We have seen better days

US Equity markets finished the first week of May in the red: S&P 500 and the Dow lost 0.2% over the week while the Nasdaq composite lost 1.5%. US stocks started the week on an optimistic note, recording three straight positive sessions before plunging on Thursday and Friday following the FOMC decision. Investors were nervous about the Fed’s ability to rein in inflation without tipping the economy into a recession.

What spooked the markets?

Russia’s invasion of Ukraine, inflation, stock market volatility, inflation, and rate hikes have all affected investor sentiment negatively. Markets are having a tough time reacting to the removal of support from the Fed, a policy path that has been discussed at length for much longer than last week. According to research from American Association of Individual Investors, the percentage of individual investors describing their six-month outlook for stocks as “bearish” surged to its highest level since 2009. Historically, the S&P 500 index has gone on to realize above-average and above-median returns during the six- and 12-month periods following unusually low readings for bullish sentiment and for the bull-bear spread. Unusually high bearish sentiment readings historically have also been followed by above-average and above-median six-month returns in the S&P 500.”

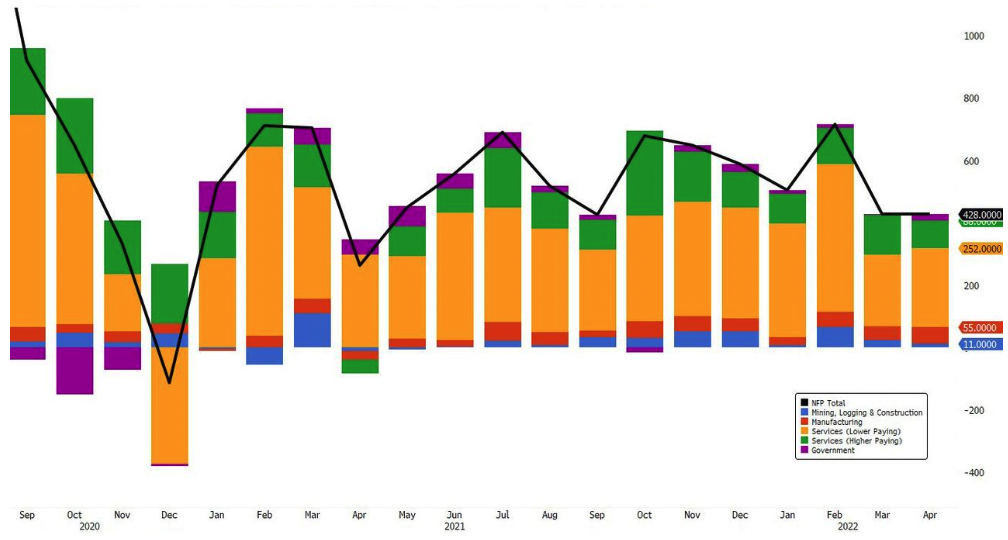

Jobs growth figures shows the US economy is still going strong

The latest NFP (non-farm payrolls) released every first friday of the month showed a gain of 428k jobs in April. This matches the figure we saw in March and similarly, gains have been broad-based , across industries but concentrated in the service sector. The unemployment rate remained at 3.6%, close to pre-pandemic levels. Prior to 2019, gains of around 200k would be regarded as a stellar jobs report.

Almost two job openings for each unemployed person

The US economy has made up for 95% of 22 million jobs lost during the height of the pandemic. However, labor supply has not caught up fully, there are now 1.9 job openings for each unemployed person seeking employment. Businesses have had a hard time finding workers as they try to meet demand for goods and services. This has led to strong wage growth for individuals – average hourly earnings at 5.5% higher than a year before but with inflation (measured by the Fed’s preferred indicator PCE: personal consumption expenditure) running at 6.6% for the same period, workers are not necessarily feeling that the good times are here.

Double Hike

Sustained price increases have not all been demand driven. Russia’s invasion of Ukraine and lockdowns in China have added to those price pressures. To stem inflation, the Federal Reserve raised its benchmark interest rate by 0.50%, a double hike, and the biggest increase in twenty years. Front-loading of rate hikes will (hopefully) slow down demand by increasing borrowing costs, before inflation gets even more difficult to control. Fed chair Jerome H. Powell stated that more double hikes would be “on the table”, but dismissed the idea that the committee is “actively considering” even larger hikes (0.75% and above).

Is this going to cause a recession?

Financial markets have been roiled by both the prospects of double hikes and what if the Fed is unable to get inflation under control. This may seem like a paradox, but the Fed is effectively trying to tap on the brakes to slow down the economy without tipping it into a painful recession. In the press conference after the May FOMC meeting, Powell states that “Everyone will be better off if [the Fed] can get this job done – the sooner the better”. However, the tools the Fed has access to, despite being very powerful, are actually quite blunt and imprecise. Powell acknowledged this in the press conference in response to a reporter; the Fed essentially has “ interest rates, the balance sheet, and forward guidance, and they’re famously blunt tools.”. The shift to higher rates may not be straightforward and the path there will be met with obstacles but the aim is to do it while achieving a prolonged expansion.

China: delisting list grows

Last week, the SEC expanded the list of entities facing possible delisting from US exchanges. The electric vehicle sector in China sold-off heavily as firms like Nio and XPeng were added to the list. At the same time, Reuters reported that officials from the US Public Company Accounting Oversight Board (PCAOB) have arrived in Beijing to attempt to settle the issue of audit reviews for US-listed Chinese companies and avoid delisting. This is a significant first step to untangling the audit requirements for US-listed firms.

Earnings spotlight

According to research from FactSet, out of the S&P 500 companies that have reported earnings so far for Q1 2022, the majority beat consensus EPS expectations. The blended year-on-year earnings growth for the index in the first quarter came in at 7.1%. Excluding Amazon, the S&P 500 would be clocking double digit earnings growth (10.1%) in Q1 2022.

We covered market movers here.

What’s Ahead

So far more than 85% of companies in the S&P 500 have reported Q1 2022 results. Out of those, according to research from Schwab, 79% have beat EPS estimates while 67% have beat revenue estimates.

Where could markets go from here?

Risks to growth have increased lately but the worst case scenario has not materialized. Companies and households are entering this next stage of the economic cycle with good fundamentals and strong balance sheets (and wide profit margins vs. historical levels for many corporations). Previously, we saw a divergence in expectations from bond and equity investors: where the former appears less optimistic but now after equity markets sold off, expectations are more aligned.

While growth may be held back by persistent inflationary pressures in the short term, investors can take a diversified approach: seeking balance between value and growth, and US and international. During times of market volatility, it becomes even more important to pay greater attention to the things one can control: diversification, asset allocation and cost.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.