A happy retirement requires planning and preparation. To be sure, a retirement that is happy and enjoyable requires more than just money — think interesting hobbies, meaningful pursuits, mental and physical health, but being financially secure will set the tone for your golden years. With average life expectancy forecast to increase to 85 years by 2040, many Singaporeans are potentially looking at a retirement of 30 years or longer.

To make the most of your retirement (and ensure your nest egg lasts), having a sound retirement plan is key. Here’s how to get yourself on the path towards financial security.

Know your expenses

Think about the kind of retirement you want and the lifestyle you would like to lead. Your retirement income will need to be enough to sustain your ideal retirement lifestyle and cover any unexpected expenses you may face in old age. Consider what age you plan to retire and how long your retirement funds might need to last – did you know that there were about 1,200 Singaporeans who lived beyond 100 in 2017?

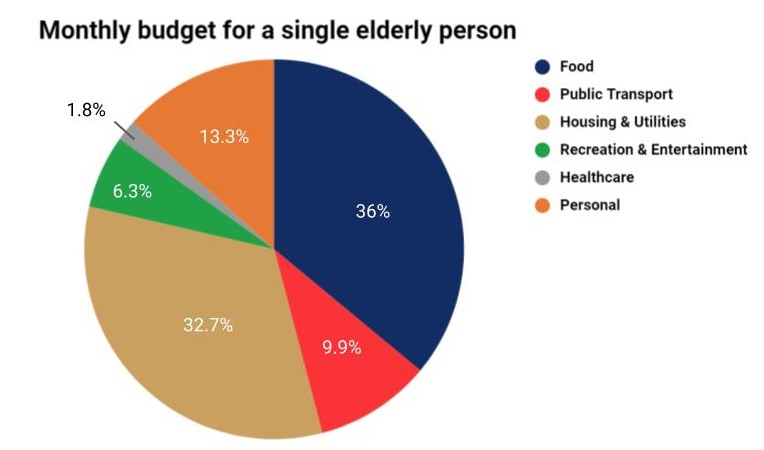

Have a good estimate of your expenses and be prepared for how that might change in retirement. A recent study by the Lee Kuan Yew School of Public Policy found that a single elderly person would need $1,379 each month just to meet basic needs, with food and housing taking up close to 70% of the monthly budget.

The study estimated the healthcare budget based on standard health services currently administered at public polyclinics but it’s worth noting that this figure could change with elderly healthcare costs (including public expenditure, private insurance, and out-of-pocket spending) projected to hit $51,000 for each elderly person by 2030.

Don’t forget to account for inflation in your budgeted expenses as well. It’s likely that Singapore’s already high cost of living could increase further by the time you retire.

Determine your CPF LIFE payouts

Once you have a sense of how much money you need to bring your retirement dream to life, make use of the online CPF LIFE Payout Estimator to estimate your monthly CPF payouts.

Under CPF LIFE, Singaporeans can start receiving monthly payouts from age 65 – and for as long as they live – to help meet their basic needs. CPF LIFE payouts give you a regular income stream, but don’t make the mistake of assuming they can provide for all your retirement expenses.

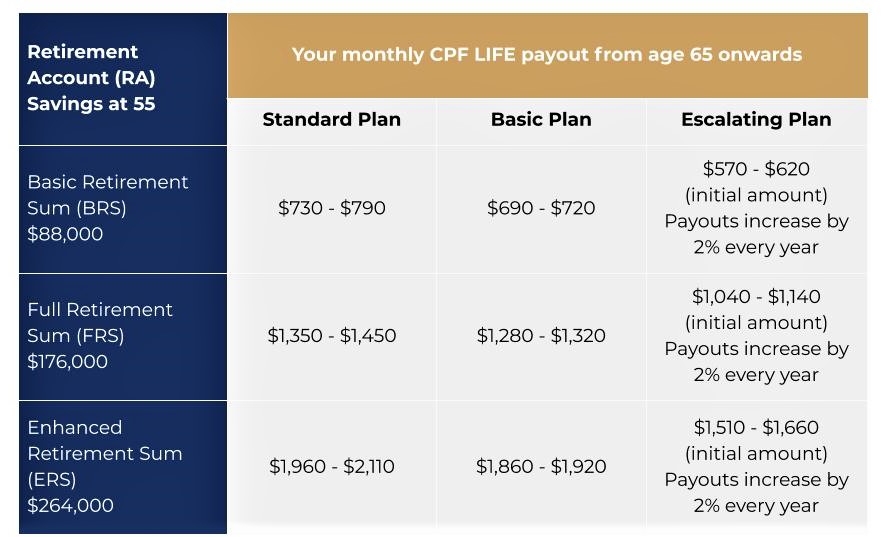

As you recall, a single elderly person would need $1,379 each month just to meet basic needs. That’s almost double the average $760 a retiree would receive under the Standard Plan for CPF LIFE payouts, assuming he only meets the Basic Retirement Sum (BRS) in his CPF Retirement Account (RA).

You can see from the table above that the estimated monthly CPF payouts (computed as of 2019) range from $570 to $2,110. Will your CPF LIFE payouts alone be enough to fund all your retirement expenses, based on what you have calculated earlier?

Grow your retirement nest egg

Regardless of the size of your paycheck, it’s understandable that you may feel unsettled at the thought of not drawing a regular salary anymore. Your golden years is when you start drawing down the money you have accumulated. You need to ensure there’s enough to carry you throughout your life in retirement.

How you invest – or don’t invest – your retirement savings could be a critical determinant of the size of your retirement income stream. While the right investment strategy for you will depend on your goals, time horizon and risk tolerance, there’s a reason why financial experts frequently advise that the best time to invest was yesterday.

For simplicity, let’s assume you invest $100 a month at a 5% annual interest rate. You begin at age 35, socking away $100 every month until age 65. By 65, you will have about $83,573 in your account.

If you begin investing at age 45, you will have $41,475. An extra 10 years of saving (and only $12,000 more of your savings) nearly doubles the balance in your account at age 65.

As the figures above show, you will only have $15,593 at age 65 if you start saving at 55. That’s the power of compounding returns. The earlier you start investing, the more time your money has to grow, and the larger your retirement nest egg will be.

Consider passive investing with ETFs

Investors in Singapore are spoilt for choice when it comes to investment types. But if you want a simple, cost-effective strategy to grow your retirement savings over the long term, passive investing is a smart choice.

It’s also a strategy favoured by billionaire investor Warren Buffet who famously won a US$1 million bet that investing in a low-cost stock index fund (a form of passive investing) will outperform most actively managed hedge funds. Buffett’s chosen index fund returned 7.1% compounded annually, while the basket of hedge funds his opponent picked returned an average of only 2.2%.

In recent years, exchange-traded funds (ETFs) have emerged as a popular passive investment that facilitates low cost diversification. ETFs track an index and aim to replicate the performance – and returns – of the index at a low cost.

Alternatively, digital wealth managers like Syfe can help you select the right ETFs for your portfolio as well. Syfe’s investment methodology is rooted in passive investing, which means we use low-cost ETFs to build our clients’ globally diversified portfolios. Investing in a broad portfolio of ETFs can now be as simple as opening an account with Syfe.

The bottom line

If you want more comprehensive guidance on how to earn healthy, long-term retirement income, download Syfe’s Retire With Confidence guide. Here’s what you will get:

- Tips on optimising your CPF savings

- How to create a diversified investment portfolio using ETFs

- Retirement planning case studies

Having a large enough nest egg is a key part of the formula for a happy retirement. You have already taken the first step of putting together a solid retirement plan. The next step is simply following through with it.

You must be logged in to post a comment.