Putin and the Rest of the World

Russian forces press ahead in Ukraine, meeting more resistance than expected but managing to control vital sites like ports. Investors were rattled as Europe’s largest nuclear plant was attacked and occupied on Friday. So far, international monitors said that there was no sign that radiation had leaked.

The United States, Europe and their allies have deployed the most effective non-military weapon they have. Russian assets held by their financial systems were frozen and Russia was cut off from SWIFT (the messaging system that enables international payments). Many businesses (Exxon, McKinsey, and Apple to name a few) are pulling out of Russia.

A week after the invasion, the Russian ruble has fallen to a record low despite the central bank’s efforts to support it by raising interest rates to 20%. Despite Russia’s attempt to sanction-proof itself over the last few years and leaning more on China, Putin’s war may end up crippling Russia’s economy and financial system.

China and Russia

China is now one of Russia’s most important trading partners. Financially, China has been an ally too, looking at direct Chinese lending (to Russian companies) volumes that peaked the last time Russia annexed Crimea in 2014. China and Russia have been working on an alternative to SWIFT but it will take some time for it to be fully operational. On the political front, Chinese officials have also stated that China is against the kind of sanctions Russia is facing currently.

As the world moves away from doing business with Russia and even buying Russian oil (that is 15% cheaper as oil surges past $110bbl), China is in a position to emerge stronger. Russian oil that used to go to Europe could go to China at a discount. As Putin moves away from the dollar and Euro, this leaves a gap for the Chinese renminbi to be currency of trade in the region.

Impact on Commodities Going Beyond Oil

Russia is the top 3 energy producing countries in the world, after the US and Saudi Arabia. Russia and Ukraine are key grain producers too, contributing almost a third of the world’s traded wheat. When it comes to metals, Russia is the second largest exporter of aluminum and the largest producer of palladium, which is used in catalytic converters.

So far, the rise in commodity prices as a response to the war would be insufficient to derail global economic and earnings growth completely given the health of the global economy, strong corporate balance sheets, along with the re-opening momentum post-Omicron. The US economy is much less energy intensive than it was 20 years ago and food and energy spending makes up 12% of total consumer spending today.

Where could markets go from here?

Historically, despite the high humanitarian cost, geopolitical events tend to have a relatively short-lived effect on markets. However, war on the border of Europe is unprecedented. Investors can take this moment to check that portfolios have sufficient diversification: across asset classes, sectors and countries. Exposure to commodities as a shorter term hedge could be useful too. Looking out further, the market impact of this conflict may fade over time, and the markets may focus on rising interest rates.

Powell’s Speech to Congress Sets the Stage for March Hike

Jerome Powell, the Federal Reserve chair, told congress that he would support a quarter percent hike at the FOMC meeting this month, underlining his intent to “avoid adding uncertainty to what is already an extraordinarily challenging and uncertain moment.”. Weighing high inflation, a strong labor market and normalization against Russia’s invasion and its impact on the economy – Powell urged that flexibility would be crucial.

Strong Jobs Report

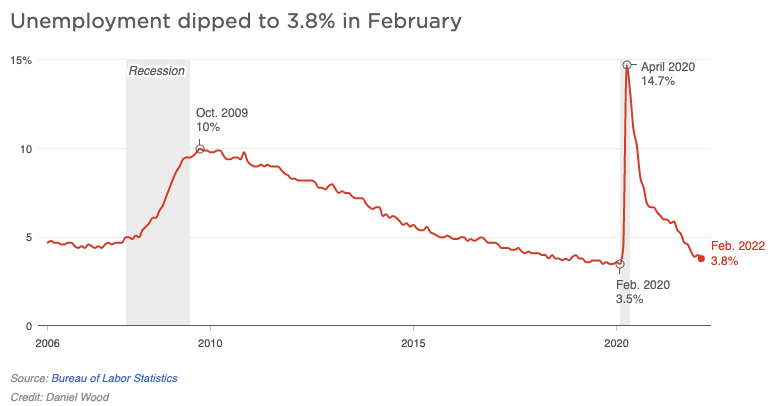

The US economy added 678k (200k more than expected) new payrolls in February and the unemployment rate fell to 3.8%. Taken together with the strong hiring in the last three months (amidst an Omicron wave), the labor market has demonstrated resilience. As compared to Feb 2020, the US economy has made up for more than 90% of jobs lost during the pandemic.

Jobs openings are near a record high and layoffs are few. Tight labor supply has pushed wages higher, even though wage growth in February was mostly flat. Job growth spread broadly across major industries, with leisure and hospitality making the most gains (179k out of 678k, or 26%).

This data release is unlikely to cause the Fed to deviate from its path. Charles Evans, president of the Federal Reserve Bank of Chicago, called it “good news – it doesn’t really change anything” that the Fed was prepositioning for.

Earnings Highlights

Profit and earnings growth will remain the key driver of returns. In the last week, top performers include value stocks like Target (TGT). Lucid (LCID) disappointed investors as it cut its production guidance for 2022. Lucid has shown that it may be able to build a better EV than Tesla but whether it can build more than 20,000 such vehicles remains uncertain.

A bit closer to home, Grab Holdings (GRAB) tumbled 37% on Thursday as its losses almost doubled to $-1.1bn in 2021 as compared to 2020. Almost 30% of that was related to public listing related expenses, which is non-recurring. Grab spent more this year to grow its pool of drivers and customer incentives to keep market share.

What’s Ahead

Here are companies we are watching next week:

JD.com (JD) like its closest Chinese peers Alibaba (BABA) was hit last year by regulatory headwinds, but showed greater resilience. We have also seen the titans of investing taking a closer look at Chinese stocks. Ray Dalio of Bridgewater and Charlie Munger of Berkshire Hathaway have increased their holdings in JD and BABA respectively.

As compared to Alibaba, JD.com is more like Amazon (AMZN) – allowing businesses to sell directly to consumers while handling the inventory and logistics without relying heavily on third party vendors. JD.com generates more revenue than Alibaba. The reasons for this are twofold: 1. The average value of goods sold on the platform is higher and 2. Given the structure of operations, JD.com is the first party in transactions with customers.

Oracle (ORCL), one the stalwarts and value-oriented names in the technology sector will announce earnings on March 10, 2022. Oracle has been down from its peak late last year due to the tech rout and due to its acquisition of Cerner for $28.3bn. This acquisition gives Oracle a way to digitize medical care as Cerner’s systems already run on the Oracle Database. Oracle has healthy operating profit margins – without accounting for non-recurring acquisition costs – in the 30-40%. As compared to peers, Oracle offers differentiated and industry-specific (HR, healthcare, customer relationship management (CRM), enterprise management) solutions that combine applications and infrastructure in the cloud.

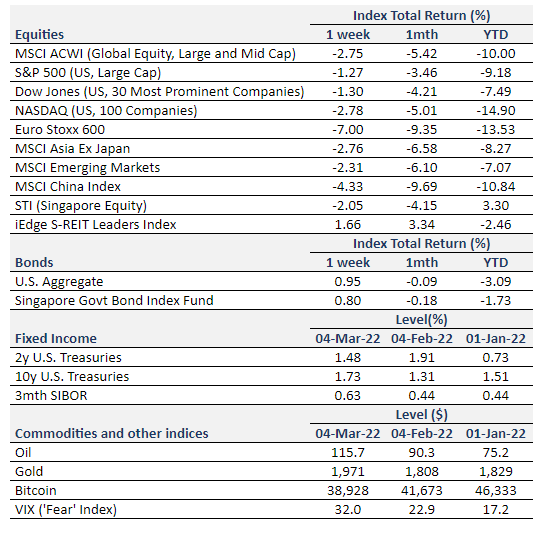

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Euro Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. U.S. Aggregate and SBIF from Bloomberg.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. Bitcoin/USD, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.