With Singaporeans’ life expectancy at birth rising to 84.8 years, being prepared for a long – and hopefully healthy – retirement is a reality more of us need to start contemplating. As Prime Minister Lee Hsien Loong announced during the National Day Rally 2019, changes will be made to the retirement age, re-employment age and CPF contribution rates to support retirees and boost their financial independence.

Here’s how the new announcements will affect you and a quick refresher on the key things you should know about CPF.

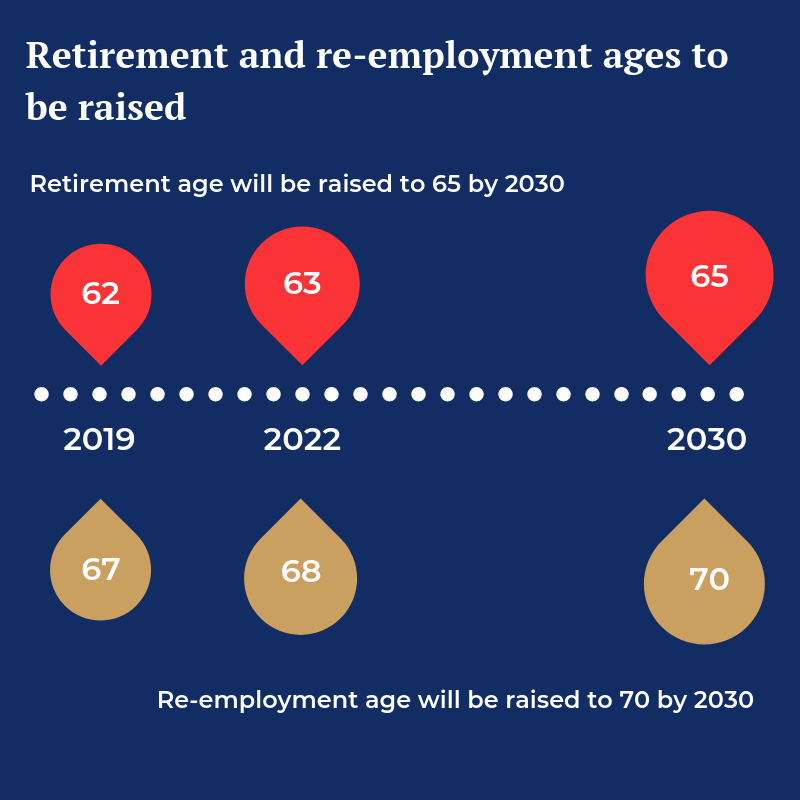

Higher retirement age and re-employment age

The current minimum retirement age of 62 will be increased to 65 by 2030. This does not mean you have to keep working till 65. It just means that from year 2030, your company cannot dismiss any employee below 65 just because of their age.

If you would like to keep working for longer, you have the option to do so as well when the re-employment age is increased from 67 to 70 years old by 2030. The new changes mean that by 2030, employers must offer re-employment to eligible staff who turn 65, up to age 70, with the flexibility to adjust contract terms.

The change will be made incrementally – the retirement age will be first raised from 62 to 63 and the re-employment age from 67 to 68 by July 2022

Change in CPF contribution rates

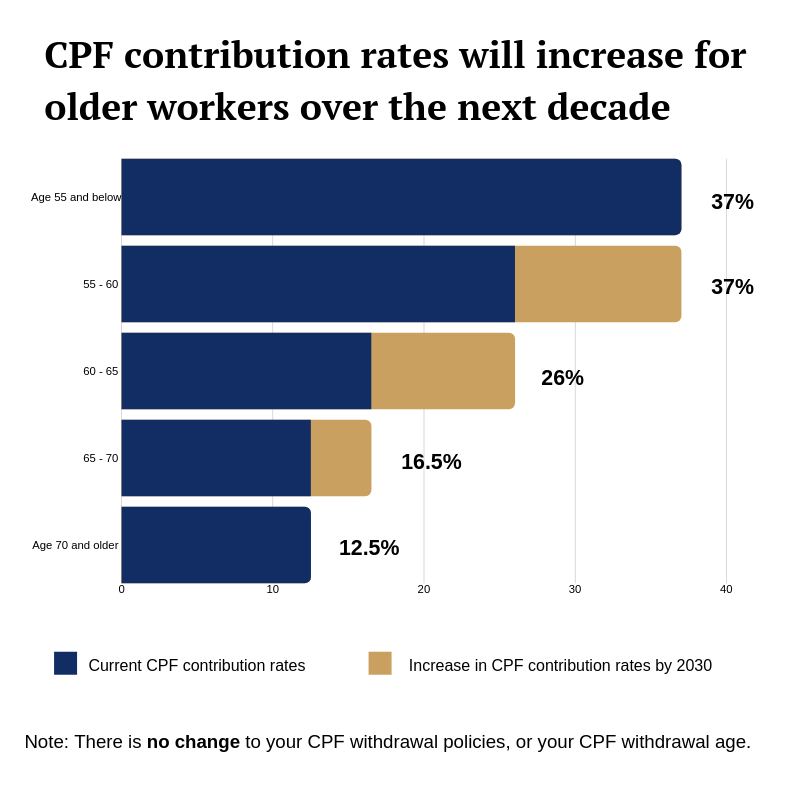

Over the next decade or so, progressive steps will be taken to raise CPF rates for workers aged above 55 to 60 to the full 37% CPF rate. CPF contribution rates for workers today begin to taper down after they turn 55.

The change enables workers aged 60 and below to enjoy full CPF rates for more years, helping them shore up their retirement savings. The additional CPF contributions will all go into the Special Account (SA).

The first rate hike is expected to be implemented in 2021 to boost retirement adequacy for older workers between 55 and 70.

The whole implementation is expected to take 10 years, depending on overall economic conditions.

Do note that there are no changes to the CPF withdrawal policies and ages. This means you can still withdraw some of your CPF savings at 55 and receive your CPF LIFE payouts from age 65.

Still unsure? Read on for our refresher on the key CPF policies to know.

6 things you must know about CPF LIFE

You don’t have to sign up for it

You’re automatically enrolled in the CPF Lifelong Income For The Elderly (CPF LIFE) scheme if you’re born in 1958 or after, and have at least $60,000 in your Retirement Account six months before you reach 65.

At 55, your RA is created for you, and savings from your Ordinary and Special Accounts (OA and SA) are transferred to your RA, up to the Full Retirement Sum (FRS).

BRS, FRS, ERS are not that confusing

Depending on your desired CPF LIFE monthly payout and CPF balances, you can choose to set aside the Basic, Full or Enhanced Retirement Sum in your RA.

The retirement sums for those turning 55 in 2019 are as follows. These sums increase every year.

- Basic Retirement Sum (BRS): $88,000

- Full Retirement Sum (FRS): $176,000 (two times the BRS)

- Enhanced Retirement Sum (ERS): $264,000 (three times the BRS)

Someone who sets aside the BRS will receive lesser monthly payouts compared to someone who sets aside the FRS. If you’re willing to pledge your property to CPF – i.e. when you sell or transfer your property, you agree to put a certain amount of the proceeds back into your CPF to make up your FRS – you can choose to set aside the BRS.

If you don’t own a property or wish to receive the full monthly payout, you can choose to set aside the FRS.

There are 3 CPF LIFE plans to choose from

The plans you select determine how your payouts are paid monthly. The Basic Plan has lower monthly payouts but lets you leave more savings for your beneficiaries. The Escalating Plan has lower payouts initially but increases by 2% yearly to help account for inflation. The Standard Plan is the default plan.

You can choose your preferred CPF LIFE plan anytime from age 65 to age 70. If you do not choose a plan before age 70, you will automatically be placed on the CPF LIFE Standard Plan.

You can get higher CPF LIFE payouts

If you have other income sources and don’t need the payouts at age 65, you can defer your payouts to earn more interest on your CPF savings. The latest you can start your CPF LIFE monthly payout is at age 70. Even if you have started receiving your payouts, you can still defer your payouts anytime up to age 70. In both cases, your monthly payout will increase by up to 7% for every year of deferment.

You (or your family members) can also make cash top-ups and / or CPF transfers into your RA, up to the prevailing Enhanced Retirement Sum. This will increase your monthly CPF LIFE payouts as well. To determine if you may need higher monthly payouts, use the CPF LIFE estimator to estimate your monthly payout based on your RA savings.

You can withdraw up to 20% of your RA balance when you turn 65

This is only applies to CPF members who did not set aside the BRS or FRS, and are born in 1958 or after. They will be able to withdraw a lump-sum of up to 20% of their RA savings at age 65. The amount is inclusive of the first $5,000 Singaporeans can withdraw from their RA at age 55.

If you had set aside the BRS or FRS at age 55, you can already withdraw your remaining CPF savings above those sums. In fact, you can apply to withdraw your CPF savings at any time after age 55, as long as you have withdrawable CPF savings.

Use the CPF WIthdrawal calculator to compute the amount that you can withdraw when you reach 55,

If you pass away, your savings are not absorbed by CPF

When you join the CPF LIFE Standard Plan for instance, CPF deducts all the savings in your RA as your annuity premium, which will be paid into the Lifelong Income Fund from which you receive your monthly payouts.

If unfortunately you pass away after receiving just $10,000 in monthly payouts, CPF will refund the unused portion of your annuity premium, without interest, back into your CPF account. This amount plus any CPF RA savings left over, will be bequeathed to your CPF nominee(s) or next of kin(s), if you haven’t made any CPF nominations at the time of your death.

The bottom line

Remember, your CPF payouts should not be your main source of income during retirement. If you want to comfortably enjoy your golden years, you have to be aware of how much you need to retire and plan for it accordingly.

For more details on how to invest strategically to grow your retirement fund, download our free Retire With Confidence e-book. If you prefer a more hands-on approach to retirement planning, join us at our upcoming retirement workshop to learn how you can work out your retirement income needs and invest for the retirement you deserve.

You must be logged in to post a comment.