Table of Contents

- The risks of playing it too safe with SSBs and T-bills

- Stocks and bonds have historically outperformed cash

- What to do with your excess cash

- The takeaway

2022 has been a challenging year for investors. The S&P 500 is down about 22% to date while bonds – typically seen as ballast for equity-heavy portfolios – have dropped about 14%.

In the midst of such volatility, many investors have flocked to the safety of cash and cash-like instruments such as Treasury bills (T-bills) and Singapore Savings Bonds (SSB).

And why not? The yields on both assets have been increasing amid rising interest rates. For instance, the latest SSB issue offers a 10-year average annual return of 3.21% while the 6-month T-bill issued in September reached a 3.32% cut-off yield.

The risks of playing it too safe

SSBs and T-bills offer capital protection and guaranteed returns, attributes which are valuable in these uncertain times. No one doubts their place as part of a well-diversified investment portfolio.

But while this approach may be “safe” in that it shields you from short-term market downturns, moving substantial amounts to cash may actually be damaging in the longer term. That’s because the rates paid on SSBs and T-bills are unlikely to keep pace with rising inflation.

Singapore’s core inflation rose to 5.1% in August 2022 on a year-on-year basis, driven mainly by higher prices of food and services. The rate was higher than the 4.8% reported for July. Meanwhile, headline inflation rose to 7.5% year-on-year in August.

If inflation remains stubbornly high and the yields on SSBs and T-bills continue to lag behind Singapore’s inflation rate, the value of your cash will erode over time.

What happens if inflation moderates? Interest rates would likely fall, and the yield on future issues of SSBs and T-bills would drop in tandem. For example, before the pandemic, the average 10-year annual return for each monthly SSB issue was 2.38% in 2018 and 2.05% in 2019.

Are such returns good enough for your future goals?

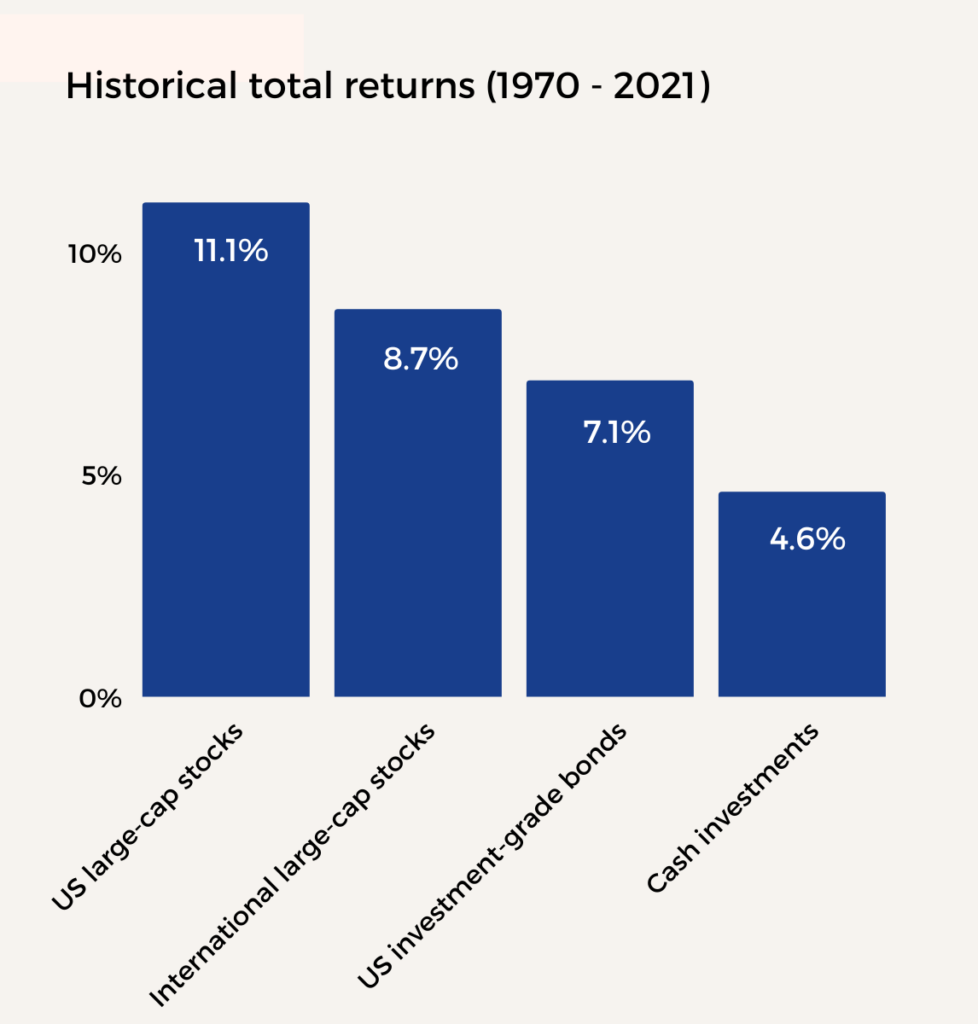

Stocks and bonds have historically outperformed cash

For long-term investors, there’s value in sticking with a diversified portfolio of stocks and bonds. That’s because stocks and bonds have historically outperformed cash. The world experienced four global recessions between 1970 and 2021, but the total returns (income and price appreciation) for stocks and bonds still outstripped that of cash.

Market volatility can be upsetting. But before you exit your investments and flee to cash, consider this. Stock markets will fluctuate in the short-term but they tend to trend upwards over time. Moreover, market advances have historically occurred more frequently – and in greater magnitude – compared to declines.

What to do with your excess cash

Say you’ve decided that your current investment portfolio is attuned to your overall risk appetite and investment goals, and you’re committed to staying invested.

But you’re wondering what to do with your excess cash. Here are some considerations that can guide your decision.

- What are your reasons for holding cash?

- How liquid do you need your funds to be?

- What returns do you need your cash to provide?

For example, if you’re just looking for a place to park your cash untouched for six months to one year, T-bills can be attractive in the current environment.

If you need to be able to withdraw your funds quickly – to use as “dry powder” for attractive investment opportunities or for unexpected emergencies – consider cash management accounts. Syfe Cash+ Flexi for instance, offers a projected return of 3.7% p.a. along with same-day withdrawals. Moreover, the projected rate will automatically adjust higher as interest rates continue to rise.

But if you need higher returns than what cash instruments can provide, consider putting some excess cash to work in investments that meet your personal risk tolerance and return expectations.

For moderate-risk investors, dividend-paying stocks or REITs might be a worthwhile addition to your core portfolio. They typically provide passive income while offering some capital gains.

Able to stomach higher risk? The sell-off in stocks could be an opportunity for long-term investors to buy more stocks of quality companies at a discount.

The takeaway

Cash should form part of your portfolio, but not dominate it.

A diversified investment portfolio containing stocks, bonds, and alternatives like REITs and commodities can help you build wealth more effectively – as long as you’re prepared to think long-term.

You must be logged in to post a comment.