First weekly gain after 7 weeks of declines

S&P 500 broke its losing streak this week. The S&P 500 rose daily for the later half of the week, gaining more than 6% over the week. According to research from Bank of America, investors put more than US$20bn into global stocks for the week, making it the largest net inflow in 10 weeks. Just last week, the index briefly dropped into bear market territory (losing 20% from peak) before rallying shortly before markets closed.

Moderating Inflation

On Friday, we got the latest reading of the Personal Consumption Expenditure (PCE) index, which showed prices for core items (excluding more volatile components like food and energy) increasing by 0.3%, vs 4.9% last month. The April reading is still a high 6.3%, coming down slightly from 6.6% in March.

This is the Federal Reserve’s preferred inflation metric over the CPI as it accounts for all goods and services consumed by households and better reflects how prices are influencing consumer behaviour. The lower rate buoyed markets, signalling that inflation might be moderating. As these measures are compared against the same month last year, the lower rate could be due to base effects (starting from a higher base in Spring 2021). Nonetheless, this data point would factor into the FOMC’s stance as committee members weigh these indicators against whether they need to do more and raise interest rates more aggressively to rein in inflation.

FOMC Minutes

Minutes from the latest FOMC meeting in early May were released last Wednesday. The content did not reveal any major surprises as Fed officials have been communicating a lot more through interviews, press conferences on their thoughts about the state of the economy and the plan to reduce inflation. This is known as forward guidance.

The double hike (50bps increase) earlier this month buoyed markets as initially it seemed likely that a triple hike (75bps at one meeting) was on the table too. The minutes revealed that: “most participants judged that 50-basis-point increases in the target range would likely be appropriate at the next couple of meetings”.

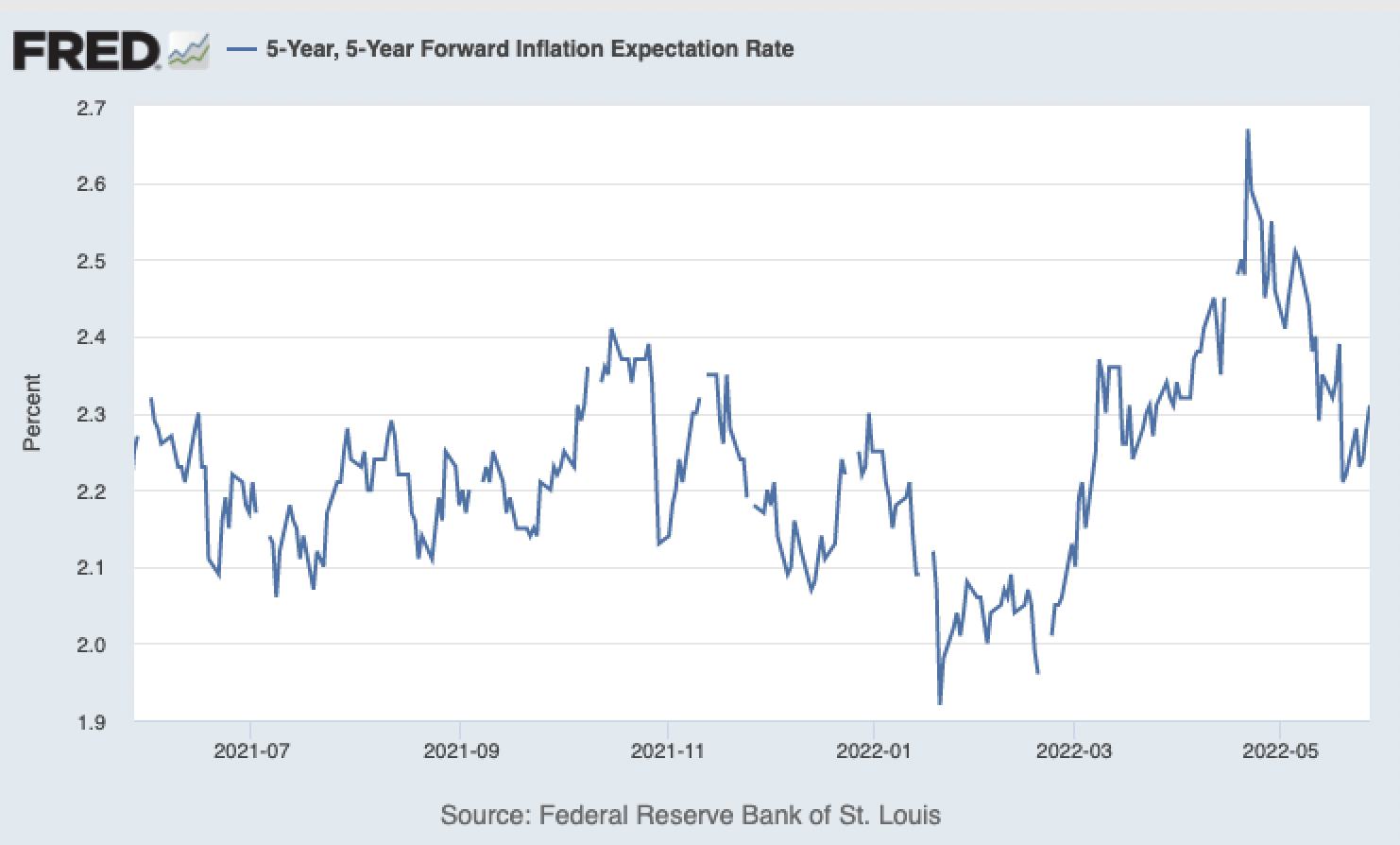

Has Inflation Peaked?

It certainly doesn’t feel this way, but market-based measures such as the 5Y5Y Forward Inflation Expectation Rate indicate that inflation is expected to revert to the mean longer term. This refers to the average inflation rate over a five-year period starting in five years time.

This metric hasn’t had the best track record in predicting what inflation would be – for instance, between 2004 and 2010, the 5-year 5-year over-anticipated what inflation would be between 2009 and 2020.

Earnings Highlight

We covered market movers here.

Retailers (Target, Costco, and Dollar Tree) had varying first quarter results. Target and Walmart benefited most during the pandemic as consumers bought durables and higher margin items like electronics. In the earnings call, Target revealed that they were carrying too much inventory: “stay-at-home” items like kitchen equipment and lawn furniture that may not move as quickly as the world re-opens. On the other hand, discount chains like Dollar Tree raised its forecast for profit growth as more consumers may be turning to them as inflation is still high.

Summer travel is expected to pick up in a big way. Southwest Airlines and JetBlue Airways said last week that their revenues for the second quarter were on track to be even higher than previously projected and that increases in fuel costs would be “more than offset” by higher ticket prices. Ticket bookings are at record highs, as consumers are still going ahead with travel despite higher prices for almost everything: tickets, accommodation, rental cars and gas.

What are other indicators telling us?

With a strong labour market still going (looking at Initial Jobless Claims this week), consumer spending remains robust. According to the Commerce Department, consumer spending rose 0.9% in April, 0.1% higher than consensus expectations. However, consumers are saving less. Household savings reached a peak during the pandemic through government support measures and decreased spending on services. The most recent measure saw households setting aside just over 4% of their after-tax income in April, the lowest since 2008.

Chinese securities buoyed

Chinese shares were up for the week too. After last week’s events that were seen as a positive turning point for Chinese internet stocks, big names in the sector beat analysts’ expectations this week: Alibaba, Baidu, Pinduoduo, Kuaishou all showed their resilience amid long lockdowns in various major cities in China.

Following up on promises to bring the economy back on track, the State Council outlined thirty-three policies and measures meant to stabilise the economy, including calling for key financial institutions to keep credit conditions accommodative.

Where could markets go from here?

Risks to growth have increased lately but the worst case scenario has not materialised. Companies and households are entering this next stage of the economic cycle with good fundamentals and strong balance sheets (and wide profit margins vs. historical levels for many corporations).

While growth may be held back by persistent inflationary pressures in the short term, investors can take a diversified approach: seeking balance between value and growth, and US and international. During times of market volatility, it becomes even more important to pay greater attention to the things one can control: diversification, asset allocation and cost.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.