This time last year, the biggest questions for investors were what shape the COVID-19 recovery would take, and how quickly the global economy would rebound. Terms like V-, U-, L-, and K-shaped recovery were bandied about and the broad consensus was that a sustained global recovery would only be possible if a vaccine could be found.

Today, we’re seeing one of the most robust post-recession recoveries in 80 years. According to the World Bank, global growth is expected to accelerate to 5.6% this year, driven largely by the strength of the US and Chinese economies.

The US economic boom

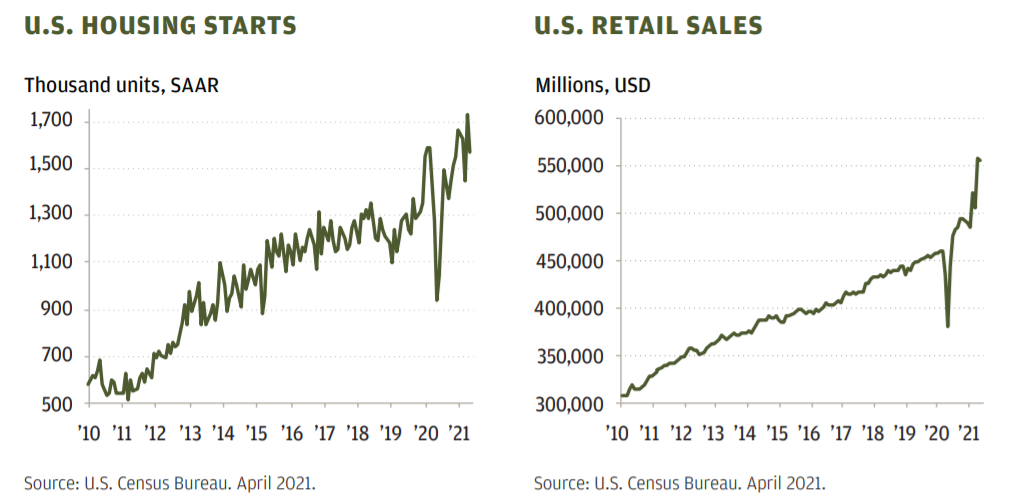

The US economy is poised for supercharged growth this year, thanks to a combination of unprecedented fiscal stimulus and a successful vaccination program. With the economic reopening well underway, US consumers are starting to spend their stimulus checks and past year’s savings. Retail sales are 20% above pre-pandemic levels. US home sales are soaring – home construction starts are at their highest level since 2006.

While travel has been slow to resume in Asia, the US domestic air travel market has shown strong signs of recovery amid rising vaccination rates.

All in all, the US recovery looks to be on solid footing and officials have raised their GDP expectations for this year to 7% from 6.5% previously.

Sustained China growth

China is already in its fifth consecutive quarter of growth and the World Bank forecasts a GDP growth of 8.5% this year for the country.

As the first country to successfully control the COVID-19 pandemic, China was also the first to experience a swift recovery. By the end of last year, its economy had returned to its pre-pandemic growth path.

Much of the expected growth this year is forecast to come from strong consumer demand. Due to COVID-19, Chinese consumers have largely shifted their spending from outside China (on things like travel and overseas shopping) to domestic Chinese products.

For instance, sales of Chinese sports brands quadrupled on a yearly basis on JD.com, while sales of domestic Chinese cosmetic brands surged 64 times year-on-year.

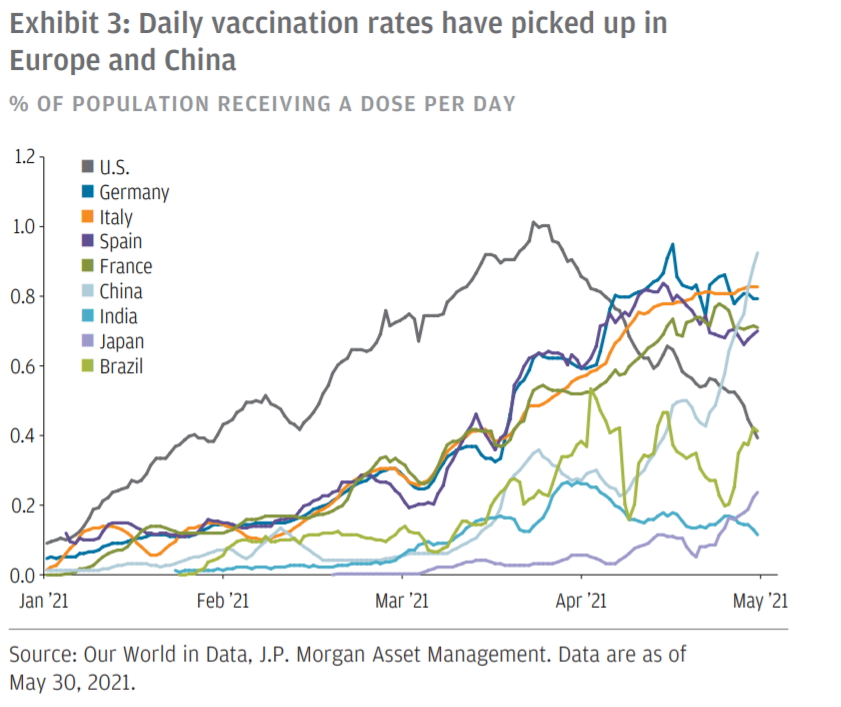

China has also made great strides on the vaccine front, with a pickup in daily vaccination rates in May. This will be key in China’s plans to reopen its borders safely and restart international travel.

The global recovery is still uneven

The US and China may be charging ahead, but the economic recovery is still uneven across different parts of the world.

COVID-19 remains a clear threat in many places. In Southeast Asia and Latin America for example, powerful second and third waves will likely dampen economic activity in the second half of 2021.

Closer to home, another outbreak of community cases could lead to a possible delay in the next stage of Singapore’s re-opening. That said, Singapore is speeding up its vaccination efforts. It is quite likely that we should see cases stabilize and a return to Phase 3 by the end of the year.

The new normal is here to stay

After more than a year of lock-downs and other restrictions, most of us can’t wait to resume the things we once took for granted, such as dining out and travelling.

But even after the world beats back COVID-19, certain things will just never be the same. One striking example is the way in which the pandemic has accelerated digitization in many areas of life.

The rise of Zoom and other work from home technologies have unlocked new ways for businesses to enhance productivity. The race to find a vaccine spurred medical innovations that could permanently transform healthcare. Trends like e-commerce, online gaming and streaming entertainment boomed during lock-downs and look set to stay even as the world reopens.

The pandemic has shifted consumer behavior and these adaptations will be hard to shake. Instead of a full return to the “old normal”, we might see more of a hybrid model: workers working remotely and in the office; e-commerce complementing physical shopping.

Keep a long-term view on technology and innovation

The accelerated adoption of technology was also reflected in the stock market performance of last year. In 2020, the explosive growth of FAANG stocks (Facebook, Amazon, Apple, Netflix, and Google) drove much of the S&P 500 overall returns.

In 2021, the technology sector has lagged as other cyclical sectors like banks, energy and airlines rebounded alongside the economic recovery. While these sectors may benefit from the reopening in the near term, it is unlikely that they have the potential to lead markets higher in the longer term.

For one, increases in hyper-connectivity, artificial intelligence (AI), exponential processing, and robotics and automation are driving digital transformation. These trends will have lasting impact on the way we work and live. Tech-oriented companies have also dominated the stock market for years as they’ve continued to grow almost regardless of the economy’s strength.

For these reasons, we continue to encourage investors to maintain a long-term perspective on the tech sector and adopt a diversified approach to investing.

Challenges ahead

As we wrote about last month, inflation and rate hikes are the top concerns for investors this year.

In an update last Wednesday, the US Federal Reserve said it might raise interest rates earlier than it had previously expected, penciling in two rate hikes in late 2023. This comes after US inflation data showed the inflation rate rising to a yearly rate of 5% in May, the highest level in 13 years.

US stocks fell last week as the Fed’s sudden hawkish shift caught investors off guard. But the major benchmarks – the Dow, S&P 500 and Nasdaq Composite – bounced back on Monday (21 June) as the market adjusted to the Fed’s rate rise outlook.

The rebound indicates that the stock market largely believes that inflation will be transitory and US economic growth will continue to gather momentum. The bond market is not signaling an inflationary environment either. Despite a hotter economy, the 10-year US Treasury yield is still hovering around 1.5% even after the Fed’s policy shift.

Inflation data and rate hike expectations could still lead to further market volatility in the months ahead. But as long as these don’t shift too much from what the market expects, the turmoil should pass fairly quickly.

Conclusion

Given the speed of the recovery to date, a sustained economic recovery in the next half of 2021 could be on the cards. Market leadership may be rotated across different market sectors; for long-term investors, having diversified exposure to different sectors and asset classes is still the best strategy.

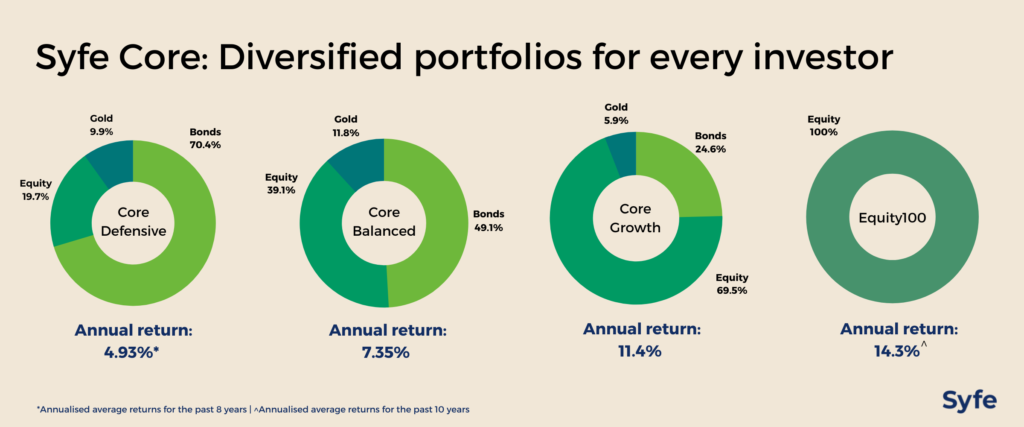

With strong growth in both the US and China, we see it prudent for investors to have meaningful exposure to both countries as well. Investors can consider our Syfe Core portfolios for US-China exposures across stocks, bonds, and gold, or Core Equity100 for a pure equity investment in these key markets.

You must be logged in to post a comment.