In our most recent webinar, we dived into how Singaporean investors can invest for rising interest rates, and how S-REITs and dividend stocks may be suitable assets to look at. Special thanks to our three panelists for the session, who shared their takes and perspectives:

- Geoff Howie, Market Strategist from SGX Group;

- Gerald Wong, CFA, Founder & CEO of Beansprout;

- Ritesh Ganeriwal, Head of Investment & Advisory at Syfe

You may watch a recap of our webinar here:

Due to time constraints, we couldn’t address all questions during the webinar. However, we have selected a few of the most popular questions on this topic, and address them below.

On the Market’s Performance

Why are US market indices rising while the STI remains stagnant, especially our local banks?

For the US markets, the technology sector has led most of the gains this year, with an impressive increase of 44% YTD. This surge is particularly attributed to major tech companies like Microsoft, Apple, and Alphabet (Google’s parent company). In contrast, the US financial services sector has shown relatively flat performance, with a modest rise of 1.5% YTD.

Regarding the Straits Times Index, the main sectors are banking, comprising around 50% of the index, and real estate, accounting for 19%. Both sectors are primarily driven by local and regional economic factors. For local banks, while there has been an improvement in net interest income, loan growth has been lacklustre due to relatively soft economic activities, which has capped the stock prices.

About the Recession

Do you foresee an upcoming recession in the US, and how might it impact the REITs and banking sectors in Singapore?

Our base case scenario anticipates a soft landing or a mild recession in the US. In recent quarters, we have observed a downward trend in inflation, while economic growth remains relatively resilient. The US GDP for Q3 grew at an annualised rate of 4.9% quarter-over-quarter, marking the highest growth since Q1 2022.

For the Singapore banking sector, the impact of a US recession could be seen in the lower loan growth. If the Federal Reserve opts to cut interest rates, this could lead to narrower interest rate margins for local banks. Despite these potential challenges, the Singapore economy is projected to demonstrate relative resilience. The local banks are well-capitalised and robust and prepared to weather the downturn effectively.

For S-REITs, the occurrence of a mild recession in the US is anticipated to lead to interest rate cuts, potentially aiding the recovery of REIT markets. Presently, S-REITs are trading at a price-to-book ratio of 0.8X, close to a 10-year low, indicating that much of the negative news has already been reflected in their current valuation.

On China

Will the property market in Singapore crash like what is happening in China?

The dynamics of the property markets in Singapore and China are distinctly different.

In Singapore’s residential market, there is less issue of oversupply, as indicated by the relatively low number of unsold units. Thanks to macroprudential measures implemented by the Monetary Authority of Singapore (MAS), such as the Total Debt Servicing Ratio (TDSR) and Loan-to-Value (LTV) limits, consumers generally do not take excessively high financing for property purchases.

In the commercial market sector, the fundamentals remain robust. The occupancy rate for office space is around 90%*, and for retail space, it’s approximately 93%*, returning to pre-COVID levels.

A September 2023 report by UBS noted that the real estate bubble index in Singapore stands at 0.45, indicating fewer market bubbles. The lower the index, the lesser the bubbles. For context, Hong Kong’s score is 1.24 and Tokyo’s is 1.65.

*Source: URA Q3 2023 Statistics

Allocation to S-REITs

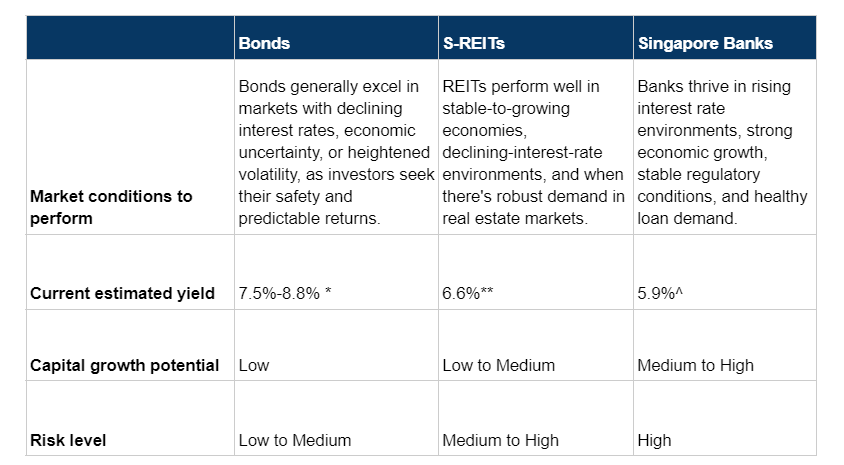

How should one determine the allocation between bonds, Singapore banks, and Singapore REITs?

The allocation among bonds, banks, and REITs largely depends on an individual’s risk tolerance and investment goals. Here’s a summary to provide an overview of the three instruments.

Following the recent market pullback, bonds, S-REITs, and bank stocks offer relatively high yields. Investors seeking stable income with a lower risk appetite may prefer a higher allocation to bonds, known for their historically lower price volatility. S-REITs are attractive to a broad range of investors, offering steady income, lower risk, and portfolio diversification through real estate. Meanwhile, bank stocks are ideal for those seeking both growth and income, comfortable with volatility, and knowledgeable about economic and financial trends, given their cyclical nature and reliance on the economy.

For a more personalised service regarding the allocation specific for your situation and needs, you can reach out to our wealth advisors.

Interest Rate Outlook

What does “Higher for Longer” mean? And How will this impact S-REITs?

The term “Higher for Longer” emerged following the September FOMC meeting. Contrary to market expectations, the Fed is unlikely to commence rate cuts in Q1 2024. This scenario suggests that the rate cuts may start in the second half of 2024. Rates will stay high for a considerable time before that.

Markets are forward-looking and tend to react in anticipation of future events. Assuming that inflation continues to trend downwards, the anticipation of eventual rate cuts could lead to a recovery in S-REITs.

About Syfe REIT+

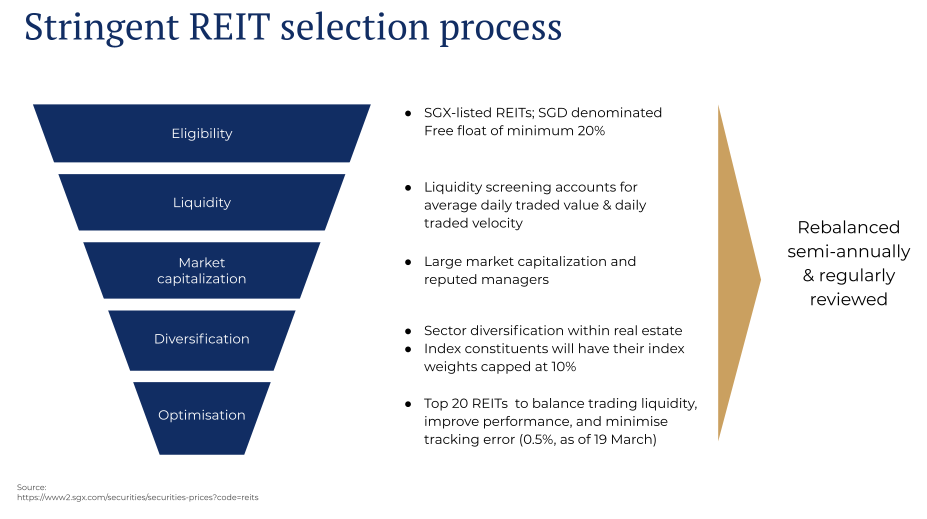

Could you please explain how Syfe selects the REITs for its REIT+ portfolio?

Syfe REIT+ is a passively managed portfolio and tracks iEdge S-REIT Leaders index. Instead of fully replicating the iEdge S-REIT Leaders index, Syfe uses an optimisation process to construct an index-tracking portfolio. The resulting REIT+ portfolio holds 20 REITs that are appropriately diversified across all sub-sectors and has a tracking error of just 0.5% to the index. Below is the REIT selection process.

The rebalancing of S-REITs typically occurs every six months. However, will Syfe consider an interim reallocation if there is an exceptionally compelling reason to do so, even when it is not the scheduled time for reallocation?

Yes, we can rebalance but only on an exceptional basis. Considering that our REIT+ portfolio focuses on the top blue-chip REITs in Singapore, significant rebalancing outside of the regular cycle is unlikely.

Read More:

Is now the time to invest in Singapore REITs?

Singapore Bank Stocks To Buy: DBS, OCBC, or UOB?

2023 Q4 Investment Outlook: What could “Higher for Longer” Mean?

You must be logged in to post a comment.