A decade ago, investors looking for diversified exposure to the market would have turned to unit trusts, purchasing them through their banks, financial advisors or other middlemen. Today, unit trusts (also known as mutual funds) are fast losing their appeal especially when compared to the more affordable and accessible exchange-traded funds (ETFs).

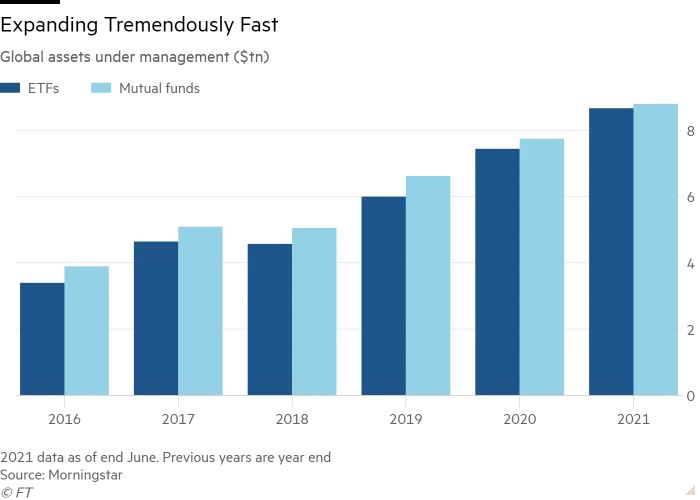

Investors are certainly making their preferences known. Global net inflows into ETFs for the first six months of 2021 totalled US$659 billion compared with US$767 billion for all of 2020, according to research and consultancy firm ETFGI.

Globally, ETF assets under management hit a record US$8.66 trillion at the end of June, just a hair’s breadth away from those in mutual funds. The gap between ETFs and mutual funds has been rapidly narrowing since 2016, a key indicator of the surging popularity of ETFs and their function as a low-cost investment vehicle.

Understanding ETFs and unit trusts / mutual funds

Both ETFs and unit trusts offer diversification benefits by holding a basket of stocks, bonds or other assets. While ETFs can be bought and sold on a stock exchange just like any other stock, investors will have to take the unit trust’s listed price at the end of the trading day whenever they buy or sell units.

Another difference between the fund types is the investment strategy used. ETFs tend to be passively managed. In other words, they are designed to closely replicate the performance of the index they track and generally hold the same proportion of securities as its index.

Unit trusts are typically actively managed. This means the fund manager aims to outperform an index benchmark by actively buying or selling securities. Success of the fund depends on whether or not the portfolio manager can consistently pick “winners”. As it turns out, that’s hardly the case.

Studies have shown over and over again that actively managed funds almost always underperform passive investments in the long run. According to the SPIVA US Scorecard for 2020, 83% of all active fund managers have underperformed their benchmarks over the past 10 years.

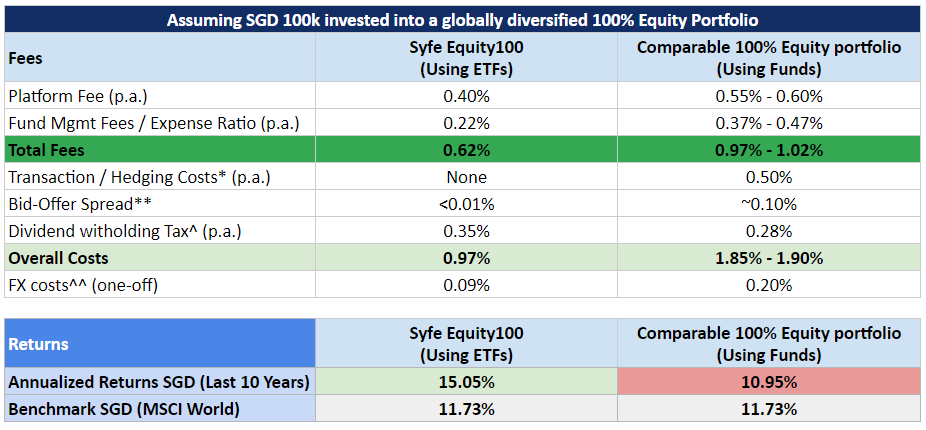

Before we delve deeper into the cost differences between ETFs and unit trusts, here’s a quick overview of the overall costs involved in an equity ETF portfolio and a comparable unit trust portfolio holding index mutual funds. While most unit trusts are actively managed, there are some that track indices passively. (Take note that actively managed mutual funds will typically have higher expense ratios compared to their index counterparts.)

The expense ratios for funds assumes them to be index funds. Active mutual funds can have expense ratios 2 – 3 times the expense ratio indicated above

*Transaction and hedging costs are estimated to be 0.5% on average based on Lumint data.

**Mutual fund bid-offer spread estimated to be approximately 0.10% based on data from National Bank Financial

^Dividend withholding tax taken as 30% for US ETFs and 15% for Irish domiciled UCIT ETF/funds. Syfe’s Equity100 dividend yield is 1.25% compared to ~1.85% estimated for a comparable 100% equity portfolio using funds

^^Syfe’s FX conversion fee is 0.09%. Funds may pay higher FX costs through banks

Expense ratio: Why it matters

Due to their passive management, ETFs often have lower expenses and costs compared to unit trusts.

High fees eat into your returns over time. An important figure to look out for when evaluating fees is a fund’s expense ratio, which can be found on the fund’s prospectus or factsheet. Investing in unit trusts typically costs more than ETFs as part of the expenses go towards the salaries of the portfolio managers and research analysts who support them.

ETFs usually have expense ratios below 0.5% while an actively managed unit trust’s expense ratio can range from 1.5% to 2% per year. A 1% difference in fees may seem minimal, but it adds up over time. If you had invested $100,000 at a 7% annual return 20 years ago, you would have ended up with roughly $350,000 today, assuming yearly investment fees of 0.5%.

But with fees of 1.5% each year, your total sum falls to around $290,000. That’s $60,000 forfeited in extra fees, more than enough for a university semester – or two – abroad!

Expense ratio alone doesn’t capture all investing costs

The expense ratio tells you a great deal about your ETF or unit trust, but it doesn’t show the full costs you’ll pay. Transaction costs and other fees such as brokerage commissions or sales charges are not included in a fund’s expense ratio.

Transaction costs

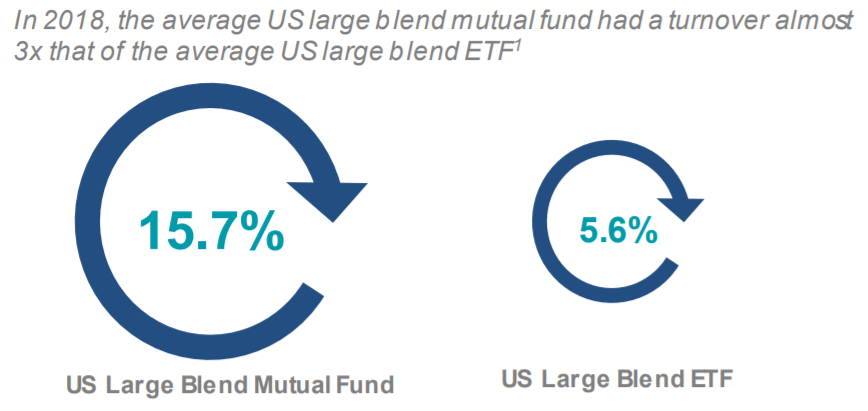

Transaction costs for actively managed unit trusts tend to be much higher compared to ETFs. Traditional open-ended unit trusts buy and sell securities based on cash flows from shareholder activity, selling portfolio holdings to raise cash to fund redemptions and buying securities using the cash received from in-flows.

ETFs, on the other hand, are traded on the exchange where sellers of ETF shares meet with buyers of ETF shares. ETFs thus typically engage in portfolio transactions only when needed, such as to track changes in the composition of the underlying index. As such, annual turnover for ETFs is usually lower, translating to lower transaction costs.

Bid-ask spread

Bid-ask spread is a common cost for ETFs, which trade like single stocks. It’s simply the difference between the price someone is willing to pay for a security (the bid) and the price someone is willing to sell that asset (the ask).

The key takeaway is that the tighter the spread, the less expensive it is to trade that ETF. From SPDR S&P 500 ETF to Invesco QQQ, many of the popular ETFs that Singapore investors have heard of tend to be highly liquid with large trading volumes. As such, the average bid-ask spread for these ETFs is usually less than 0.01%.

At Syfe, we use ETFs as the building blocks of our portfolios to keep investing costs as low as possible for our customers. This is also why we only select ETFs that are highly liquid and have negligible bid-ask spread. Additionally, we’ve optimised our trading process to buy or sell ETFs near their closing prices. This further minimises the impact of bid-ask spread on our ETF portfolios.

With unit trusts, the common assumption is that there’s no bid-ask spread because investors buy and sell their units at net asset value, which gets reported daily after market close. What investors don’t realise is that each time units are created or redeemed, the portfolio manager has to buy and sell the fund’s underlying securities and pay the bid-ask spread for those transactions. If these securities are thinly traded, the large spread could even negatively impact fund performance.

Additionally, the spread is a shared cost incurred by all unitholders on a daily basis. This is unlike the spread for ETFs, which is a one-time cost that kicks in only when the ETF is bought or sold. According to analyst estimates, the bid-ask spread for large-cap mutual funds is between 0.04% to 0.10%, and between 0.20% to 0.50% for small-cap mutual funds.

Dividend withholding tax

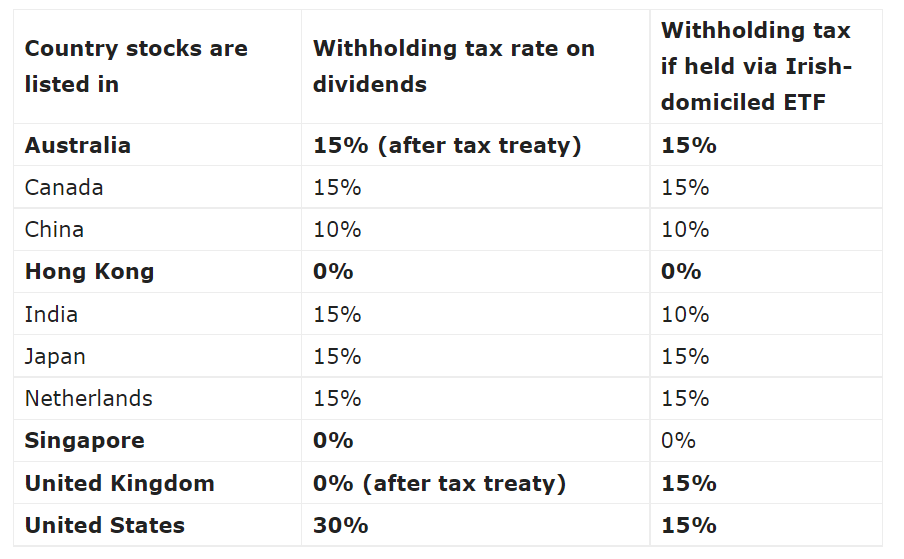

One aspect of investing in foreign shares is the withholding tax on dividends that Singapore investors need to pay. How much this withholding tax is varies according to the country the stock is listed in.

Singapore does not have a tax treaty with the US. As a result, Singapore investors are taxed a 30% withholding tax on dividends from US-listed securities (including ETFs and unit trusts). This applies whether you buy these securities through a broker, fund platform or robo-advisor.

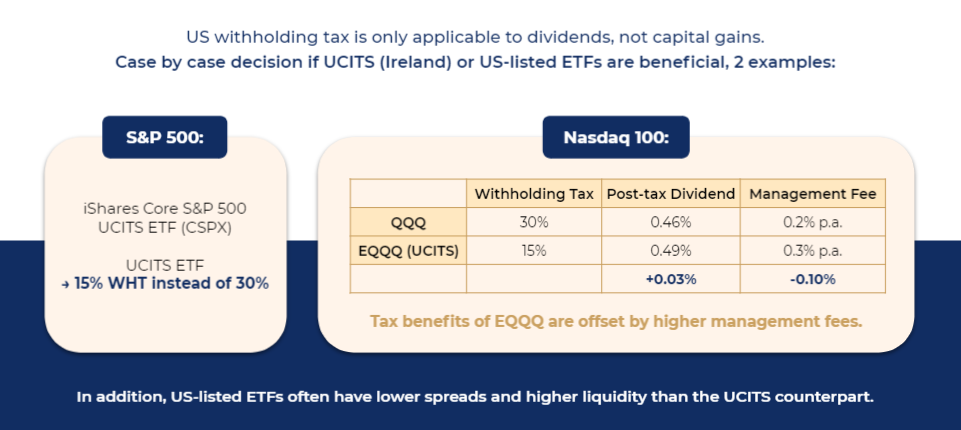

One way to get around this is to invest in UCITs products that are domiciled in European markets such as Ireland. This structure benefits from the US-Ireland tax treaty, which means your dividends will be taxed at only 15%.

However, do note that UCITs investment vehicles are only beneficial for US-listed stocks. As the above analysis from Financial Horse shows, investing in UK stocks via Irish domiciled UCITs products might actually backfire as you’d end up paying more withholding tax without the US-UK tax treaty.

At Syfe, we have weighed the pros and cons of UCITs ETFs / unit trusts carefully and will use them only when they benefit clients. Their tax advantages notwithstanding, most UCITs ETFs / unit trusts typically have higher expense ratios, lower liquidity, and wider bid-ask spreads compared to US-listed ETFs.

Let’s illustrate this with the Invesco QQQ and its UCITs alternative, the Invesco EQQQ. With a 30% withholding tax, your final QQQ dividend yield is 0.46%. With EQQQ’s lower withholding tax, you get to keep a higher yield of 0.49%. However, this additional yield is offset by EQQQ’s higher expenses.

The same logic applies when comparing US-listed ETFs and UCITs unit trusts. Although the former may have a higher tax implication, the higher TER and other trading costs associated with unit trusts outweigh any tax savings.

A final point to note is that the impact of dividend withholding tax very much depends on the dividend yield of the investment. Most investors invest in US-listed assets for capital gains, not dividends. And remember, Singaporeans are not taxed on US capital gains.

One example is the Syfe Core range of portfolios. Our Core portfolios are designed to focus on generating consistent risk-adjusted total returns for clients. Dividends form a very small percentage of total returns and thus the impact of dividend withholding tax is quite minimal. For investors seeking dividend income, they would be better served with dividend stocks or REITs from the Singapore market where dividends are tax exempt.

FX charges

Just as securities listed on our Singapore Exchange are denominated in SGD, securities listed on foreign exchanges will be denominated in foreign currencies. For Singapore investors who buy US-listed ETFs and other securities, there will be a foreign currency charge for converting SGD to USD.

This applies even if you buy a SGD-hedged unit trust, in which case the currency conversion is indirectly incurred when the fund manager buys a foreign stock. To buy Apple stock for example, the fund will still need to exchange SGD for USD. This FX fee is not accounted for in the expense ratio and is typically not transparently stated upfront.

Generally, retail investors pay between 0.50% to 0.70% in FX fees when they buy ETFs through their broker. Syfe customers pay much less – just 0.09% in FX fees – to access US ETFs.

Currency conversion charges however, should not be a reason to avoid investing outside of Singapore. In the long run, the performance of a globally diversified portfolio tends to outweigh any currency impact.

Hedging costs

One often overlooked downside of SGD-hedged unit trusts is the cost of hedging your currency exposure. Research has shown that active funds which hedge currency exposure incur significant hedging costs. On average, this hedging cost is 0.42% per annum and can result in long-term substantial underperformance when compared to unhedged share classes.

While there could be some cases where SGD-hedged share classes result in reduced FX volatility for income-oriented investors, investors with such needs might be better off taking direct exposure to locally listed and SGD denominated products such as REITs.

Why ETFs are better than unit trusts

For Singapore investors, we find that ETFs are a more cost-effective and efficient investment vehicle. One ETF typically holds shares in hundreds (and sometimes thousands) of listed companies; an ETF can cover a broad range of markets, sectors, styles, geographies, and assets.

It’s true that unit trusts can offer similar diversification benefits, but why pay an arm and a leg for them? When fees are the most proven predictor of future fund returns, it makes sense to minimize them.

Here’s the same table we showed earlier in the article. Notice how despite the comparable exposures, there is a significant return differential of 4%, which can be traced to the higher costs carried by unit trusts.

The expense ratios for funds assumes them to be index funds. Active mutual funds can have expense ratios 2 – 3 times the expense ratio indicated above

*Transaction and hedging costs are estimated to be 0.5% on average based on Lumint data.

**Mutual fund bid-offer spread estimated to be approximately 0.10% based on data from National Bank Financial

^Dividend withholding tax taken as 30% for US ETFs and 15% for Irish domiciled UCIT ETF/funds. Syfe’s Equity100 dividend yield is 1.25% compared to ~1.85% estimated for a comparable 100% equity portfolio using funds

^^Syfe’s FX conversion fee is 0.09%. Funds may pay higher FX costs through banks

At Syfe, we believe in low fees. That’s why we use ETFs in our portfolios and charge all-in management fees of 0.35% to 0.65% per year. And by the way, this includes all brokerage costs, portfolio rebalancing, and dividend reinvestment costs.

Disclaimer

This article is not intended to be financial advice, or a recommendation for any investment or investment strategy. The information is prepared for general information only, and as such, the specific needs, investment objectives or financial situation of any particular individual have not been taken into consideration. Syfe makes no warranty as to the accuracy of completeness of this article and accepts no responsibility for its content. Please note the value of investments can go down as well as up, and you may not get back all the money that you invest. Past performance is no guarantee of future results.

You must be logged in to post a comment.