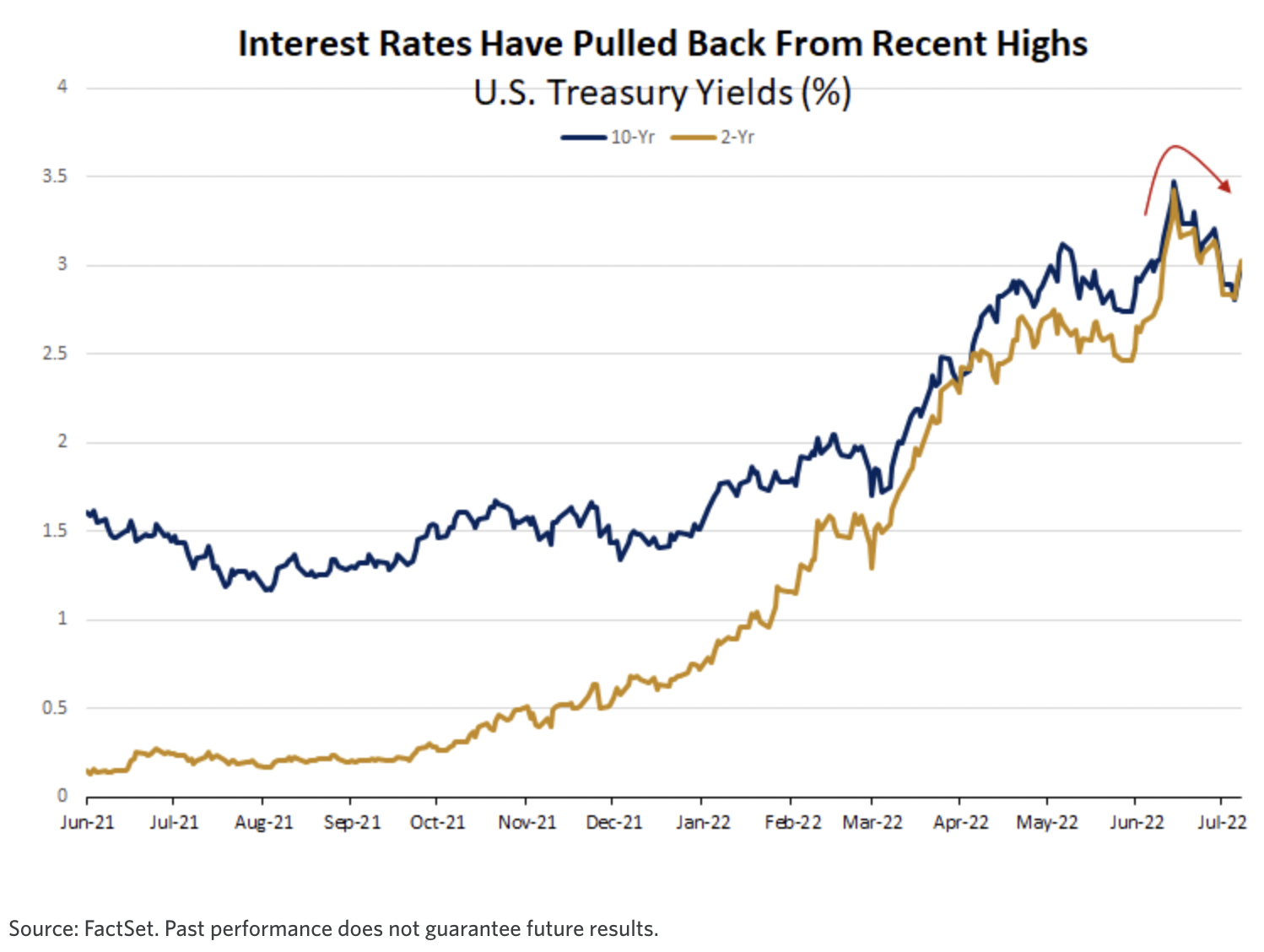

Recovery for stocks but re-inversion for bonds

US Stocks had a good week of recovery, led by tech-heavy Nasdaq, which is up 5%. Fears about a recession continue to push Treasury yields down and led to a re-inversion of the yield curve. As we wrote before when 2 year yields were briefly higher than 10 year yields earlier this year, yield curve inversions tend to precede recessions but there have been false positives.

Shorter and shallower recessions tend to happen when there are smaller increases in unemployment – this makes sense intuitively too. US recessions where the unemployment rate rose by 2.5% were the most mild, with US GDP falling less than 1.5%. Given the strength of the labour market and the state of household and corporate balance sheets, there is reason to believe that if a recession were to emerge, it could be a short and shallow one.

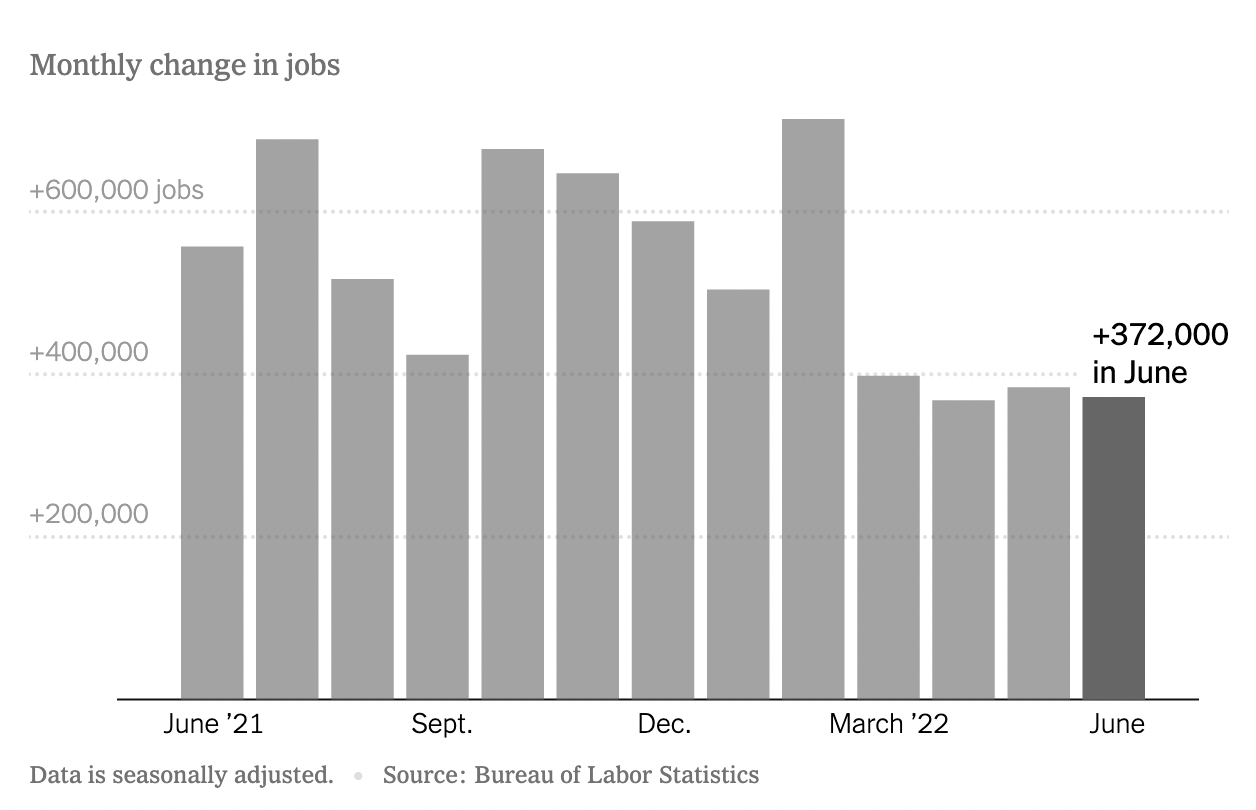

Strong labour market

The US economy added 372,000 jobs in June, in line with jobs added in the prior three months. The unemployment rate stayed at 3.6%. Job openings fell but there are still nearly two jobs for every person looking for work. However, the pressure to hire might be diminishing slightly as borrowing costs increase and expansion plans are put on hold or scaled down.

Wage growth continues

Wages grew at 5.1% in the 12 months ending in June, slightly lower than 5.3% in May. Wage inflation has not been the largest contributor to inflation as Chair Powell stipulated, but “going forward, they would be very important”. He makes the case that job growth will need to slow for the economy to be on a sustainable path for the long-term.

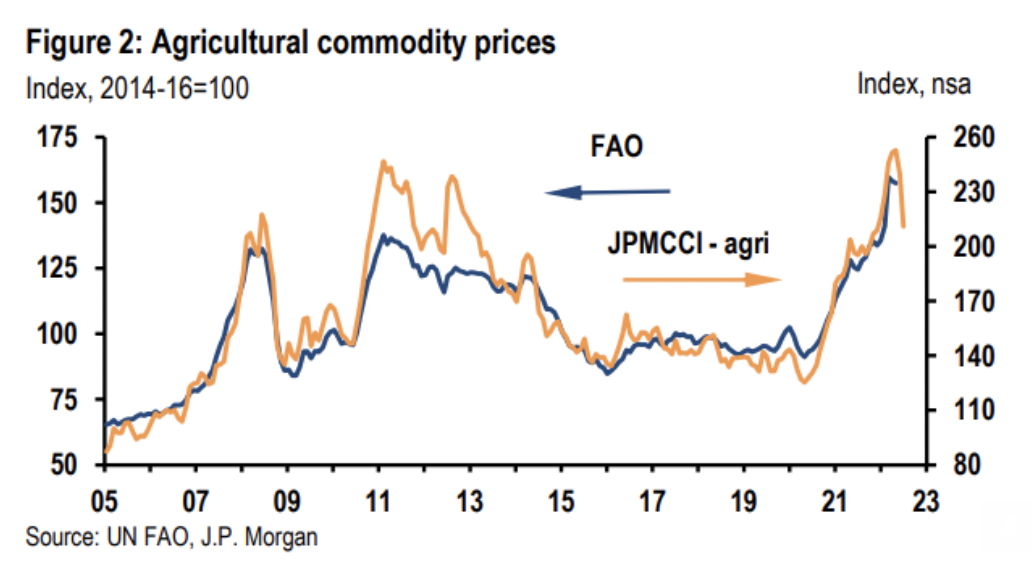

Food inflation wanes

Soaring food inflation due to the war in Ukraine shows some signs of waning. The United Nations (UN) Food and Agriculture Organisation’s food-price index dropped for a third straight month. The index of agricultural commodities, below, from JP Morgan, fell due to lower wheat prices. A sustained fall in supply side inflation could help reduce pressure on central banks to tighten monetary policy aggressively.

Supply chain issues are moderating

Some further good news on the supply side. An index of supply chain pressure: shipping and freight costs and how quickly the chain is moving along (compiled by the NY Fed) shows while pressure is still high, it is declining.

China remains buoyant

Chinese equities, as represented by MSCI China, took a breather and were largely flat for the week. Some positive news on the trade front: Vice Premier Liu He had a call with US Treasury Secretary Janet Yellen as President Biden considers lifting tariffs on imported Chinese goods to reduce domestic inflation.

Beijing attempted to roll out China’s first vaccine mandate by limiting access to public areas based on vaccination status, but had to backtrack shortly due to backlash.

Earning Insights

We covered market moves here: Coinbase, Amazon, and Tesla.

Elon Musk intends to terminate his $44bn deal to buy Twitter, but the mechanism and clause to do so would not be straightforward as Twitter has said that they will enforce the deal. We will share more next week as details emerge.

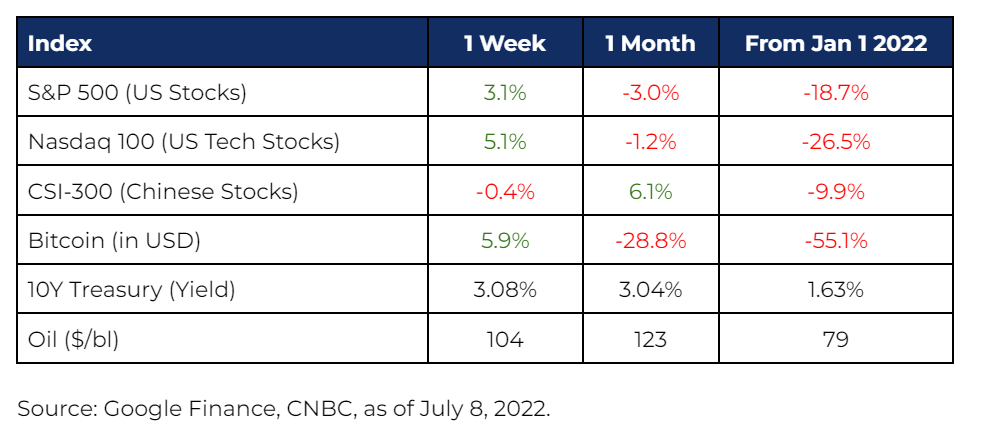

Market Stats

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.