Thought Of The Week

U.S Earnings Season, Higher Inflation Expectations

Major U.S indices notched their third weekly gains helped by ongoing recovery from the health crisis and strong corporate earnings results. Although market volatility has edged lower in recent sessions with VIX closed at 15.01 on Thursday, its lowest close since February 2020, there were big moves beneath the surface. While some companies were able to insulate themselves from the global supply-chain crisis and deliver strong results by passing down higher prices to consumers, other companies such as Intel struggled with parts shortage and China’s gaming crackdown, causing its shares to drop more than 10% after earnings. Other technology shares also slipped along with Snap after the social-media company blamed Apple for the changes to its privacy rules that would hurt its ad business. Snap’s stock tumbled more than 25%, highlighting the impact of Apple’s new policy on digital advertising.

Meanwhile, Federal Reserve Chair Jerome Powell stuck to the same script during a virtual panel discussion on Friday before entering a media blackout period ahead of the FOMC’s upcoming meeting scheduled on November 2-3. The central bank is expected to announce tapering considering persistently high inflation. The 10y breakeven-rate, a key measure of investors’ inflation expectation, has also notably increased to 2.64% from 2.31% in September although it should not pose any serious concern about longer-term inflation.

Stocks in Asia also rose after China Evergrande Group avoided default with a last-minute payment to its international bondholders, easing concerns about a contagion from the property developer’s woes. This will buy some time for asset sales until Oct 29, the end of the 30-day grace period for a next dollar coupon payment.

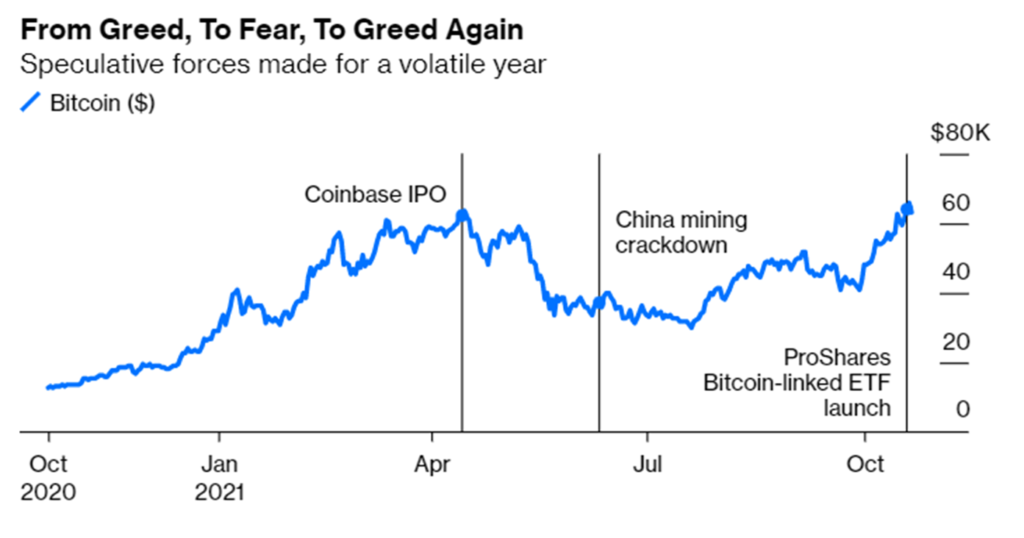

First Bitcoin-Linked ETF and What It Means

The first Bitcoin-linked ETF, ProShares Bitcoin Strategy ETF (BITO), debuted on Tuesday, making the most widely traded cryptocurrency even more accessible to investors with regular brokerage account. However, the ETF will not hold actual Bitcoins and will primarily invest in Bitcoin futures which are traded separately on regulated U.S exchanges such as Chicago Mercantile Exchange (CME). Regulators prefer futures-based ETFs due to a lack in jurisdiction over crypto trading venues that are not registered as exchanges in the U.S, which may leave investors vulnerable to fraud and manipulation since regulators will have any insight to the sources.

While some crypto enthusiasts complain that futures-based ETFs will not track bitcoin perfectly because of the costs of buying and selling futures contracts, others are contending that the launch of a bitcoin ETF would increase the cryptocurrency’s legitimacy and make it easier for institutional investors to get exposure. Other asset managers that quickly followed suit include Valkyrie Investments, which launched Bitcoin Strategy ETF on Friday and VanEck, which is slated to start next week.

Chart Of The Week

Important Information and Disclosure

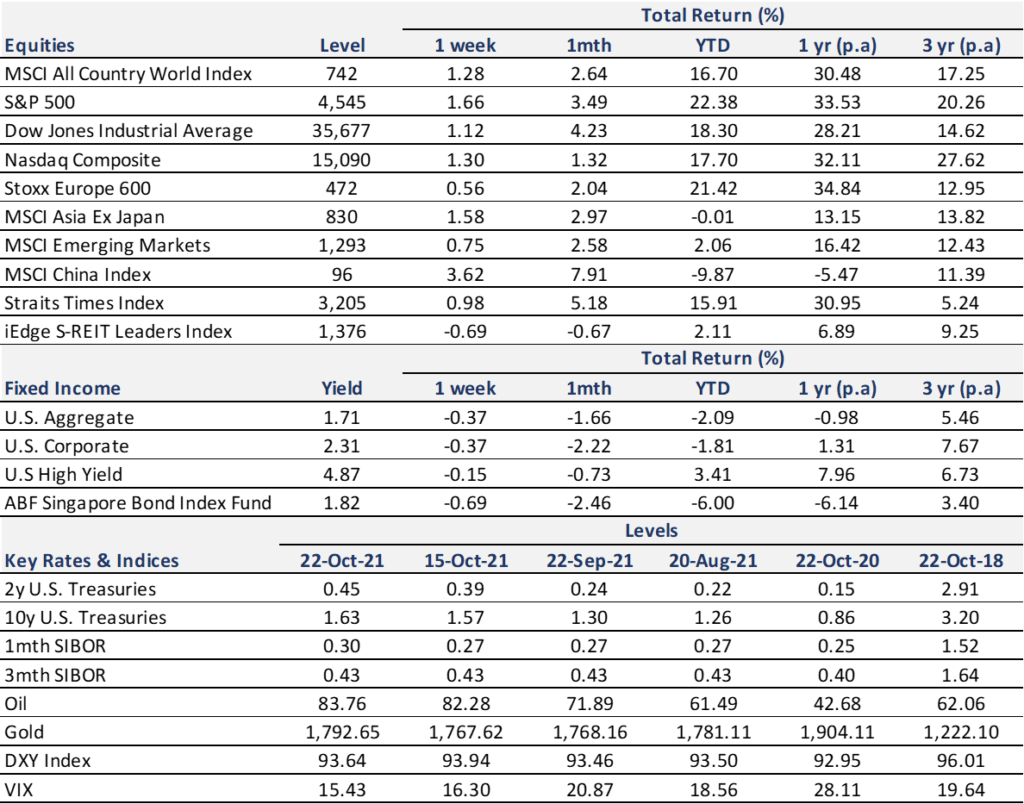

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total

return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.