Thought Of The Week

U.S September Inflation, Fed Meeting Minutes, Earnings Season

U.S consumer price inflation was largely in line with expectations. The headline inflation rose by 5.4% on an annual basis while the core CPI, which excludes the more volatile categories of food and energy costs, rose 4%. The stretch of higher inflation which many economists now expect to linger, is weighing on policy decisions at the Federal Reserve. In minutes released on Wednesday, the Fed officials were concerned that the disrupted supply chains were raising the risks of more persistent inflation as they firmed up plans to conclude their bond-buying stimulus program by the middle of next year. Higher consumer spending, shortage of workers and rising energy prices are keeping inflation higher for longer and this may prompt the Federal Reserve to act “earlier and swifter” to alter monetary policy to head off inflation.

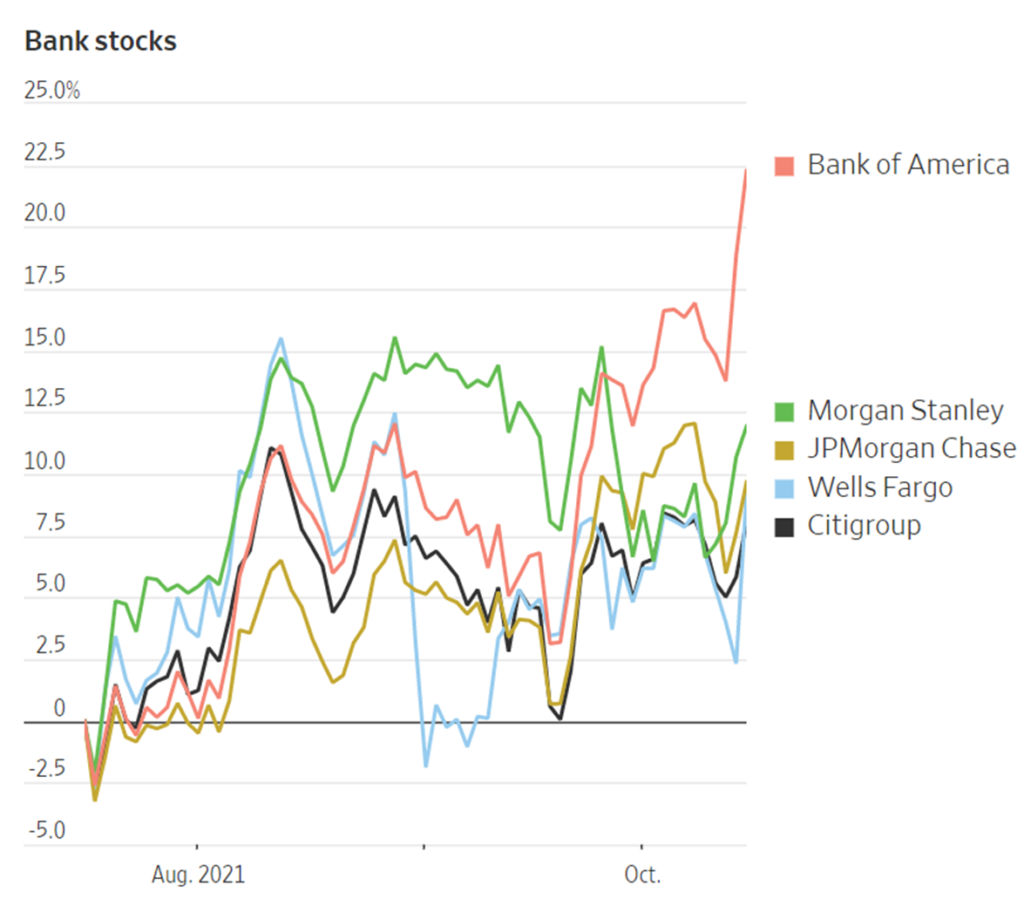

Meanwhile, U.S big banks kicked off the third quarter earnings season which all of them reported double-digit profit gains. Bank profits soared in the latest quarter largely due to a boom in mergers and acquisitions, higher equities trading volumes, as well as releasing the money that was socked away to prepare for a wave of loan defaults during the pandemic. The robust results helped to turn stocks higher which began the week with losses.

Singapore Tightens Policy in 3 years

The Monetary of Singapore (MAS) unexpectedly tightened its monetary policy during its semi-annual review on Thursday. The move came amid mounting cost pressures due to supply constraints which the central bank believes that this will ensure price stability over the medium term. Unlike most countries that use interest rate as its main policy tool, Singapore uses the Nominal Effective Exchange Rate (NEER), which is the exchange rate of SGD against a trade-weighted basket of currencies, since the economy is highly dependent on trade. By raising the slope of the NEER band while keeping the width and midpoint unchanged, MAS is effectively allowing the SGD to appreciate and allow imports to become cheaper and exports to become more expensive.

This slight tightening marks the start of a new growth cycle and is expected to moderate inflation, like many other central banks across the world. SGD appreciated against USD on the news, which may be short-lived if the U.S central bank tightens its monetary policy to address accelerating inflation as well.

Chart Of The Week

Important Information and Disclosure

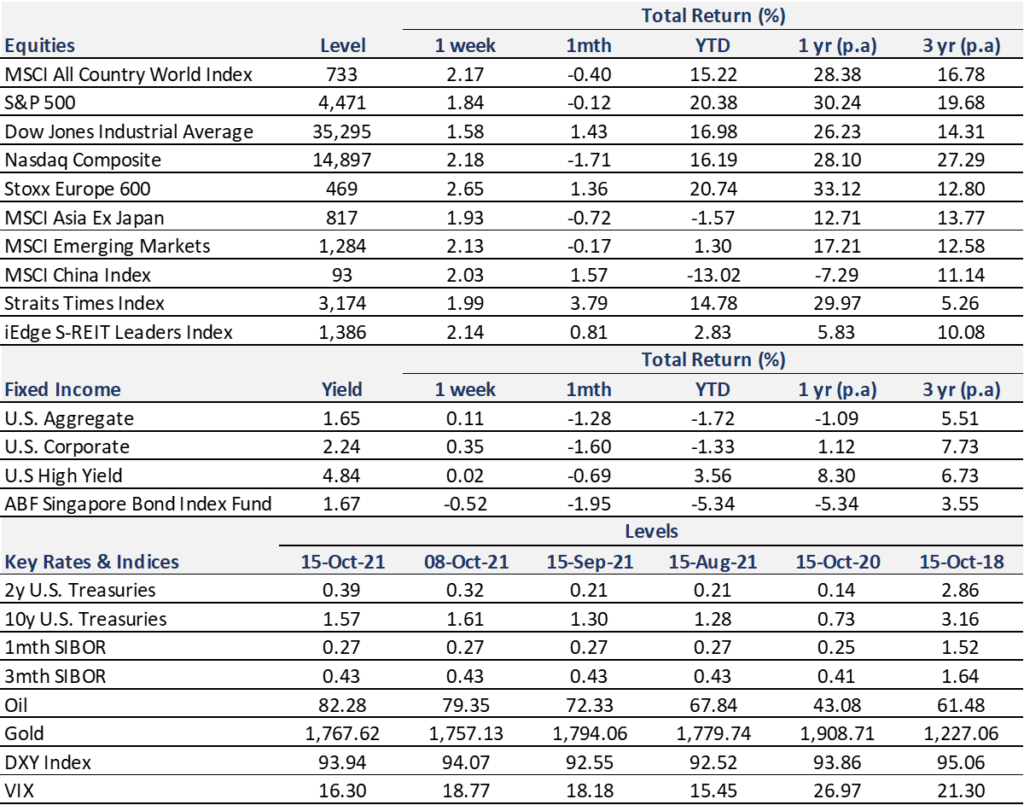

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.