With the volatility of the US elections behind us and a global effort to roll out the COVID-19 vaccines underway, the stock market appears set to move higher in 2021.

Last year, investors witnessed both the end of the longest bull market and the shortest bear market in US history. Despite the economic toll of the coronavirus pandemic, US stocks closed the year on a high. The S&P 500 was up 16.3% while the tech-heavy Nasdaq Composite gained 43.6% for the year.

As we sail into 2021, here are three themes that we see playing out for the year ahead.

Vaccines and stimulus

The world now has at least two effective vaccines with several more vaccine candidates in various stages of clinical trials. Countries have begun inoculating their citizens – in Singapore, more than 6,200 people have received their first doses.

As the pace of coronavirus immunizations picks up in the coming months, investors are optimistic this can help reopen businesses and restore the economy by the later half of 2021 or early next year.

In the immediate term, US president Joe Biden’s recently announced US$1.9 trillion stimulus package is a shot in the arm for the American economy until vaccines become widely available. Proposed measures include US$1,400 direct payouts to Americans and an increase in jobless benefits that will extend through September.

The market had rallied ahead of last Thursday’s unveiling of the new stimulus plan but reversed course during Friday’s trading. The modest pullback was not unexpected as investors questioned whether the massive stimulus package could lead to higher interest rates or tax hikes in the future.

Overall, while we’re optimistic about the stock market’s trajectory in 2021, we do see some bumpiness in the weeks ahead. The stock market will likely take its cue from the upcoming earnings season, and Biden’s stimulus plan may still face significant changes before it gets passed.

China rising

We see China’s stock market bull run as another key trend accelerating in 2021.

The Chinese economy has returned to almost pre-pandemic output levels after shrinking 6.8% in the first quarter of 2020 due to the initial lockdown after their coronavirus outbreak. While the US and parts of Europe grapple with a resurgence of coronavirus cases, domestic production, tourism and retail consumption are all up in China.

Reflecting the post-pandemic recovery, China’s CSI 300 index, which tracks the 300 biggest firms listed on the mainland, surged 27.2% in 2020. This gain handily outpaces the S&P 500’s increase. Likewise, the Shanghai Stock Exchange Composite Index, which tracks the performance of all A-shares and B-shares listed on the Shanghai Stock Exchange, was also up 13.9%.

Will Chinese equities overtake US stocks?

According to the Centre for Economics and Business Research, the Chinese economy – currently the world’s second-biggest – is set to overtake the US faster than previously anticipated. This comes as China has weathered the pandemic better than the US. The Chinese has also been charting a new development strategy of focusing more on its domestic market.

Will the same apply to Chinese equities? Over the past decade, US stocks have broadly outperformed a basket of international developed and emerging market stocks. But last year, Asian stocks surged to top gains of their US peers.

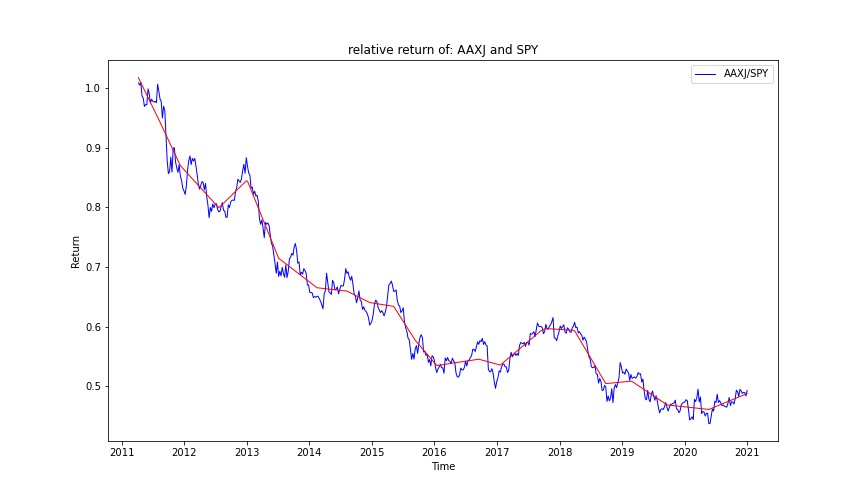

For the purpose of our analysis, we took US stock returns to be represented by the SPDR S&P 500 ETF (SPY) and Asian stock returns to be represented by the iShares MSCI All Country Asia ex Japan ETF (AAXJ).

The above chart AAXJ/SPY shows the relative performance of both funds. An uptrend indicates that AAXJ is performing better than SPY and vice versa. We can see that from 2017 to 2018, Asian equities outperformed before falling back. In 2020, Asian equities were once again in the lead.

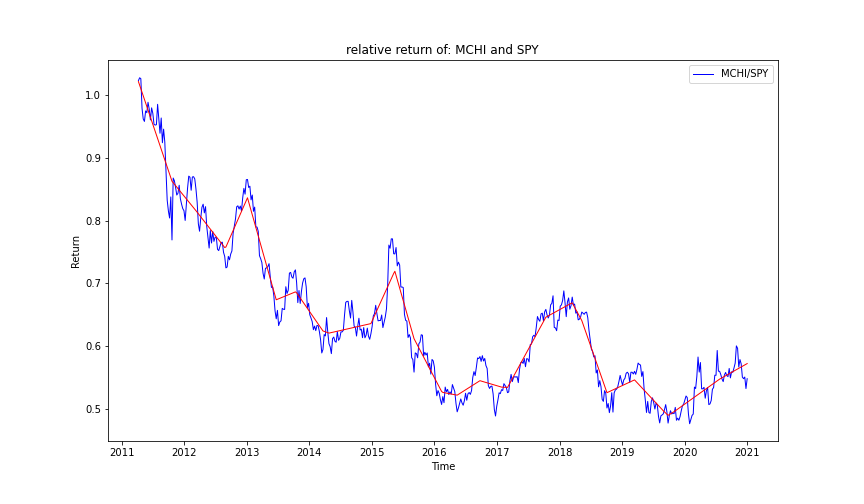

Given that 43.4% of AAXJ’s underlying holdings are domiciled in China, we then looked into comparing the performance of Chinese equities (represented by the iShares MSCI China ETF (MCHI)) and US stocks.

The chart MCHI/SPY above shows how much the MCHI, which tracks the MSCI China Index, has surged relative to the SPY in 2020. We can conclude that a significant driver of AAXJ outperformance stemmed from the strong gains made by Chinese equities last year.

China stocks are poised for a repeat of 2020

Although it may be too soon to tell whether Chinese equities will eventually overtake US stocks, there are signs that the current bull run will continue to gather steam well into 2021.

First, China will likely continue to benefit from low interest rates worldwide, the massive liquidity in global financial systems, as well as its rapid post-pandemic rebound.

In its China outlook report, Goldman Sachs noted that China is poised to deliver “one of the strongest and fastest macro recoveries in 2021 among major economies globally”. The investment bank forecasts a 20% rebound in Chinese corporate profits, and is overweight on Chinese equities.

Likewise, Morgan Stanley also remains overweight China. It has forecasted “solid” earnings growth for Chinese companies amid a potentially more stable US-China trade environment under Joe Biden, and a more broad-based global recovery in 2021.

Dividends make a comeback

Dividends were one of the first things companies cut during the pandemic as they looked to preserve cash amidst the ensuing economic shutdowns.

Despite headwinds caused by the pandemic, S&P 500 companies paid out a record $58.28 per share in dividends in 2020. This was 0.7% higher than 2019’s record, data from S&P Global show. This was mainly due to a stronger-than-expected payment in Q4 2020 and a strong Q1 payout before the pandemic struck.

For 2021, dividend stocks could come back in favour as corporate balance sheets are repaired. According to Tony DeSpirito, chief investment officer of US fundamental active equity at BlackRock, S&P 500 dividend cuts peaked in May and have since stabilized. The firm expects “dividend growth to resume in 2021 as vaccine distribution and greater clarity in general give company managements the confidence to release excess cash in the form of dividends and buybacks.”

This trend is likely to apply to Singapore REITs as well. The dividend drop for many S-REITs in 2020 stemmed mainly from rental reliefs granted by landlords to their tenants. Some REITs also decided to defer dividend payouts to retain capital, as allowed under COVID-19 relief measures announced by the Inland Revenue Authority of Singapore.

With Singapore now in Phase 3, the worst is over for many S-REITs. We should expect to see more of them raise dividends in 2021.

Conclusion

As long as interest rates remain lower for longer around the world, equities should offer attractive return prospects in 2021, supported by very loose monetary policies globally and continued fiscal support.

Analyst forecasts for global equities also see 2021 corporate earnings exceeding 2019 results. This should provide further support for equities over the course of the year. Nevertheless, there is bound to be short-term corrections in between.

For investors, our advice remains the same. Focus on the long-term and stick to your investment plan. As 2020 proved, the best days usually follow the worst days for the market.

By Richard Yeh, Head of Portfolio Construction and Risk Management, Syfe

You must be logged in to post a comment.