Putin’s End Game

Russian and Ukrainian foreign ministers failed to make any progress on Thursday in Turkey. This marked the first in-person meeting since Putin invaded Ukraine two weeks ago. More than two million Ukrainains have fled since then. Russian attacks have turned even more brutal in recent days, with the bombing of a maternity hospital and attacks on civiilans using “humanitarian corridors” to escape.

After two weeks of fighting and facing far more resistance both in Ukraine and internationally than expected, Putin’s possible end game is looking a lot less clear. It is unlikely that we would see a regime change in Russia (despite what Twitterverse wishes for) or a swift cease-fire at this point. Things could get worse for Ukraine in the next stage of the war before a path to stability emerges.

China and 5.5% GDP Growth

CCP wrapped up its 13th National Committee last week where Xi emphasized ethnic unity, food security and economic stability. China has set its GDP growth target for 2022 at about 5.5%, lower than 7% from the previous decade but still an ambitious target for the world’s second largest economy. Premier Li Keqiang admitted that China faces headwinds as it tries to reach that target – listing problems such as climate change, income disparity and high levels of debt that are difficult to untangle even with monetary and fiscal policy support. Besides keeping monetary policy accommodative, PBoC will also transfer profits of 1trln RMB (approx 160bn USD) to the central government this year as a fiscal boost.

As we covered last week, Russia may lean on China more going forward and the RMB could stand to benefit in the short term as Russia is cut off from G3 and more.

Audit Checks for US-Listed Chinese Stocks Triggers Sell Off

Last Thursday (March 10, 2022), investors sold Chinese tech stocks as the SEC threatened delisting if several Chinese companies (BeiGene, Yum China, Zai Lab, ACM Research, and HUTCHMED Limited) do not provide adequate disclosure to allow a US accounting firm to conduct an audit. These five companies have till March 29 to respond and submit documentation.

If not Russian Oil, then what?

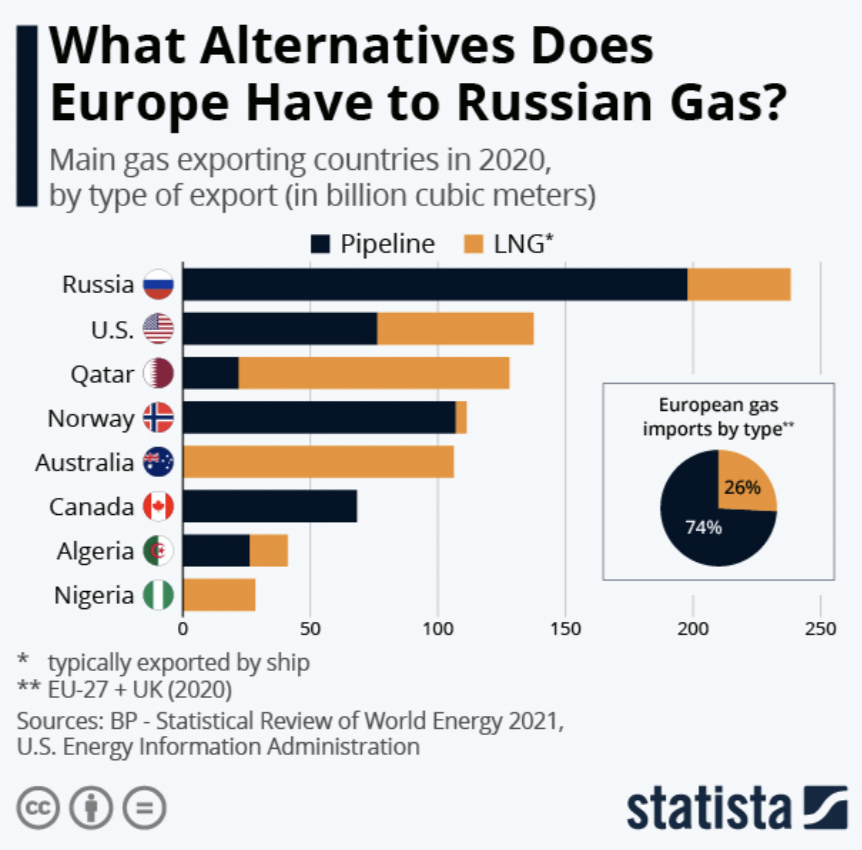

Russia is the top 3 energy producing countries in the world, after the US and Saudi Arabia. Last week, oil topped $139 per barrel (highest since GFC) before falling more than 10% on Wednesday. Earlier sanctions have left the energy sector out, but President Biden banned Russian oil and other energy imports last week. This move could push oil prices up further in the short term as US oil producers scramble to raise production levels while also looking for the missing barrels elsewhere – potentially Iran and Venezuela.

Additionally, the US economy is much less energy intensive than it was 20 years ago and food and energy spending makes up 12% of total consumer spending today.

While the US has some alternatives to Russian energy, the story is quite different for Europe. The alternative solutions for Europe are either insufficient or too difficult logistically to achieve in the short term. Even if willing OPEC+ members (ex- Russia) manage to reach maximum capacity, there will still be a shortfall.

Inflation at Almost 8%

US CPI rose 7.9% through February, the fastest pace in 40 years. This report caught the start of higher gas prices due to Russia’s invasion of Ukraine and for the next few months, we may expect to see effects of higher energy costs percolate. 2021 GDP growth rate hit a 37 year high at 5.6%. Strong consumer spending, nonresidential fixed investment, export growth and strong inventory investment generated the majority of the growth last year.

Earnings Highlights

We covered key market moves here.

What’s Ahead

Jerome Powell, the Federal Reserve chair, told congress that he would support a quarter percent hike at the FOMC meeting on March 15-16. Markets are expecting the first hike to be delivered next week, the start of at least expected four rate hikes this year.

Pinduoduo, Futu, AngloGold, FedEx, and Gamestop are set to report earnings next week.

Where could markets go from here?

Wars cause tremendous humanitarian cost. Historically, geopolitical conflict tends to have a relatively short-lived effect on markets. However, war on the border of Europe is unprecedented. Investors can take this moment to check that portfolios have sufficient diversification: across asset classes, sectors and countries. Exposure to commodities as a shorter term hedge could be useful too.

So far, the rise in commodity prices and potential supply shocks as a response to the war have ignited fears of stagflation, which last happened more than 40 years ago in a vastly different world. So far, these albeit alarming increases in commodity prices are insufficient to derail global economic and earnings growth completely given the health of the global economy, strong corporate balance sheets, robust momentum from the recent jobs report, along with the re-opening momentum post-Omicron.

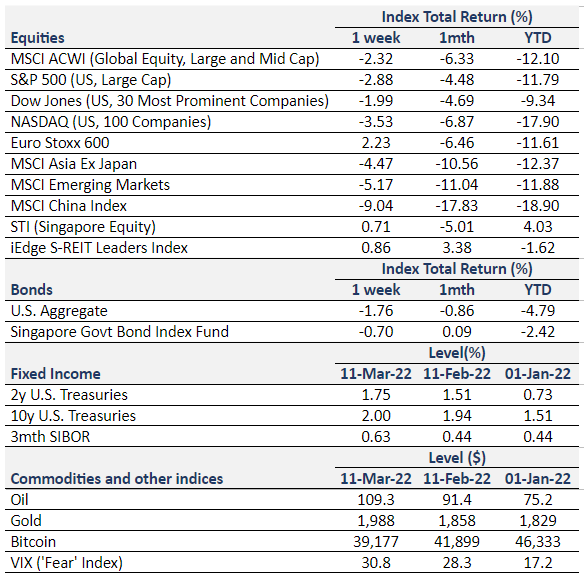

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Euro Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. U.S. Aggregate and SBIF from Bloomberg.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. Bitcoin/USD, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.