As 2024 begins, the investment landscape is marked by guarded optimism and strategic caution. The US equity market approaches record highs, the Fed deliberates on policy shifts and China confronts economic headwinds. Against this backdrop, investors face a complex environment filled with uncertainties.

During our 2024 Investment Outlook event, we have received many questions from participants eager for guidance. Here are our investment team’s answers to the six most frequently asked questions.

US Equities

Q1. Is it still a good time to invest in US equities in 2024?

- After a 25% rise last year, US equities are expected to deliver more modest returns in 2024, as valuations are on the higher side.

- For the economic outlook in the US, even though the base case scenario is for a soft landing, the risk of a pronounced economic slowdown cannot be ruled out.

- Having said that, one lesson from 2023 is the difficulty of predicting market movements. Those who completely stayed out of the equity market last year missed the rally.

- Our advice is to stay invested but also to build more resilience into your portfolio. You can consider diversifying part of your portfolio into bonds, which currently offer attractive opportunities.

Bonds

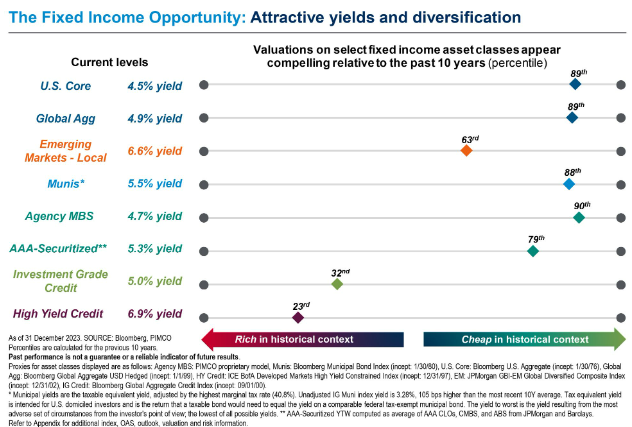

Q2. When shall I deploy cash to bonds?

- It may not be prudent to wait for the Fed to start cutting rates before buying into bonds.

- The key reason is that the market always moves ahead of the news, often preceding the Fed’s actions.

- Currently, the market has priced in scenarios for a soft landing, but a more pronounced economic slowdown has not yet been reflected in prices. Based on the average valuation over the last 10 years, most subsectors of bonds are still attractively valued.

Q3. How long do we stay invested in the bond market for a decent return?

- The total return of bonds consists of two components: yields and price movement.

- Currently, bond yields are at a 15-year high. Regarding price movements, bond prices are negatively correlated with interest rates; that is, when interest rates decrease, bond prices tend to move higher. As the Fed transitions from rate hikes over the last two years to rate cuts in 2024 and 2025, bond prices could be supported.

- Given the current market conditions, investors may not need to stay invested for an extended period to see a decent return.

China

Q4. What could be the catalyst for China’s equity markets this year, given the ongoing property market downturn?

- China is undergoing a transition from investment and infrastructure-led growth to consumption-driven growth. However, downturns in property and equity markets have dampened consumer confidence.

- To stablise the economy, the government needs to implement more policy supports. The government is cautious now, as too much monetary easing could put pressure on its currency, the Chinese Yuan .

- As the Fed moves to cut rates, China’s central bank, the People’s Bank of China (PBoC), could have more room to maneuver its monetary policies. More aggressive policy supports, including quantitative easing, could be the catalyst for the Chinese stock market.

Japan

Q5. Why did the Nikkei index jump so much recently despite some structural issues such as an aging population?

- One reason for the surge is the improvement in corporate governance among Japanese companies. The Tokyo Stock Exchange has put pressure on Japanese corporations to return cash to shareholders, leading to record levels of buybacks last year.

- Policymakers have made efforts to redirect corporate profits towards households, increasing labor bargaining power, and consequently boosting consumption and investment.

- Other factors, such as outflows from China and optimism from prominent investors like Warren Buffett, have bolstered sentiment.

- These factors have driven inflows into Japanese equities from both domestic and foreign investors, highlighting a renewed confidence in Japan’s market potential.

Singapore REITs

Q6. Are S-REITs still a good investment in a higher for longer interest rate environment?

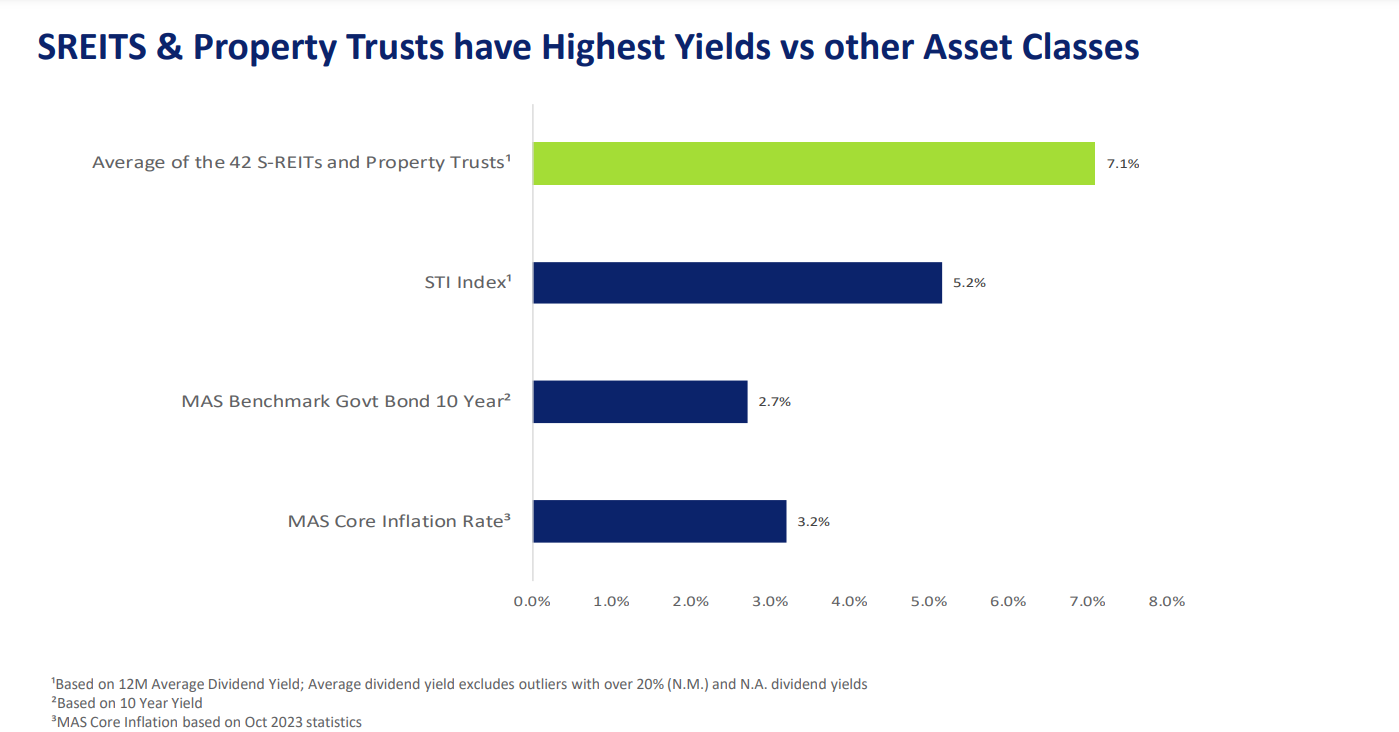

- S-REITs still offer a unique opportunity for investors, especially for those looking to build passive income. The average yield of S-REITs is 7.1%, which is much higher than that of other asset classes.

- The fundamentals of S-REITs are sound, with an average gearing ratio around 38%. REITs managers actively manage the balance sheets and interest rates.

- Currently, the price-to-book ratio stands at 0.9X, below the long-term average of 1.03X, making it attractively valued.

- As the Fed has signaled a shift towards rate cuts in 2024, this development could remove one of the primary headwind for S-REITs and serve as a catalyst for price recovery.

Read more:

Watch Market Outlook 2024:

You must be logged in to post a comment.