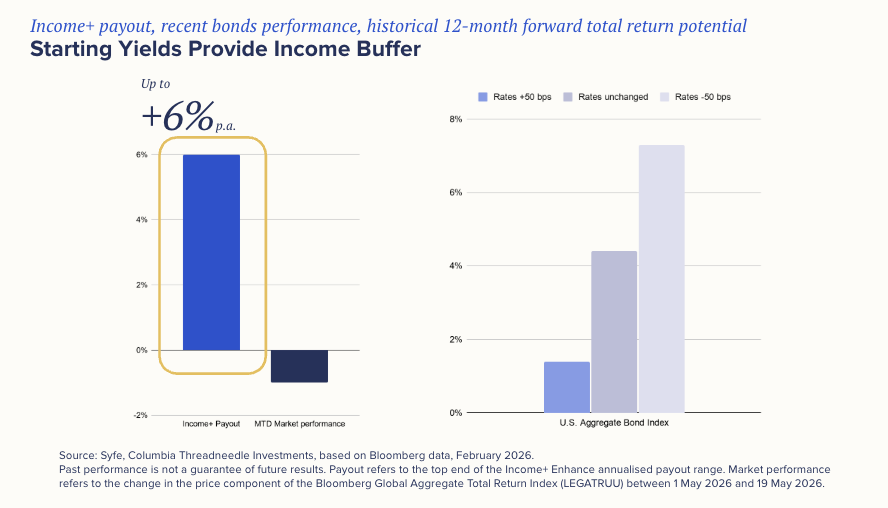

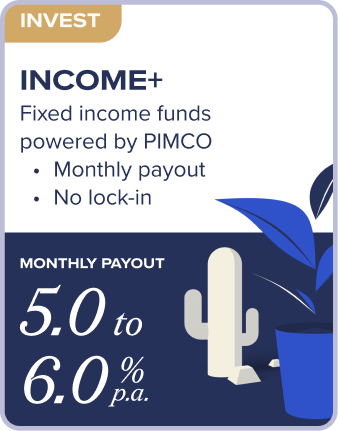

Income investors should seize this window of opportunity and lock in these yields while they can. Our Income+ portfolios are delivering 5%-6% payouts. Investors would be buying these yields at a lower cost. Higher yields provide a buffer that often supports total returns, paying investors steady, attractive income to wait for the turn in interest rates.

EQUITY

In equities, we’ve just witnessed the best US earnings season since 2021. Fundamentals are strong, with over 84% of companies beating analyst estimates, according to FactSet calculations. UBS research notes that it takes more than one hike historically to derail the stock market’s rally. Stocks could also find renewed strength if central banks shift their focus from worrying about near-term inflation to shoring up long-term economic growth.

Any recovery in the stock market is unlikely to be even, however. Investors have been getting selective this year – favouring industries benefitting from AI, countries with energy security, and companies with stronger fundamentals. They’re also less forgiving as the market gets increasingly expensive (Nvidia fell after beating estimates).

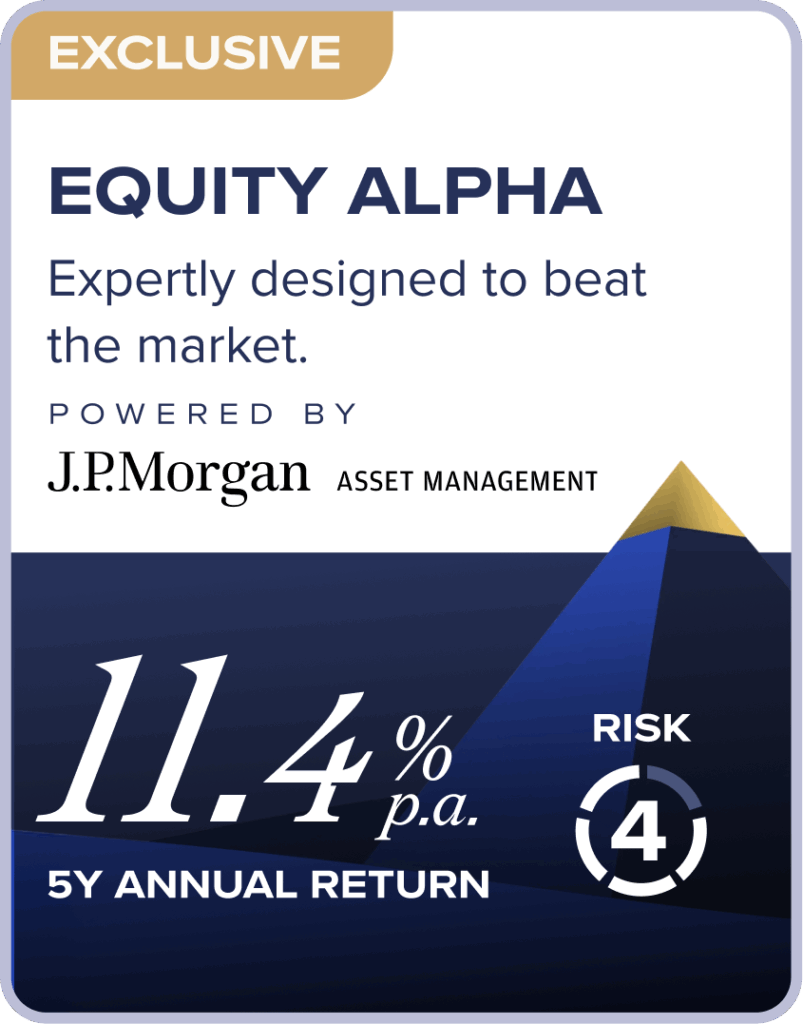

With most DIY investors still concentrated in a handful of AI winners, this is a real risk. Selection and diversification are key. Both are on offer in our newest portfolio, Equity Alpha.

Powered by J.P. Morgan Asset Management, the strategy covers 2,500+ stocks, extracting alpha by overweighting stocks with higher return potential and underweighting those with weaker fundamentals. In a market that increasingly rewards the right choices over broad exposure, that distinction could be a real returns driver for your equity or multi-asset allocation.

You must be logged in to post a comment.