Brief Bear

S&P 500 has fallen for seven consecutive weeks and on Friday afternoon, briefly crossed the bear market threshold (a 20% fall from peak) before rallying and ending the trading session close to where it started. For the last few months, investors have been worried about inflation (how long will it go on for? Has it peaked?) and how aggressive the Fed should and will have to be in increasing interest rates to slow down the economy and rein in inflation. Too much and it might tip the economy into a recession while too little and too late will make it much harder (and possibly more painful on households) to tamp down inflation.

Stalwarts stalling

A possible catalyst for this week’s market turbulence is results from consumer staples such as Walmart and Target. For the first time in many years, Walmart reported a fall in quarterly profits – signalling that the largest retailer in the US and largest non-governmental employer in the world was having trouble passing rising costs to consumers without taking a meaningful hit in sales. This may be an inflection point as a few months ago (and before Russia’s invasion of Ukraine), companies like Starbucks and McDonalds were more confident that price increases will not impact sales significantly.

Target also revealed that as consumers shifted their spending patterns coming out of the pandemic, the store has been left holding on to an oversupply of items – kitchen appliances, televisions and lawn furniture (durable goods that did well in the last two years). Now, shoppers have switched from to different goods (apparel and travel related products and from goods to services. As we have written a few weeks ago, the leisure sector has provided optimistic forward guidance for the next quarter.

We covered market movers here.

Not all bad news..

Consumer sentiment and spending for services is still strong. According to the WSJ, looking at data from online-reservation platform, Resy – April was the busiest month on record. The busiest months tend to fall in the summer. The US economy is largely consumer driven – where consumption contributes to ⅔ of GDP. Whether US consumers will be able to sustain consumption patterns in light of higher prices and as fiscal support for Covid-19 fades will be a key indicator to watch.

The Treasury Department announced a record monthly budget surplus of 308bn USD in April. The Treasury department holds the purse strings for the nation, somewhat similar to the Ministry of Finance in Singapore. The US, like most nations that have poured tremendous fiscal resources to fight Covid-19, has accumulated a large budget deficit to fund support programs. The April surplus has helped chip away at that accumulated budget deficit. This bit of positive news went largely unnoticed by the market during the week. A smaller budget deficit (it might be too early to hope for a budget surplus at the moment) reduces the risk of a fiscal crisis and leaves greater leeway for expansionary fiscal policies during a recession if necessary.

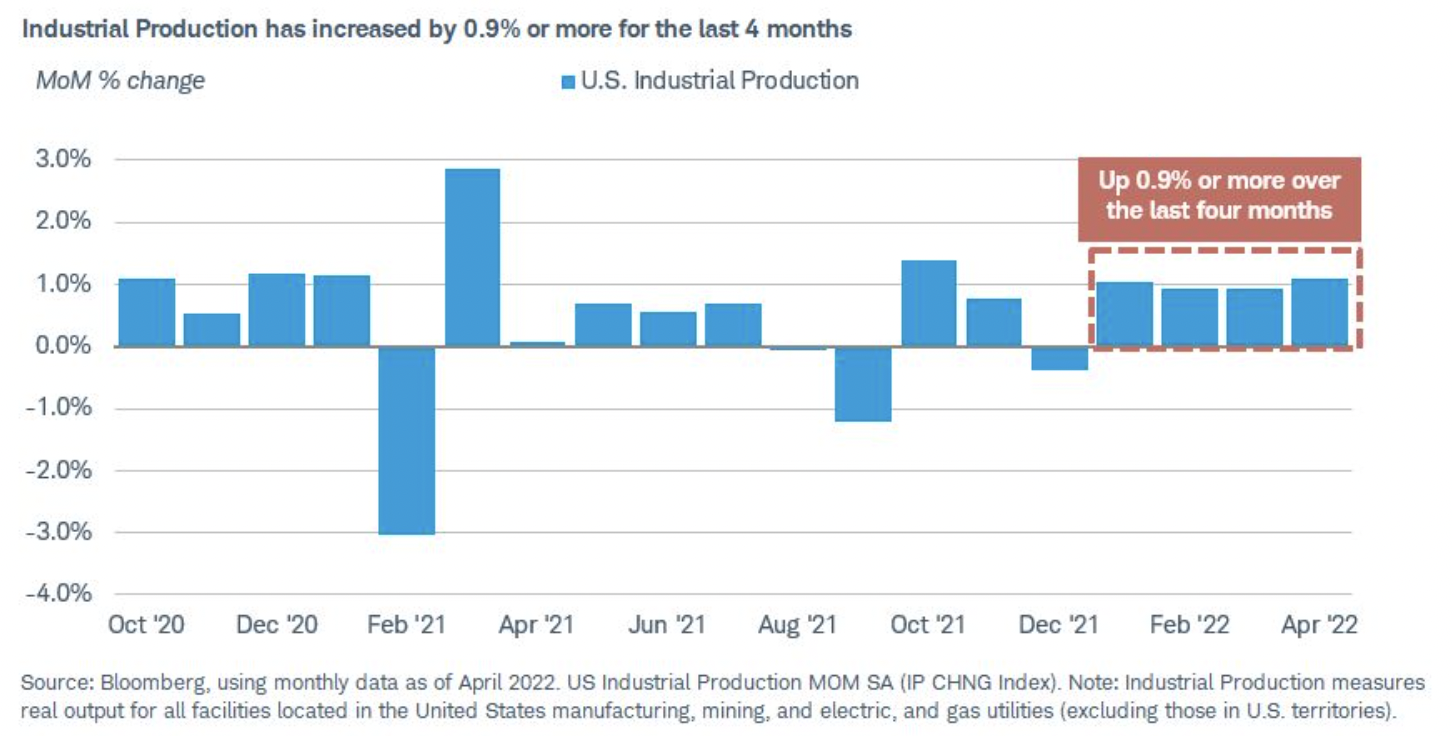

What are other indicators telling us?

The manufacturing industry is on the recovery, shrugging off labour and supply chain challenges. Intuitively, when labour and components are in short supply, we would not expect to see positive manufacturing indicators. However, we have seen industrial production and capacity utilisation surpass pre-pandemic levels, along with strong increases for new orders for the rest of the year.

Source: Schwab Center for Financial Research

Greater support for Chinese securities

Chinese shares were up more than 3% this week. China cut the five-year prime rate (the main mortgage interest rate) on Friday to 4.45% from 4.6%. This cut was largely expected as the economy slowed down due to lockdowns. However, the size of the reduction (15bps) came as a surprise as it is the largest reduction since the rate system was reformed in 2019. This move has been seen as one of the strongest signals of governmental support for the property sector in several years.

Chinese internet stocks were buoyed this week by two key events: Vice Premier Liu He’s appearance at the CPPCC (Chinese People’s Political Consultative Conference) meeting with internet companies and JP Morgan’s upgraded price targets and outlook for the sector. After labelling the sector “uninvestable” two months ago, the upgraded outlook from JPM came due to recent positive regulatory announcements and revisions to audit secrecy laws in order to avoid potential delistings. Both developments represented a positive shift that the regulatory super-cycle that triggered a selloff is tapering.

Where could markets go from here?

Risks to growth have increased lately but the worst case scenario has not materialised. Companies and households are entering this next stage of the economic cycle with good fundamentals and strong balance sheets (and wide profit margins vs. historical levels for many corporations).

While growth may be held back by persistent inflationary pressures in the short term, investors can take a diversified approach: seeking balance between value and growth, and US and international. During times of market volatility, it becomes even more important to pay greater attention to the things one can control: diversification, asset allocation and cost.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.