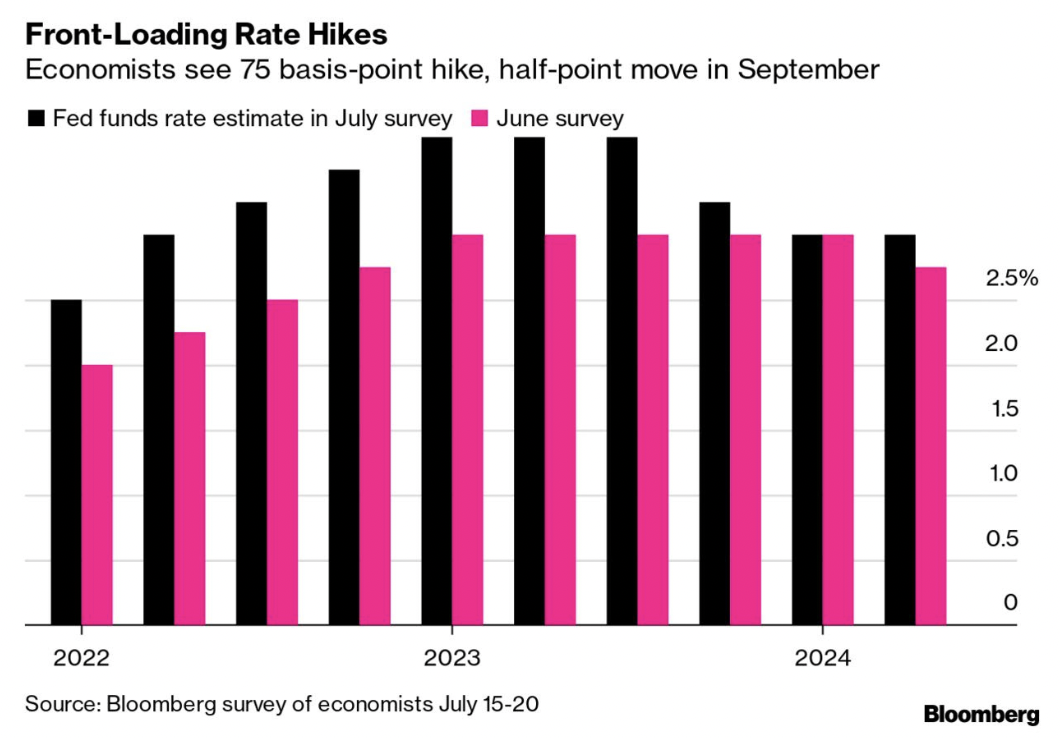

Gearing up for hikes

The Federal Reserve’s rate setting committee (FOMC) is set to meet next week (July 26-27). The market is expecting a 75bps hike (similar to the one delivered in June) to combat inflation, which rose to 9.1%.

Following the July meeting, economists see a smaller move in September. The committee is up against a tough fight – trying to bring inflation down without tipping the economy into a prolonged recession.

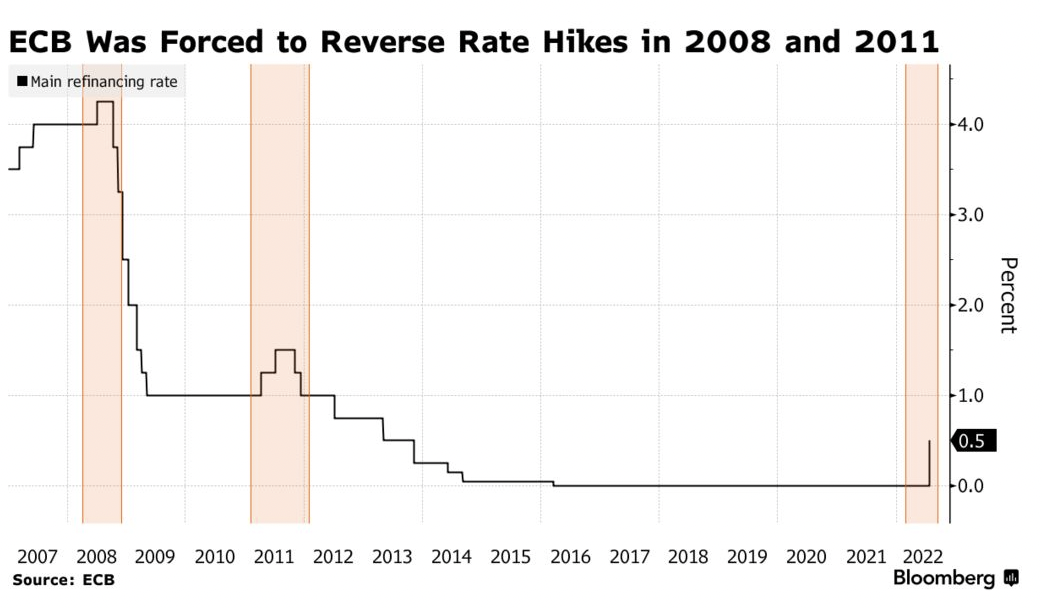

Running up that hill (too)

Like the Fed, the European Central Bank (ECB) made an outsized move this week – raising interest rates by double the amount that was expected from forward guidance. The somewhat unexpected move came as officials stated that they have to ensure that inflation expectations do not become entrenched, leading to potential wage price spirals and making it much harder to tame inflation.

Interestingly, the ECB has reversed hikes in 2008 and 2011 due to the Global Financial Crisis (GFC) and European Debt Crisis. Both times, interest rates were raised in July and subsequently reversed a few months later.

Again, there is merit in making a bigger move now, in case growth slows even more in the coming months. With inflation in the high single digits and bond yields being positive (after years of negative yielding debt), the ECB has some way to go in raising rates, starting effectively from zero.

Anchored at 3%

Despite high inflation and big hikes coming, yields on the 10 year US Treasury remain anchored at about 3%. As short term yields go above longer term yields, we get a treasury curve inversion (typically, investors look at the yield on the 2 year treasury vs that of the ten year).

A yield curve inversion has preceded every US recession in the last 50 years. This is seen as a recession signal, but the economist, Campbell Harvey, who is seen as a voice of authority on yield curve inversions prefers to use the 3 month Treasury instead of the 2 year, as it is more representative of current market conditions. Currently, 3 month yields remain below 10 year yields, but the gap has been narrowing as 3 month yields go up while 10 year yields remain at about 3%.

Many bond market participants think that the Fed is going to have to raise interest rates a bit too much and tip the economy into a recession, even if it will be a mild one. In this case, treasury yields will remain range bound. So, investors are still buying long dated treasury bonds now (when yields are high enough), locking that in even if yields could go higher as the Fed raises interest rates.

Didi’s massive fine

China fined Didi Global more than 8bn RMB (1.2bn USD), marking the end of a one year investigation. Didi’s Chairman and President were also fined 1 million yuan as Didi was found to have violated laws around data management and neglecting to comply with regulations.

Post the announcement, Didi’s share rose 4% in US trading as the penalties fell short of the worst possible scenario. Didi is expected to prepare for the HK listing and its app has returned to domestic app stores. Other large Chinese tech companies: Tencent and Alibaba recovered too – the penalties and requirements for rectification laid out helps give tech companies a better understanding of where the red line may be.

Big week for tech earnings:

Besides the FOMC meeting, it will be a big week for technology companies too, with Apple, Microsoft, Meta, and Amazon reporting Q2 earnings.

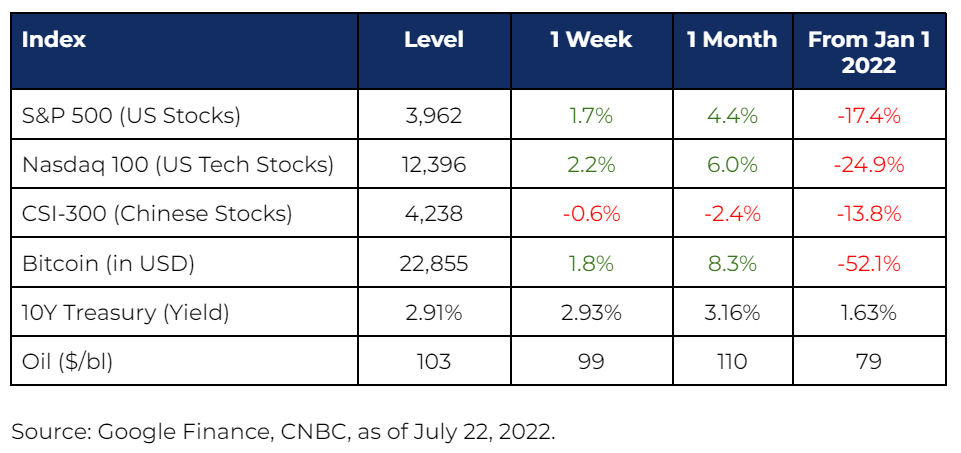

Market Stats

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.