The Week Ahead

- China Industrial Production (Feb)

- U.S Retail Sales (Feb)

- FOMC Meeting

Thought Of The Week

Stimulus Bill Passed, Inflationary Pressure Eased

After two months since his American Rescue Plan was first unveiled, President Joe Biden finally managed to sign the $1.9 trillion pandemic-relief bill into law, marking his first major legislative achievement and allowing aid to flow to households, businesses, state and local governments.

The new bill includes $1,400 direct payments to most Americans which will be disbursed within days and an extension of $300 per week supplemental unemployment benefits into September. Unlike the previous stimulus checks which bore former President Donald Trump’s name in the memo line, Biden does not believe that it is a “necessary step” since it is “about the American people getting relief” and hopes to expedite the payments process.

The fiscal package will allow Biden to turbocharge America’s economic recovery which will help to create momentum for his budding presidency as he turns to a longer-term recovery package targeted at infrastructure and climate measures that could cost trillions of dollars more.

Concerns of an overheating economy which caused elevated bond yields over the past 2 weeks eased after the latest tame consumer price readings. Although the surge in demand for manufactured goods has caused some price pressures, they are likely to ease as demand shifts back to services later this year where the spare capacity in services will limit the inflation increases. Risk assets found fresh momentum this week with all market indices in the positive territory.

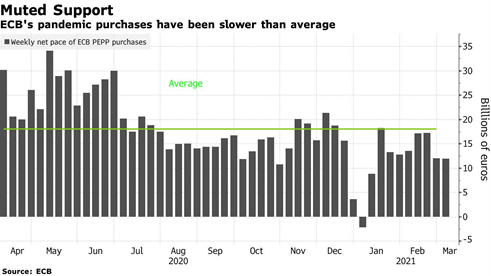

ECB Pledged to Accelerate Bond Buying

European Central Bank kept its monetary policy decision unchanged on Thursday but announced that bond purchases under the Pandemic Emergency Purchase Program (PEPP) would be “conducted at a significantly higher pace” in the next three months. This is to combat the recent spike in bond yields that would have posed a risk to the eurozone since those yields are often used as reference rates for bank loans to companies and households.

While the announcement provided some relief for the European bond market, investors remain sceptical on its commitment to maintain favourable financing conditions. In fact, ECB had bought fewer bonds through PEPP in recent weeks despite the sell-off in bond markets. Given that there were no targets on quantities or prices, the impact of a higher PEPP purchase pace remains vague as the pandemic-related restrictions the reasons limiting the economic growth instead borrowing costs.

Elon Musk Eyes Residential Energy

While Tesla is often seen as a synonym for electric vehicles, it has always been more than a car company with its official mission to “accelerate the world’s transition to sustainable energy”. Since 2015, Tesla has been expanding quietly into the residential energy, developing utility-scale batteries to store wind and solar energy when prices and demand are low, and selling back to the grid when prices are high.

This week, Tesla was reported to be plugging a 100-megawatt battery in Texas which will connect to the same electric grid that nearly collapsed due to the extreme weather conditions last month. It is estimated that a battery of the size could power up to 20,000 homes on a hot summer day. Although Tesla’s focus on energy is often overshadowed by its car business, analysts are estimating that Tesla Energy’s growth will be accelerating in coming years and may represent up to 30% of the company’s total revenue by the 2030s, up from roughly 6% today.

Chart Of The Week

Important Information and Disclosure

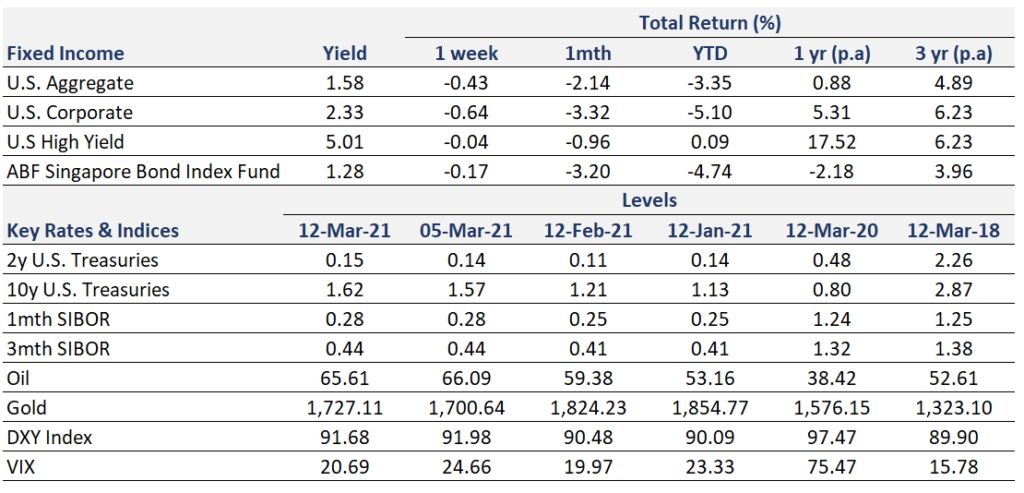

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.