Table of contents

- Income, revenue, and DPU growth

- Potential pipeline

- Low leverage, low default probability

- Sponsor reputation

- Assembling a REITs portfolio

Real estate investment trusts (REITs) allow investors to reap all the benefits of being a landlord without the time, hassle, and huge financial commitment that comes with owning a physical property. Without having to change a single lightbulb, REIT investors get to receive rental income via quarterly or semi-annual REIT dividend payouts.

While REITs with a high dividend yield certainly look attractive, it is misleading to conclude that high dividend yield alone indicates a good REIT. Instead, investors need to do their due diligence and look into the other factors that determine the quality of a REIT.

Income, revenue, and DPU growth

The financial statements of a REIT (easily available on the REIT’s website) can tell you a lot about its financial health. Look for REITs that show consistent growth in gross revenue and net property income (NPI). Gross revenue for a REIT mainly comes from the rent collected from its properties while NPI is essentially what’s left after the REIT pays for all the expenses associated with operating and maintaining the properties.

But an increase in gross revenue and NPI should also come with an increase in distribution per unit (DPU). DPU is how much an investor gets for every unit they have in the REIT. A jump in gross revenue and NPI without a corresponding increase in DPU could mean that the REIT is issuing new units to raise more funds. Beyond diluting existing unitholders, an enlarged unit base can cause DPU to remain stagnant or fall because the total amount available for distribution i.e. distributable income has to be paid out to more units of the REIT.

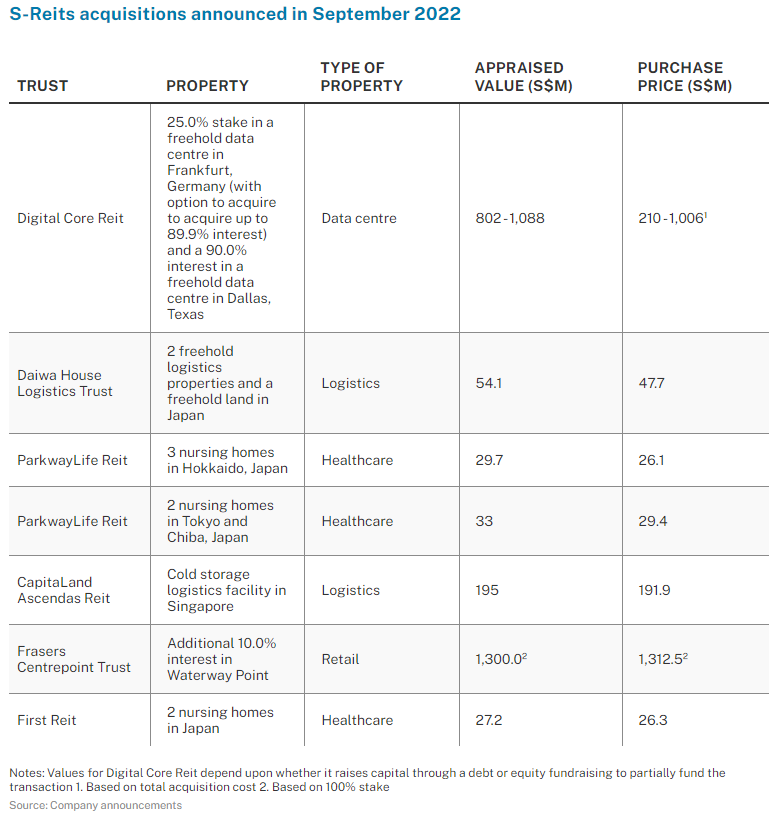

Potential pipeline

REITs with strong acquisition pipelines tend to be well-positioned for further growth. Acquisitions can help diversify portfolios while improving earnings and DPU over time.

Apart from a strong pipeline, investors should also look out for REITs that have good asset enhancement initiatives in place. Such upgrades and improvements can yield the potential for higher rental income in the future.

Low leverage, low default probability

Gearing ratio, also known as leverage, is the ratio of a REIT’s debt against total assets. A REIT with a low gearing ratio has a greater capacity to undertake more debt for future yield accretive acquisitions. Furthermore, the REIT’s interest expense is likely to be lower, resulting in higher NPI.

S-REITs are already required by the Monetary Authority of Singapore (MAS) to limit their gearing ratio to 50%. So when choosing REITs for your portfolio, pick REITs that have a gearing ratio comfortably below this limit.

Another financial ratio to look at would be interest coverage ratio. A REIT with a high interest coverage ratio is capable of meeting the interest payments on its debt without much difficulty. Even if NPI were to fall, investors can be assured that the REIT is unlikely to default on its interest payments.

Sponsor reputation

Sponsors play a large part in how the market views their REITs. REITs with well-known sponsors like Mapletree, Keppel, and CapitaLand tend to enjoy greater capital gains and larger trading volumes.

Conversely, as the First REIT saga illustrates, a sponsor with a less-than-stellar reputation can have an adverse impact on the REIT. First REIT’s share price has plunged since its sponsor, Lippo Karawaci, had its credit rating downgraded and its reputation tarnished by an alleged bribery case linked to the Lippo Group.

The importance of picking a REIT with a strong and reputable sponsor also becomes apparent when it comes to property acquisitions. A strong sponsor can give a REIT access to valuable assets through a robust pipeline of quality asset injections. This serves as a ready source of growth for the REIT.

Assembling a REITs portfolio

“Diversification is the only free lunch in investing” applies as much to REITs as it does to stocks. Maintaining proper diversification is essential when building a portfolio of REITs, which should ideally include REITs from the various real estate sub-sectors – retail, commercial, industrial, residential, hospitality and healthcare.

Other than choosing the right REITs based on the factors above, investors have to consider the market outlook for these sectors when making their choice. For investors who do not have the time or inclination to pour over financial statements, corporate announcements, and market news, they can consider Syfe REIT+, a portfolio that holds 20 of Singapore’s largest REITs.

For investors who prefer to build their own REIT portfolio, they can consider using Syfe Trade for easy and affordable access to the Singapore market. Pricing for SGX stocks is just 0.06% of traded value (minimum S$1.98), and there are no platform and withdrawal fees.

You must be logged in to post a comment.