This article was first published in The Business Times.

Table of contents

- The basics of CPF

- What is the proportion of CPF members who invest their CPF-OA assets?

- How much do CPF members invest?

- CPF-OA and CPF-SA savings as bonds?

- What the experts say about CPF investing

- The value of certainty at the end of a bull run?

- Focus first on putting uninvested cash to work

Saving for retirement is one of the most important investment goals and for many of us, assets in CPF could be a major source of investable assets.

Why are we writing this?

This topic and more broadly CPF has gained momentum recently as many in Singapore are accumulating a large amount of their wealth in CPF, and are considering all the ways to work their money harder.

“Should I invest my CPF” is one of the top searches on Google! There are a lot of materials available on the mechanics of how to invest your CPF assets, including what you can invest in, and how to find the cheapest way to do so but the most important question of whether one ends up better off forgoing the 2.5% guaranteed return is inadequately addressed.

This seemed too abstract to tackle: on the one hand, high single digit to low double digit investment returns are being advertised, which makes one want to forgo the 2.5% guaranteed annual return for CPF-OA savings. However, looking at total profit and loss statistics based on a Straits Times article: from October 2019 to September 2020 (post a market correction), 1 in 2 people who invested their CPF savings ended up worse off.

In this post, we wish to address whether investors should invest their CPF savings by making the question less abstract:

1. How did two similar investors with S$50,000 fare depending on whether they invested their CPF-OA assets?

2. What well known investors like Jack Bogle (the founder of Vanguard who popularised index funds and ETFs) had said on the topic

3. So, should I invest my CPF-OA assets?

Before we get into it, the basics of CPF:

We have linked resources here if you want to find out more but the basics are:

What is the proportion of CPF members who invest their CPF-OA assets?

Based on CPF statistics, there are more than 4 million CPF members. 977,000 of those members invest their CPF-OA assets. This works out to be roughly 1 in 4.

How much do they invest?

CPF members have $520bn in assets, $176bn in CPF-OA and $131bn in CPF-SA. Approximately $17bn (based on the latest annual report from CPF) of CPF-OA savings were invested, working out to be under 10% of total CPF-OA assets.

Average OA Amount Per CPF Member = $42,000 (rounded off to nearest $1,000)

Average investable savings in CPF-OA = $42,000 – $20,000 = $22,000

Average CPF-OA savings invested through CPFIS (CPF Investment Scheme) = $17bn / 977,000 members = $17,000 (rounded off to nearest $1,000)

CPF-OA and CPF-SA savings as bonds?

CPF-OA savings earn 2.5% annually, and 1% higher for the first $20,000 for those under 55 years old. For CPF-SA, since the guaranteed interest rate is higher, the threshold for investing these assets would naturally be higher as well.

CPF-OA and SA savings and fixed income share some common traits, especially when we zoom into government guaranteed bonds specifically. There are some differences ostensibly given the structure of CPF to begin with and how it differs from cash.

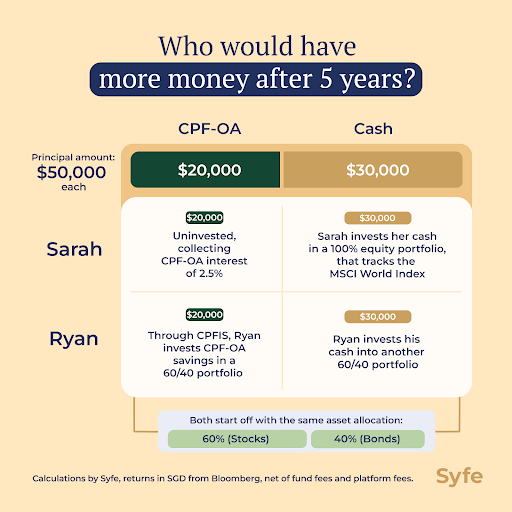

Sarah or Ryan: Who would have more money?

Assuming there are two individuals: Sarah and Ryan1 have $50,000, $30,000 (60%) in Cash and $20,000 (40%) in CPF-OA savings that can be invested. They acknowledge that they will not need these assets for five years at least.2

Sarah and Ryan have a 60% equities and 40% fixed income asset mix overall. Who do you think would have more money at the end of five years and ten years?

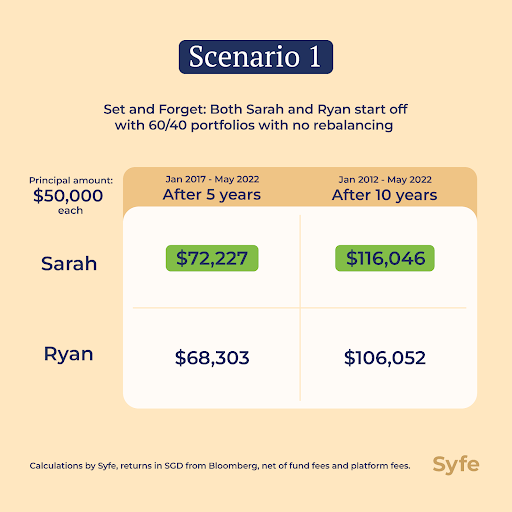

Scenario 1: Sarah and Ryan invest through digital wealth platforms. Sarah invests in an ETF tracking MSCI World (Global Equities) with returns in SGD while Ryan’s 60/40 portfolios are also in SGD and consist of mutual funds.3

Ryan and Sarah take a fire-and-forget approach; they do not rebalance their portfolios. At the end of 2021, Sarah’s portfolio has a larger allocation to equities than she started with.

Sarah ends up with almost $10,000 more than Ryan even when the investment period is extended to be more than 10 years.

Scenario 2: As their portfolios are not rebalanced in Scenario 1, Ryan’s portfolio maintains a 60/40 allocation while Sarah’s portfolio drifts and ends up closer to a 80/20 allocation in 2021 as the equity portion of her assets grew much faster.

In Scenario 2, we assume that Sarah rebalances her portfolio at the end of each year. Say at the end of 2013, Sarah’s portfolio had a 66% allocation to equity, she would allocate 6% (66-60%) to CPF. As one cannot withdraw from CPF before retirement age, if her portfolio goes to 58% equity, she would not re-allocate CPF assets to bring the equity portion back to 60%.

Even with annual rebalancing, Sarah still ends up better off!

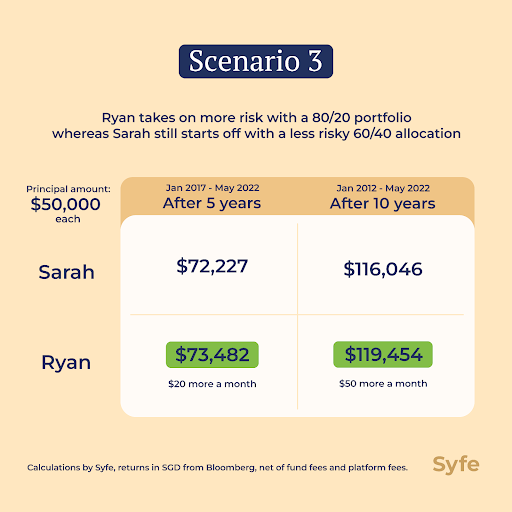

Scenario 3: What if Ryan increased his allocation to equities, instead of a classic 60/40 portfolio, how much more money would he get if he went for an 80/20 allocation instead, similar to Sarah’s drifted portfolio allocation by 2021 in Scenario 1?

Sarah has the same assets here as in Scenario 1 and starts off with a 60/40 portfolio.

Even with taking on more risk through a higher allocation to equities, Ryan’s portfolio only marginally outperforms Sarah’s. He stands to gain about $20 more a month from 2017 and $50 dollars more a month from 2012. Sarah still starts off with a 60/40 portfolio.

What the experts say…

Jack Bogle, founder of Vanguard and best known for revolutionising passive investing, is a strong supporter of considering the defined contribution equivalent of CPF, US Social Security benefits, as part of an investor’s fixed income weighting in their investment portfolio. Otherwise, one ends up being over-allocated to bonds and under-allocated to equities.

David Blanchett who runs retirement research at PGIM and Paul Kaplan, director of research at Morningstar studied different portfolio implementation decisions and the effect on certainty-equivalent income over time. In other words, as the certainty on the value of CPF assets is higher than invested assets, that certainty carries intrinsic value and also opportunity cost.

As markets may remain volatile post the worst start for US equities in 50 years, investors grow to appreciate CPF’s guaranteed return and the lack of volatility, considering CPF as ballast for stability.

The value of certainty at the end of a bull run?

We looked at medium to long term investment periods (5-10 years) for a lump sum investment. In the last ten calendar years there has been a bull run for financial markets, especially for equities! As this bull run has come to an end, the value of certainty has increased.

Sarah, who left her CPF-OA assets un-invested and considered it as her portfolio’s bond component while building her own 60/40 portfolio fared better than Ryan, regardless of whether she used a fire-and-forget approach or rebalanced her portfolio every year.

There is merit in having CPF-OA savings work as they are intended as there are almost no alternatives to 2.5% guaranteed returns annually.

Focus first on putting uninvested cash to work

Many regard CPF savings as “can see but cannot touch”, but it does not mean that CPF-OA savings are more “expendable”. In fact, CPF savings come with a higher opportunity cost as compared to cash due to its guaranteed return.

Ultimately, investing comes down to risk and return; and how to maximise returns while keeping risk capacity in check.

Our goal at Syfe is to help build long term wealth. As our research has shown, considering the guaranteed return of CPF-OA (like a bond allocation that never loses value) as a safety net enables investors to maximise the potential returns of investments made with cash. Furthermore, we would advocate for deploying cash before deploying CPF-OA savings for investments.

The three core principles underpinning our investment philosophy is diversification, cost-effectiveness, and to build wealth for the long-term. These core principles would apply for investing, regardless of the source of funds: CPF-OA savings or cash.

1 Fun fact: Popular names for babies in the 1980s in Singapore

2 Why did we use these figures? Based on official statistics from CPF:

Sarah puts all her cash assets in a 100% equity portfolio, assuming that it tracks the MSCI World Index, and leaves her CPF-OA savings un-invested. She has built her own 60/40 portfolio, with 60% allocated to equity and 40% in CPF-OA, treating that as bonds.

Ryan invests $30,000 in a classic 60/40 portfolio through funds and the remaining $20,000 in a 60/40 portfolio consisting of CPFIS-eligible funds. These two portfolios will have slightly different historical returns as the underlying funds differ.

Average OA Amount Per CPF Member = $42,000 (rounded off to nearest $1,000)

Average investable savings in CPF-OA = $42,000 – $20,000 = $22,000 as $20,000 minimum in CPF-OA must be reached before CPF-OA savings can be invested.

Average CPF-OA savings invested = $17bn / 977,000 members = $17,000 (rounded off to nearest $1,000)

We took $20,000 as a reasonable middle figure between $17,000 and $22,000.

3 Underlying returns data used for scenarios are time-weighted, in SGD, net of platform fees, fund and ETF fees, starting from January 2012 and January 2017.

You must be logged in to post a comment.