Singapore REITs (S-REITs) have come under pressure in recent months due to tighter COVID-19 restrictions and the expectations of an early rise in interest rates.

Although falling prices are disappointing, they can be an opportunity for long-term investors to accumulate S-REITs at a bargain. Despite near-term challenges, S-REITs will likely remain resilient in the medium to long term given their robust fundamentals and growth outlook.

Here’s why.

Explaining the volatility

In May, Singapore entered Phase 2 (Heightened Alert) to curb the spread of the coronavirus. As the situation improved, so did investor sentiment. S-REITs enjoyed a short rally before growing COVID-19 clusters in July and August once again put us back into tightened safe management measures.

The retail, office and hospitality REIT subsectors were most affected by these stricter measures.

In September, another headwind for S-REITs came in the form of interest rate uncertainty. Since the US Federal Open Market Committee (FOMC) confirmed plans to taper its bond buying by the end of this year, the US Treasury yield has been rising, suggesting higher interest rates on the horizon.

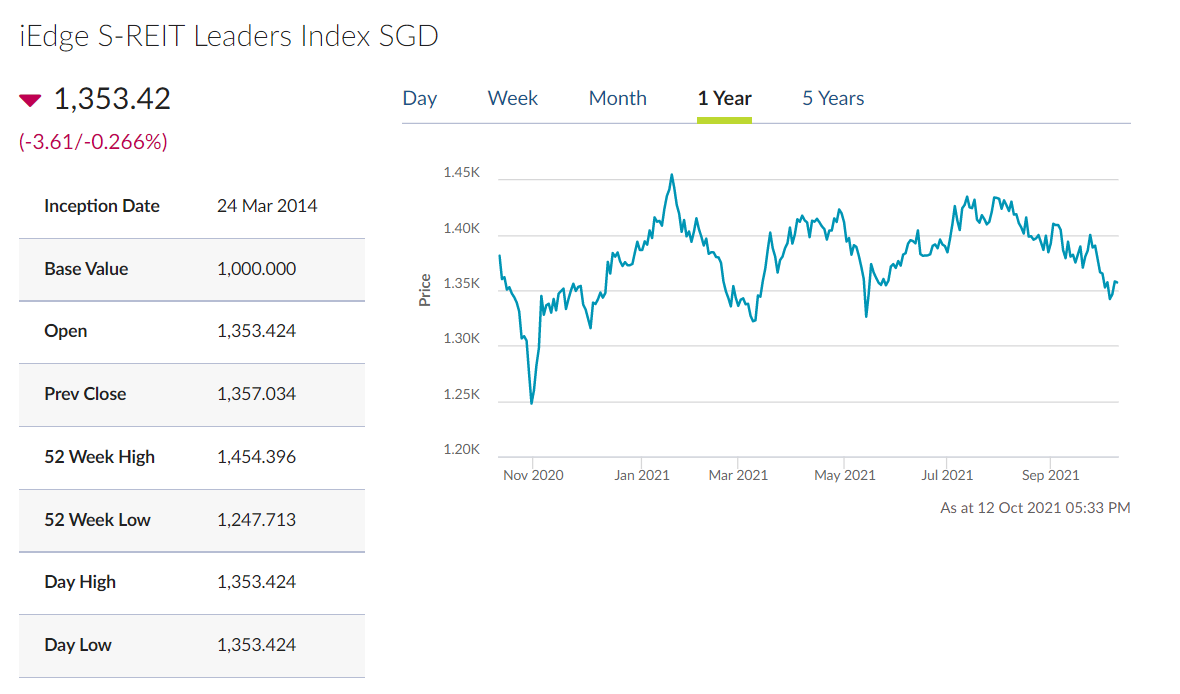

Rising rates tend to be a negative catalyst for REITs. The rate hike scenario has seen global REITs dip about 2%. In line with global REIT markets, the iEdge S-REIT Leaders Index ended the third quarter of 2021 down 1.4%.

S-REITs are still an attractive investment

Despite these pullbacks, S-REITs are a fundamentally resilient asset class in land scarce Singapore. This can be seen in how the Singapore REIT market rebounded following the March and November 2020 declines.

Although interest rates will eventually rise as the global economic recovery stabilises, current interest rates remain low (the 10-year Singapore government bond yield stands at 1.7% at this time of writing). With an average dividend yield of 5%, S-REITs are still the more attractive income option.

Bright spots for retail REITs

Restrictions on dine-in, social gatherings and a return to work-from-home have largely dampened the recovery of retail REITs, which were expected to outperform this year.

That said, S-REITs with exposure to suburban malls have demonstrated resilience as Singaporeans flocked to neighbourhood malls for essential services like food and groceries. The impact of the current restrictions was also less severe compared to last year’s circuit breaker. Most retail and food and beverage outlets remained open. Fitness classes were offered in some capacity.

Singapore now has one of the highest COVID-19 vaccination rates globally, with over 80% of the population fully vaccinated. As we push ahead to treat the coronavirus as endemic, our high vaccination rates coupled with our vaccine booster programme should pave the way for a progressive full reopening.

In the months ahead, shopper footfall is likely to rebound from the return of social activities. Downtown malls will likely benefit from vaccinated travel lane (VTL) arrangements too as tourists return.

Industrial REITs to remain resilient

Industrial and data centre REITs have largely held up well despite the tighter COVID-19 rules implemented in July and August. However, they too, were affected by the threat of rising interest rates after the conclusion of the September FOMC meeting.

That said, industrial REITs are likely to remain one of more resilient and sheltered REIT sectors in Singapore. For one, they tend not to be affected by social distancing restrictions. The accelerated growth of e-commerce, cloud computing, and digitalisation has also boosted demand for logistics facilities and data centres. These structural trends are here to stay, especially as some form of hybrid work becomes the norm.

What’s more, industrial REITs have completed more than S$6 billion worth of acquisitions this year. This includes Ascendas REIT’s acquisition of 11 data centre properties in Europe and ARA Logos’ acquisition of five logistics properties in Australia. We expect industrial REITs to continue pursuing acquisitions, which should spur more distribution per unit (DPU) growth in 2022 and beyond.

Near-term challenges for office and hospitality REITs

The default work-from-home directive is slated to end on October 24. That said, partial WFH arrangements are poised to be the new normal. In the short term, this is likely to affect demand for commercial office space.

That said, the long-term outlook for office REITs remains positive. Singapore is still one of the top cities for multinational companies and tech giants looking for regional headquarters. The relatively small homes in our city state also mean that there will always be a need for offices.

Hospitality REITs may face a longer road to recovery. Although Singapore has expanded its VTL arrangements, mass leisure travel is likely to only return in 2022. This is in line with the Singapore Tourism Board’s assessment that international visitor arrivals could take three to five years to return to 2019 pre-COVID levels.

To diversify their portfolios from traditional hotels, some hospitality REITs have pivoted to longer-stay accommodation assets this year. For instance, Ascott Residence Trust has acquired rental housing and student accommodation properties while CDL Hospitality Trust has revised its principal investment strategy to include similar long-lease assets. This should help enhance income stability and portfolio resiliency over the next few years.

REITs and rising rates

In recent days, concerns around a rate hike scenario appear to have eased, judging by the slight uptick in REIT unit prices.

Generally, higher long-term interest rates tend to compress the present value of dividends. This reduces the attractiveness of dividend-producing stocks and REITs, and we usually see a fall in valuations of these assets.

However, these concerns seem overblown. Firstly, rising interest rates are not necessarily bad. They signify that the economy is getting stronger, which means we should see rising occupancy rates as more businesses expand or are set up. This could lead to faster rental growth, which bodes well for REITs.

Although higher rates typically increase the cost of borrowing, most S-REITs are moderately leveraged since they need to comply with the 50% gearing limit imposed by the Monetary Authority of Singapore (MAS). With their healthy balance sheets, they are less likely to be affected by higher interest costs.

During the last interest rate hike in 2016 to 2018, most S-REITs were able to keep their interest costs relatively stable as well. Given that S-REITs have since scaled up due to industry consolidation and acquisitions, they are in an even better position to obtain competitive interest rates from their banks and minimise the impact from refinancing.

A diversified REIT portfolio is still best

In the weeks ahead, there will be further updates on the COVID-19 situation in Singapore, as well as economic and earnings data.

The current share price weakness offers long-term investors the opportunity to accumulate quality S-REITs that can capitalise on our eventual reopening. One way to do so is through Syfe REIT+, which holds 20 of the largest REITs in Singapore.

Here’s a sense of how well-diversified the portfolio is.

Retail: CapitaLand Integrated Commercial Trust (CICT), Frasers Centrepoint Trust (FCT), Lendlease Global Commercial REIT (LREIT)

Industrial: Ascendas REIT (AREIT), Mapletree Logistics Trust (MLT), Keppel DC REIT (KDCREIT)

Office: Mapletree Commercial Trust (MCT), Suntec REIT (SUN), Keppel REIT (KREIT)

Hospitality: Ascott Residence Trust (ART), CDL Hospitality Trust (CDREIT)

Healthcare: Parkway Life REIT (PREIT)

With a diversified portfolio, poor performance from a single REIT subsector will have a much smaller impact on your overall portfolio returns. You also avoid the risk of being overexposed to any one REIT.

Syfe REIT+ has an estimated dividend yield of 5.1% in 2021. If you’re keen to accumulate more REITs at the current attractive prices, consider a dollar cost averaging (DCA) strategy. For instance, you can choose to invest $1,000 into your Syfe REIT+ portfolio every month. This allows you to buy more at lower prices during market dips, while avoiding the risk of deploying all your cash should the market drop further.

You must be logged in to post a comment.