Not Yet But Maybe

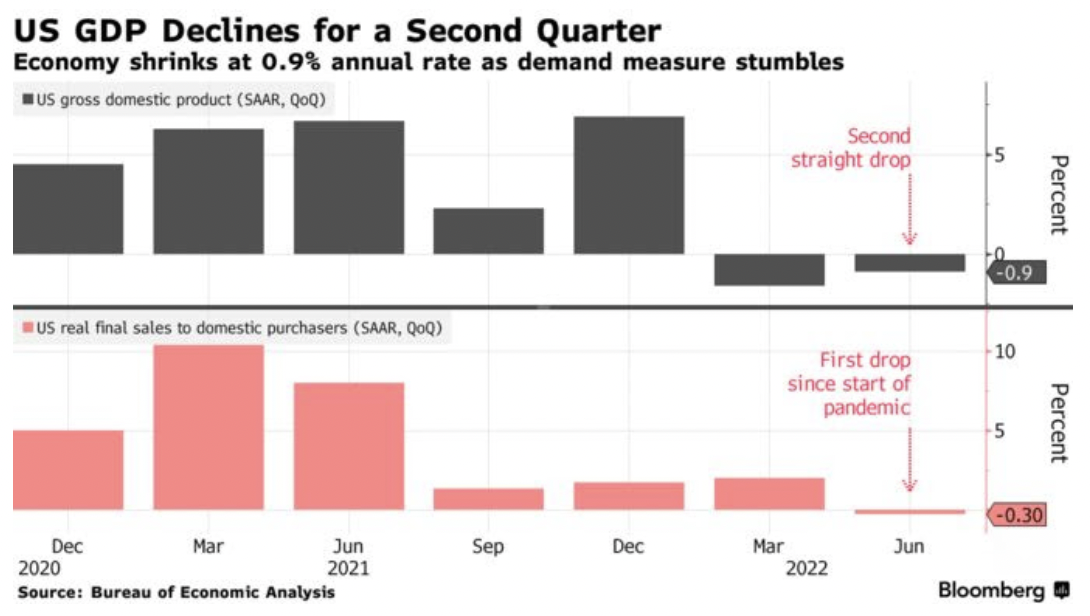

Inflationary concerns in the US have shifted towards recession recently as many accept that it could be the price to pay to bring inflation down. US GDP fell for the second consecutive quarter – the latest reading showed a 0.9% annualised contraction, following a decline of 1.6% (also annualised) in the first quarter of 2022.

Technically, a recession is often defined by two consecutive quarters of negative growth. But according to the National Bureau of Economic Research, the official arbiter of recessions in the US, the country has not entered a recession yet as the labour market remains strong – wages, prices and consumer spending all continue to rise.

More worryingly but unsurprisingly given the rise in prices, personal consumption (about ⅔ of US GDP) fell for the first time since the start of the pandemic. It is hard to see things turn around quickly, especially with a strong dollar. A rise in domestic demand through imports would actually count against GDP measures. A strong dollar could also hurt export competitiveness.

Another supersized move

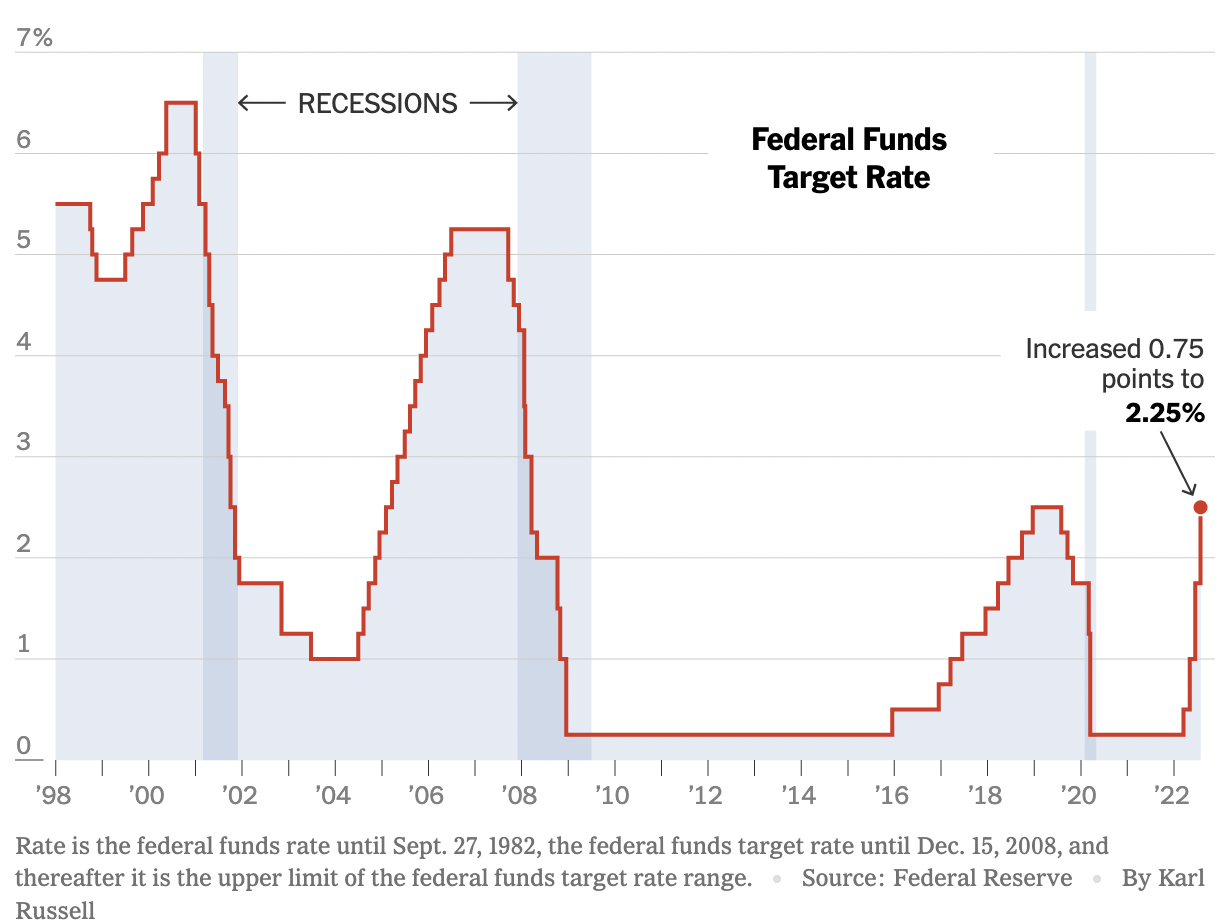

The Federal Reserve raised interest rates by 0.75% in the July FOMC meeting, a move that was regarded as the base case prior to the meeting. Committee members voted unanimously to make the same move as in June, pushing the federal funds rate up to 2.25-2.50%.

Chair Powell left large rate hikes on the table for subsequent meetings, yet major indices gained following the meeting.

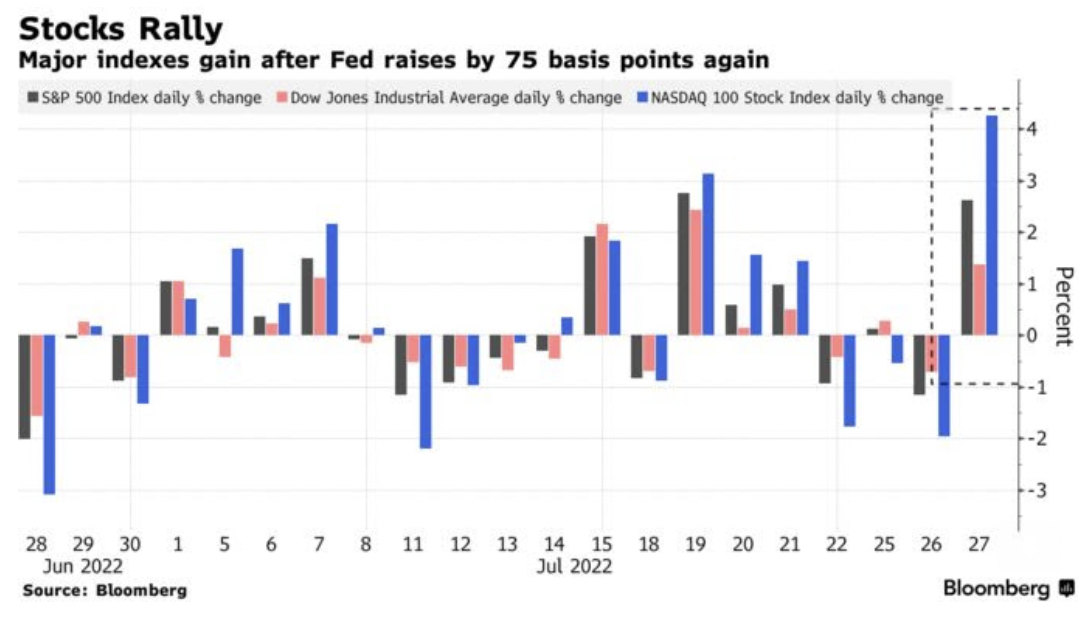

Relief rallies

The S&P 500 index is set for one of its best months – gaining 9% in the last month. 10-year bond yields fell to the lowest since April post GDP release, which showed a technical recession and US equities rallied on Friday on better than expected earnings from big tech – Apple and Amazon.

Regardless of whether we have peak inflation, global bonds are looking at their best monthly gain since 2020. Investors may be signalling that the Fed’s aggressive stance has reached a peak, to the extent that it is going to cause a recession.

Alibaba goes to Hong Kong?

Alibaba plans for a primary stock listing in HK at the end of the year, as the NY-listed company is facing the possibility of delisting due to audit rules. Alibaba would be following in the footsteps of several Chinese companies that have opted for dual-primary listing in the US and Hong Kong. Doing so gives companies access to mainland investors, bringing in billions of fresh money – while serving as twin engines for a plane.

Mainland funds and assets tend to be somewhat contrarian, buying the dip even as foreigners sell. For instance, Tencent has been the most purchased HK-listed stock despite the tech rout in the last eighteen months.

Chinese and US officials have yet to reach a concrete agreement over audit rules and necessary disclosures for companies under review to continue trading on the US exchanges.

Big week for tech earnings:

Recap on big tech here: Apple and Amazon stay strong, but Meta stumble.

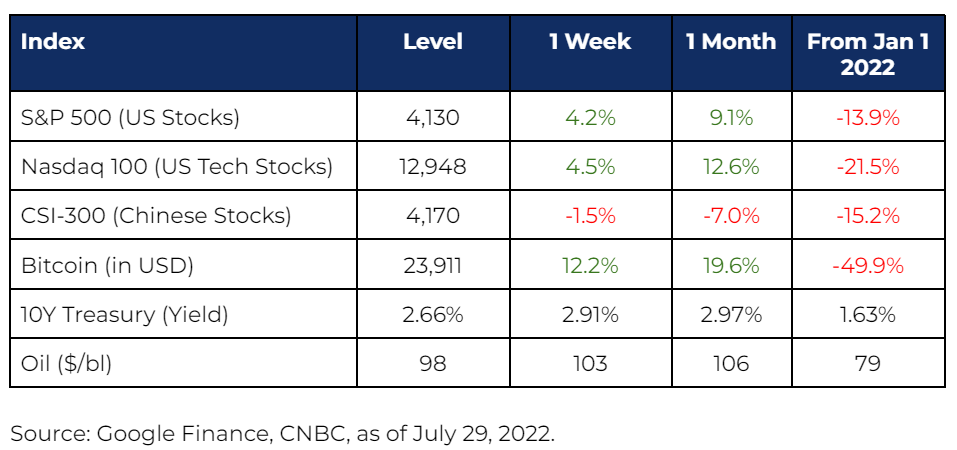

Market Stats

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.